Connect with us

DELHI: India’s subscription economy is learning to move at thumb speed. As UPI cements itself as the country’s default way to pay, ChanaJor OTT is leaning...

MUMBAI: PhonePe, the Walmart-backed digital payments firm, has received regulatory approval to proceed with its stock market listing, clearing a key hurdle after confidentially filing for an...

MUMBAI: If money talks, Jupiter Money just made a power move by bringing banking veteran Akhilesh Jha into the conversation. In a strategic hire that signals...

MUMBAI: Fintech just got a major shake-up. India’s largest listed retail stock broking house, Angel One has roped in Ambarish Kenghe as its new group chief...

MUMBAI: POP, the fintech startup targeting young Indian consumers, has appointed Chandresh Pancholi as its new head of engineering and product. Pancholi joins from Navi, where...

MUMBAI: Known affectionately in fintech circles as AK-no, not the Indian cinema stalwarts Anil Kapoor or Anurag Kashyap-Ambarish Kenghe is poised to script his own blockbuster....

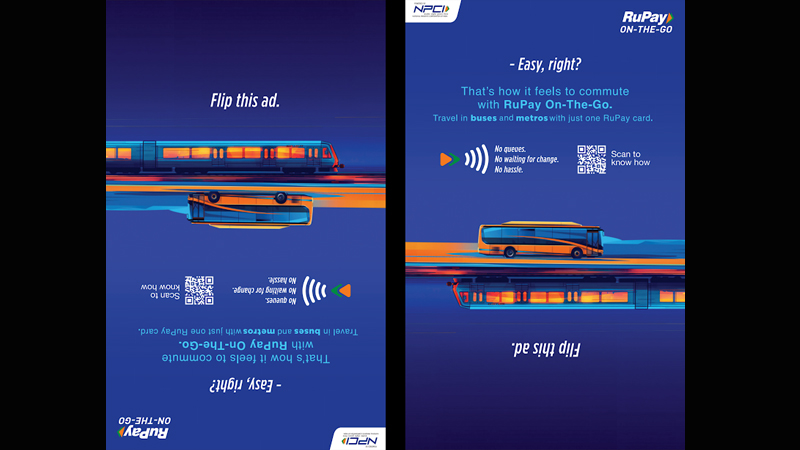

MUMBAI: Remember the days of frantic scrambles for exact change with rickshaw drivers, the despair of handing over a Rs 500 note, and the resigned sigh...

MUMBAI: It’s bringing out all its aces in a bid to create awareness and boost adoption of its card. Retail payment and settlement body National Payments...

Mumbai: It has been almost two decades since we saw the rise of the internet and various applications like Facebook, Twitter, Gmail, etc. They have brought...

Mumbai: Transak has announced that it is launching its full suite of services to India with the roll-out of UPI payment integration on platforms including Metamask,...

KOLKATA: In a bid to drive its reach and growth, digital payments platform PhonePe is betting big on the IPL by taking up six different sponsorships...

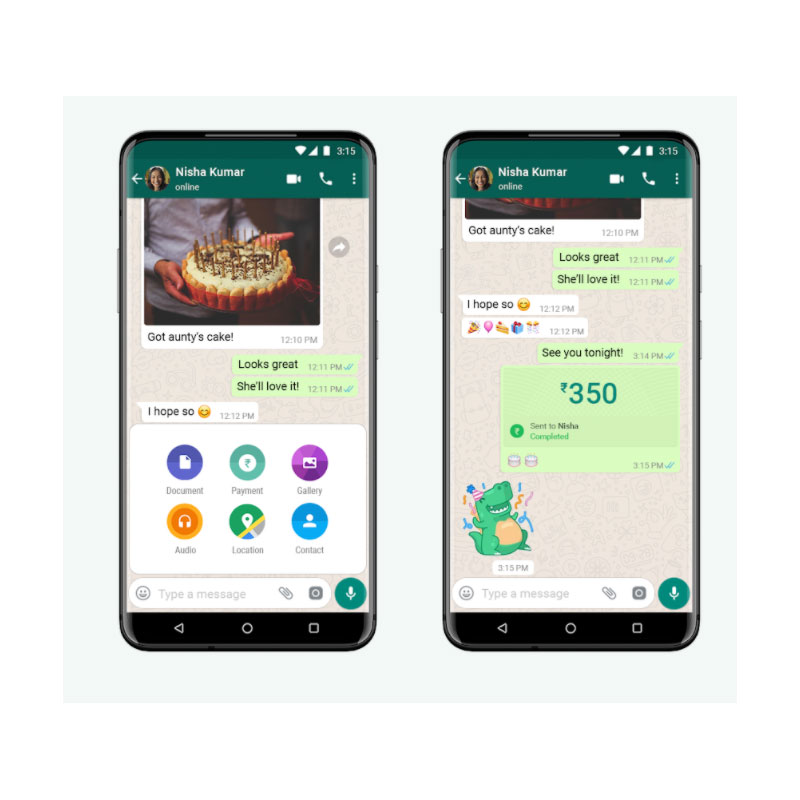

KOLKATA: In what could be a turnaround for India’s payments market, WhatsApp Pay has gone live today. WhatsApp’s parent company Facebook has been developing the payment...

KOLKATA: IN10 Media Network’s OTT platform, Epic On– recently launched in an all-new and reimagined avatar – has partnered with Amazon Pay. Through this collaboration, Amazon...

KOLKATA: The unified payments interface (UPI) service crossed a billion transactions a month last year and is on a constant upward trend. As more Indians make...

DELHI: In 2019, the four forms of online payments — debit cards, credit cards, Immediate Payment Services (IMPS) and Unified Payments Interface (UPI), recorded a combined...

MUMBAI: Nick Wrenn has been appointed as the managing editor of CNN’s production and newsgathering operations across Europe, the Middle East and Africa. Prior to the...