Connect with us

MUMBAI: Zomato, the poster child of India’s food-tech revolution, has released its Q3 FY25 results, revealing a fascinating mix of growth and persistent challenges. Founded by...

Mumbai: The NDTV group reported its first quarter results for financial year 2023. The company’s revenue stood at Rs 113.70 crore up by Rs 18 crore...

BENGALURU: Indian content creator, aggregator distributor, specifically in the media and entertainment industry and now television broadcaster, Shemaroo Entertainment Ltd (Shemaroo) reported 39.7 percent drop in...

BENGALURU: The Essel Group’s News media arm Zee Media Corporation Ltd (ZMCL) reported an eight percent decline in revenue from operations to Rs 631.75 crore for...

BENGALURU: Mukesh Dhirbhai Ambani’s largest start up in the world, Reliance Jio Infocomm Limited (Jio) reported 62.5 percent growth in standalone profit after tax (PAT) for...

BENGALURU: Indian cable network and broadband company Den Networks Ltd (Den) reported consolidated profit after tax (PAT) of Rs 12.28 crore for the quarter ended 31...

BENGALURU: Indian telecom major Bharti Airtel reported 17 percent y-o-y increase in revenue for its Digital TV Services for the quarter ended 30 September 2019 (Q2...

BENGALURU: FMCG player Procter & Gamble Hygiene and Health Care Ltd (P&G) reported 7.6 percent year-on-year (y-o-y) growth in revenue from operations for the quarter ended...

BENGALURU: Indian film and media company Eros International Media Ltd (Eros) reported a 15.9 percent decline in consolidated net sales/income from operations (Op Rev) for the...

BENGALURU: Indian content creator, aggregator and distributor, specifically in the media and entertainment industry, Shemaroo Entertainment Ltd (Shemaroo) reported 15.9 percent year-on-year (y-o-y) growth in revenue...

BENGALURU: Mukesh Dhirubhai Ambani’s largest startup company in the world – Reliance Jio Infocomm Limited (Jio) reported 6.1 percent growth in standalone profit after taxes (PAT)...

BENGALURU: Indian direct to home (DTH) behemoth Dish TV India Ltd (Dish TV) reported profit after tax (PAT) of Rs 152.69 crore for the quarter ended...

BENGALURU: In the first quarter of the previous fiscal, restructuring at Indian multi system operator (MSO) Hathway Cable and Datacom Ltd (Hathway) had brought for it...

BENGALURU: Indian direct to home (DTH) behemoth Dish TV India Ltd (Dish TV) reported profit after tax (PAT) of Rs 19.7 crore for the quarter ended...

BENGALURU: Backed by higher subscription revenue and a 93 percent collection efficiency, Indian multi-systems operator (MSO) Siti Networks Limited (Siti) posted 146 percent higher operating profit...

BENGALURU: Indian direct to home (DTH) behemoth Dish TV India Limited (Dish TV) reported profit after tax (PAT) of Rs 22.5 crore for the quarter ended...

BENGALURU: Indian multi system operator (MSO) and broadband internet services (broadband) provider GTPL Hathway Limited (GTPL) has reported a year-on-year (yoy) growth in standalone as well...

BENGALURU: Despite lower admits and occupancy during the quarter ended 31 December 2017 (Q3 2018, the quarter under review), Indian entertainment and exhibition company PVR Ltd...

MUMBAI: It would be safe to say that this was the year of the big DTH challenge. India’s cable TV multi system operators (MSOs) could not...

BENGALURU: Indian multi system operator (MSO) Den Network (Den) reported growth in operating revenue, operating profit (EBIDTA) and profit after tax (PAT) for the quarter ended...

BENGALURU: Indian cinema chain Inox Leisure Limited (Inox) has reported improved revenue and net profit after tax (PAT) for the quarter ended 30 September 2017 (Q2-18,...

BENGALURU: Indian entertainment and exhibition company PVR Limited (PVR) reported a slight decline in total revenue for the quarter ended 30 September 2017 (Q2-18, current quarter)...

BENGALURU: Indian integrated media content house Shemaroo Entertainment Limited (Shemaroo) reported 8.6 percent higher y-o-y consolidated Total Revenue for the quarter ended 30 June 2017 (Q1-17,...

BENGALURU: The Essel Group’s core education company Zee Learn Limited (ZLL) reported 2.43 times consolidated profit after tax (PAT) in the year ended 31 March 2017...

BENGALURU: Indian direct to home (DTH) company Dish TV India Limited (Dish TV) has reported growth across important financial and operational parameters including operating revenues (TIO)...

BENGALURU: Indian direct to home (DTH) company Dish TV India Limited (Dish TV) has reported growth across important financial and operational parameters including operating revenues (TIO)...

BENGALURU: The Essel Group’s news network Zee Media Corporation Limited (ZMCL) reported more than double (2.47 times) year-over-year (y-o-y) operating profit (Simple EBIDTA) for the quarter...

BENGALURU: The Essel Group’s news network Zee Media Corporation Limited (ZMCL) reported more than double (2.47 times) year-over-year (y-o-y) operating profit (Simple EBIDTA) for the quarter...

BENGALURU: The board of directors of the Essel group’s education company Zee Learn Limited (ZLL) have declared a first time ever dividend of 5 percent per equity...

BENGALURU: The board of directors of the Essel group’s education company Zee Learn Limited (ZLL) have declared a first time ever dividend of 5 percent per equity...

BENGALURU: DB Corp Limited (DB Corp), home to flagship newspapers Dainik Bhaskar, Divya Bhaskar, Dainik Divya Marathi and Saurashtra Samachar reported 10.5 percent higher consolidated revenue...

BENGALURU: DB Corp Limited (DB Corp), home to flagship newspapers Dainik Bhaskar, Divya Bhaskar, Dainik Divya Marathi and Saurashtra Samachar reported 10.5 percent higher consolidated revenue...

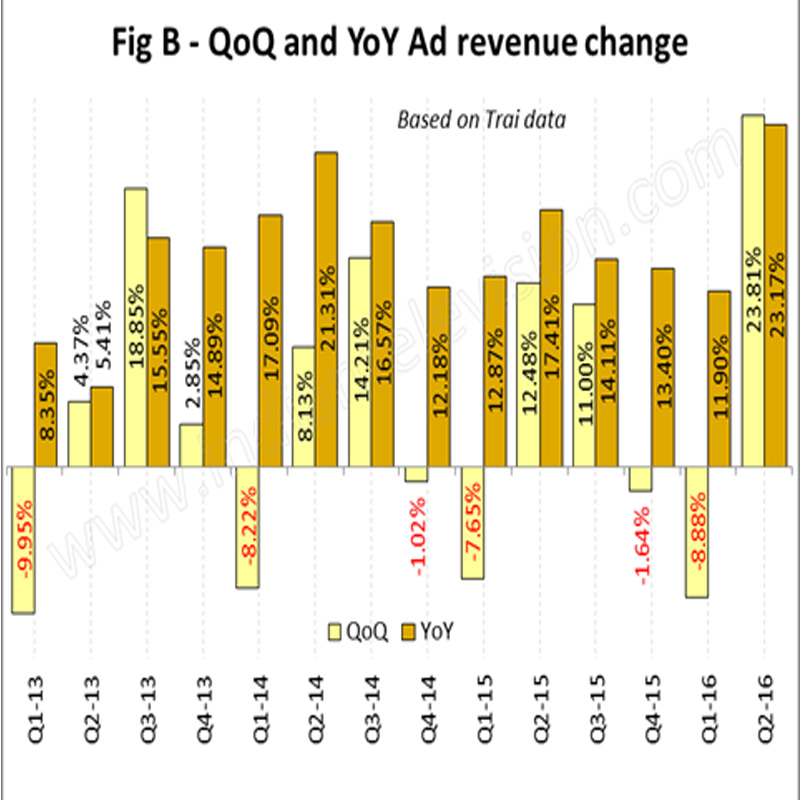

BENGALURU: Indian digital cinema distribution network and in-cinema advertising platform, UFO Moviez Limited (UFO) reported a 9.5 percent year-over-year (y-o-y) growth in advertising revenue for the...

BENGALURU: Indian digital cinema distribution network and in-cinema advertising platform, UFO Moviez Limited (UFO) reported a 9.5 percent year-over-year (y-o-y) growth in advertising revenue for the...

BENGALURU: Indian motion picture exhibition, production and distribution house PVR Limited (PVR) reported more than nine-fold (9.3 times) profit after tax (PAT) for the fiscal ended...

BENGALURU: Indian motion picture exhibition, production and distribution house PVR Limited (PVR) reported more than nine-fold (9.3 times) profit after tax (PAT) for the fiscal ended...

BENGALURU: Sun TV Network Limited (Sun TV) reported 7.3 per cent growth in consolidated Total Income from Operations (TIO) and 16.8 percent growth in profit after...

BENGALURU: Sun TV Network Limited (Sun TV) reported 7.3 per cent growth in consolidated Total Income from Operations (TIO) and 16.8 percent growth in profit after...

BENGALURU: Music Broadcast Limited (MBL), which runs Radio City, reported 14.9 YoY (year-on-year) growth in operating revenue (OpRev) for the quarter ended 31 December, 2015 (Q3-2016,...

BENGALURU: Music Broadcast Limited (MBL), which runs Radio City, reported 14.9 YoY (year-on-year) growth in operating revenue (OpRev) for the quarter ended 31 December, 2015 (Q3-2016,...

BENGALURU: Indian private FM player Entertainment Network (India) Limited (ENIL) reported 22.9 per cent YoY increase in Total Income from Operations (TIO) in the quarter ended...

BENGALURU: Indian private FM player Entertainment Network (India) Limited (ENIL) reported 22.9 per cent YoY increase in Total Income from Operations (TIO) in the quarter ended...

BENGALURU: The Essel group’s education company Zee Learn Limited (Zee Learn) reported 12.4 percent higher YoY Total Income from Operations (TIO, revenue) in the quarter ended...

BENGALURU: The Essel group’s education company Zee Learn Limited (Zee Learn) reported 12.4 percent higher YoY Total Income from Operations (TIO, revenue) in the quarter ended...

BENGALURU: Balaji Telefilms Limited (Balaji Telefilms) reported 3.5 times consolidated profit after tax (PAT) in the quarter ended 30 September, 2015 (Q2-2016, current quarter) at Rs...

BENGALURU: Indian custodians of music company Saregama Limited (Saregama) reported 35.6 per cent YoY growth in revenue or Total Income from Operations (TIO) for the quarter...

BENGALURU: Tips Industries Limited (Tips) reported a 12.5 per cent growth in its Audio Products Sales to Rs 9.01 core (75 per cent of Total Income...

BENGALURU: HT Media Limited (HT Media) reported 7.3 per cent growth in total income from operations (TIO) for the quarter ended 30 September, 2015 (Q2-2015, current quarter) at Rs 601.55...

BENGALURU: This is the third consecutive quarter that direct to home (DTH) company Dish TV has reported growth across important financial and operational parameters including operating...

BENGALURU: An 18.2 per cent YoY increase in advertising revenue ramped up Hindustan Media Ventures Limited (HMVL) total revenue by 16.2 per cent during the quarter...