Connect with us

MUMBAI: Ipsos India has found a new country head and managing director in Amit Adarkar, who will take charge from first week of September. He replaces...

MUMBAI: Little did anyone know that the Modi sarkar that had vowed to boost growth, control inflation and restore investor confidence will actually work wonders at...

MUMBAI: 50 per cent Indians are optimistic about Indian economy and expect that the economy will be stronger in next six months, a rise of two...

MUMBAI: India’s economic confidence revived substantially due to healthy farm output, a sharp boost in exports and narrowing of current account deficit, according to a report...

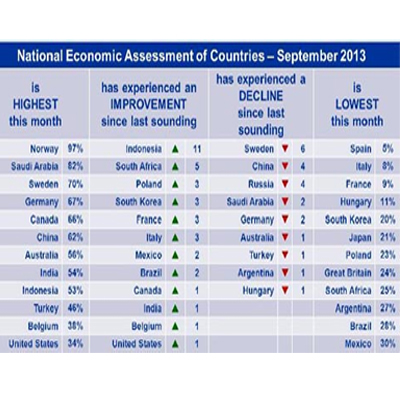

MUMBAI: India’s economic confidence recovered marginally but it remains uncomfortably uncertain as food inflation remains sky high and economic growth dwindling, according to a report by...

MUMBAI: India’s economic confidence remained shaky due to gloomy investor sentiments, chronic gaps in infrastructure, high inflation and interest rate, according to a report by global...

MUMBAI: Hansa Research and Ipsos have entered into a Memorandum of Understanding (MoU) to jointly bid for the new Indian Readership Survey (IRS) contract that starts...

MUMBAI: India‘s Economic Confidence grew by six points to 75 per cent in the month of October compared to the previous month, becoming the second most...