Connect with us

Mumbai: Kantar, a marketing data and analytics company, has launched ‘Uncovering Consumer Decision Making in Digital Commerce’ a comprehensive report collating multiple studies done across various...

Mumbai: In the run-up to this year’s festive season, Flipkart presents its H1 edition (January to June 2024) of the much-awaited ‘#FlipTrends’ report, which presents an...

Mumbai: MiQ, the world’s largest independent programmatic media partner for brands and agencies, unveiled its global Advanced TV research report, which surveyed 7,000 consumers and 1,100...

Mumbai: Consumer sentiment shows recovery and uptick of 1.2 per cent points for urban Indians in December 2023, according to the Refinitiv-Ipsos Primary Consumer Sentiment Index...

Mumbai: Ipsos Global Predictions for 2024 shows a positive outlook emerging for the year 2024 with 87 per cent urban Indians and 70 per cent global...

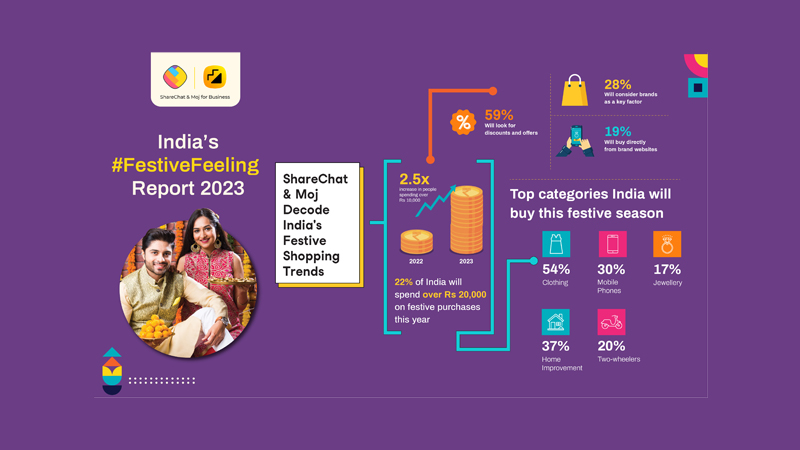

Mumbai: Capturing India’s shopping sentiment this festive season, ShareChat and Moj, India’s leading homegrown social media and short video platforms, today released a report titled India’s...

Mumbai: Dish TV India on Wednesday announced their financial results for the first quarter of the financial year 2022–2023. The company’s reported net profit declined 64.47...

Mumbai: India’s OTT video market will reach total revenues of $3 billion in 2022 and is expected to more than double to $7 billion by 2027,...

Mumbai: The Indian sports media market is expected to grow to over $13.4 billion by 2027, as per a report by investment consultants Anand Rathi Advisors...

Mumbai: On building a profitable business, Hathway Cable and Datacom managing director Rajan Gupta stated that he believes FY 2022–23 will be a transformational year for...

Mumbai: Box office numbers reach Rs 4,200 crore during January-April recording the cinema exhibition industry’s best performance post-Covid, as per a report by cinema advertising company...

Mumbai: WATConsult, an Isobar Company and the globally awarded hybrid digital agency from dentsu India, has released the fifth report of WATInsights – digital commerce series....

Mumbai: Sports media rights investments in India will grow at 10.1 per cent CAGR (compound annual growth rate) over 2021-26, bolstered by demand for cricket properties,...

Mumbai: There has been an increasing awareness of the metaverse recently. It was revealed in Wunderman Thompson Intelligence’s latest survey ‘New Realities: Into the Metaverse and...

Mumbai: India has a sports fan base of 136.3 million, according to the latest report by Ormax Media. A sports fan is defined as someone who...

Mumbai: The year 2021 saw a resounding comeback for sports sponsorships and media deals, as compared to 2020 when the pandemic took over. The size of...

Mumbai: Users spent a total of 4.35 billion minutes gaming on MX Player in 2021, the media company reported, with an average watch time of 56...

Mumbai: 2021 has been a year of discovery for consumers. As we learn to adjust in a world that changes often and unpredictably, brands would need...

Mumbai: In recent times, several advertisements have faced controversy with various individuals or groups objecting to them. There is also a growing trend of ads and...

Mumbai: Worldwide spending on telecommunications and pay-TV services is forecast to reach $1.5 trillion in 2021, representing an increase of one per cent over 2020, according...

Mumbai: The Indian gaming market is poised to reach $6-7 billion in value by 2025, according to a report by the Internet and Mobile Association of...

Mumbai: Pay TV subscription revenue is expected to reach $7.6 billion by 2026 over $6.4 billion in 2021, stated Media Partners Asia in its latest report...

Mumbai: India has 353 million OTT users and 96 active paid subscriptions, according to Ormax OTT Audience Report 2021. The research is based on a sample...

Mumbai: Global brand consultancy Interbrand launched its Breakthrough Brands 2021 report unveiling the top 30 brands set to take the US market by storm in the...

MUMBAI: Alcohol ad spend in 12 key markets, including India will grow by 5.3 per cent in 2021, ahead of the 4.9per cent growth of the...

NEW DELHI: When it comes to entertainment, Indians are hooked to their mobile phones and unlikely to let go any time soon. In fact, mobile gaming,...

New Delhi: Checkbrand, an online sentiment analysis company, has analysed data for 45 top players on social media for the period of August – October 2020...

NEW DELHI: Mobile manufacturer Vivo has shared the findings of the second edition of ‘Smartphones and their impact on human relationships 2020’, a study that showcases...

MUMBAI: Zydus Wellness Ltd reported a growth of 9.3 per cent in gross sales for the second quarter ending 30 September 2020. The total income from...

MUMBAI: Credit rating agency, Fitch Ratings, stated that India’s new National Digital Communication Policy (NDCP) could manage to benefit the telecom sector by making it easier...

MUMBAI: Marketing technology company 4C, in its latest report, reveals that spend across major social and mobile platforms in the first quarter of 2018 increased significantly...

MUMBAI: OnePlus continued its growth in the overall Indian premium Android smartphone segment (above $400) by capturing 48 per cent market share in Q4 2017, as...

MUMBAI: Deloitte India has launched the eighth edition of its report on technology, media and telecommunications which predicts major advances in machine learning, voice over LTE...

MUMBAI: The increasing penetration of digital media in India is creating huge opportunities for marketers to reach out to untapped audiences in newer ways than before....

MUMBAI: The advertising spend in India is expected to grow by 12.5 per cent in 2018 from 9.6 per cent last year, according to Dentsu Aegis...

MUMBAI: The Parliament’s Standing Committee on Information Technology and Communications (SCIT) has sent out a stern message to the stakeholders of India’s broadcast and cable industry,...

MUMBAI: Oyo hotels has launched its analysis report which reveals that tariffs in its hotels across top leisure destinations in India are six per cent lower...

MUMBAI: Majority of media and marketing professionals are sleep-starved, according to Expedia’s new edition of Vacation Deprivation Report 2017, stating that they cannot afford to take...

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua.

MUMBAI: J. Walter Thompson Intelligence’s newly launched innovation and futurism unit The Innovation Group has unveiled a new report on Generation Z (those born in the...

MUMBAI: The year 2014 saw the sports landscape in the country being altered as maiden sports leagues were introduced. But what will be the road ahead...

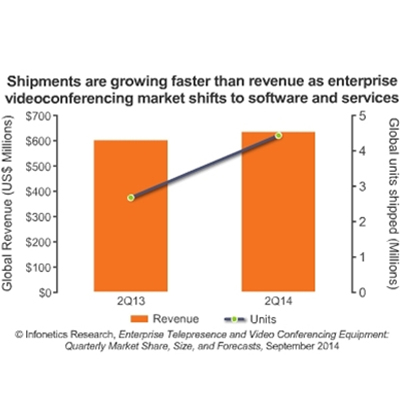

NEW DELHI: The video conferencing and telepresence market rose two per cent to $752 million in the second quarter of this year. According to an...

MUMBAI: As of June 2014, there were 243 million claimed internet users in India out of which 192 million are active internet users who access internet...

MUMBAI: With laptops, smartphones and tablets becoming a part and parcel of people’s lives today; internet is bound to become an integral part of advertising and...

MUMBAI: A major new strategic management report warns that broadband video services will eventually displace broadcast distribution, but telecommunications providers may not be the ultimate winners...

MUMBAI: 2004 was a landmark year for the growth of digital services, according to the record industry. Over 180 legitimate music download services were launched globally...

MUMBAI: For the third year in a row, US broadcaster CBS has catalogued efforts by its television network, programming arms and local television stations in a...

MUMBAI: The CII-KPGM report has identified ten action points for the entertainment industry and the government. The aim is to drive home the point that growth...

CANNES: Consumers will increase their power as the direct arbiters of the mantle of celebrity, thanks to the explosive growth and use of new entertainment technologies...

MUMBAI: The BBC Governors have published the latest findings of their Programme Complaints Committee – for the period 1 October to 31 December 2004. The Governors’...