Connect with us

MUMBAI The advertising world, it seems, refuses to read the room. Whilst economists fretted over trade wars and geopolitical chaos, the ad business simply cracked on....

MUMBAI: It’s been two decades since I have been listening, participating and speaking about the great inflection point in digital in India. Every five years with...

KOLKATA: The Asia Video Industry Association (AVIA) has announced the publication of the governance framework for online curated content (OCC) services (hereafter referred to as the...

MUMBAI: Streaming video is becoming increasingly crucial for Indian legacy broadcasters, as GenZ continues to spend an increasing amount of time on video apps, watching their...

NEW DELHI– ZyXEL Communications, a world-class broadband networkingcompany providing a wide-ranging portfolio of Internet-enabled wired and wireless solutions, has introduced its NWD6505 and NWD6605 802.11ac Dual-Band...

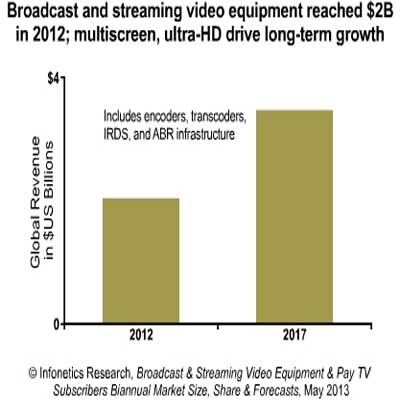

NEW DELHI: Broadcast and streaming video equipment market is likely to grow 12 per cent in 2013 from two billion dollars in 2012. According to...

MUMBAI: More than 94 million people in the US in June 2005, or 56 per cent of the domestic Internet population, viewed a streaming video online,...