Connect with us

SINGAPORE: Forget the remote control. Asia-Pacific’s couch potatoes are voting with their thumbs — and the verdict is brutal for old-school television. Media Partners Asia’s annual...

SINGAPORE: The Asia Video Industry Association (Avia) has slipped two new power players into its boardroom, adding extra muscle as the region’s video business hurtles through...

MUMBAI: Three weeks. That’s all it took for FlareFlow to vault from newcomer to number one on America’s free entertainment app charts, on both iOS and...

SINGAPORE: Micro-dramas, once a fringe curiosity, are now a juggernaut. China’s revenues rocketed from $0.5 billion in 2021 to $7 billion in 2024 and will overtake...

BALI: JioStar’s Sushant Sreeram came out swinging at APOS 2025, tearing up the traditional streaming script with a bold case for fluid monetisation and empathy-first design....

MUMBAI: To use a cricket analogy, television is going to go even more on the backfoot while online video shall come charging down the pitch to...

Mumbai: The premium video-on-demand (VOD) category, driven by advertising and subscription, generated $1.04 billion in revenues over 1H 2024, up 38 per cent from $760 million...

Mumbai: Media Partners Asia’s (MPA) 2024 Asia Video Content Dynamics report offers a comprehensive analysis of content investment, engagement, and viewership across TV, VOD, and theatrical...

Mumbai: The premium video-on-demand (VOD) landscape in Southeast Asia continues to grow revenues at a double-digit pace with viewership relatively robust, as revealed by the latest...

Mumbai: The premium video-on-demand (VOD) landscape in South Korea grew subscribers, revenues and engagement at robust levels in 1H 2024 according to analysis conducted by ampd,...

Mumbai – An insightful report released today unveiled the transformative power of India’s streaming video on demand (VOD) industry and its contribution to the nation’s video...

Mumbai: The Asia Video Industry Association (AVIA), held its annual OTT Summit in Singapore on 5 December, where over 90 per cent of the speakers were...

Mumbai: In a fireside conversation at APOS Bali (Indonesia) 2023, created and curated by Media Partners Asia (MPA), Prime Video VP international prime video Kelly Day...

Mumbai: APOS, the defining voice and global platform for the Asia Pacific media and telecoms industry, took place from 26-28 September 2023, at the Ayana Estate...

Mumbai: APOS, the defining voice and global platform for the Asia Pacific media and telecoms industry, took place from 26-28 September 2023, at the Ayana Estate...

Mumbai: APOS, the defining voice and global platform for the Asia Pacific media and telecoms industry, took place from 26-28 September 2023, at the Ayana Estate...

Mumbai: India’s OTT video market will reach total revenues of $3 billion in 2022 and is expected to more than double to $7 billion by 2027,...

Mumbai: Sports media rights investments in India will grow at 10.1 per cent CAGR (compound annual growth rate) over 2021-26, bolstered by demand for cricket properties,...

Mumbai: The production of local originals in India is heating up and giving a boost to the creative economy. Online video platforms are expected to invest...

Mumbai: In the 18 months post-lockdown, Star TV network has emerged as the top broadcaster with over 30 per cent network share and strong growth across...

Mumbai: Sports will be a key focus area for the Zeel-Sony merged entity, said Zee Entertainment Enterprises Ltd (Zeel) MD and CEO Punit Goenka, as the...

Mumbai: Global streaming platform Netflix will pump more money into producing content in India, said chief executive officer Reed Hastings. The key executive of the streaming giant was...

Mumbai: Pay TV subscription revenue is expected to reach $7.6 billion by 2026 over $6.4 billion in 2021, stated Media Partners Asia in its latest report...

Mumbai: The focus areas of the company in the APAC market have not changed much in the last one year, said Luke Kang, who was appointed...

New Delhi: After a 27 per cent plunge in 2020, ad revenue in India is forecast to rebound strongly over 2020-25 with a CAGR of 13...

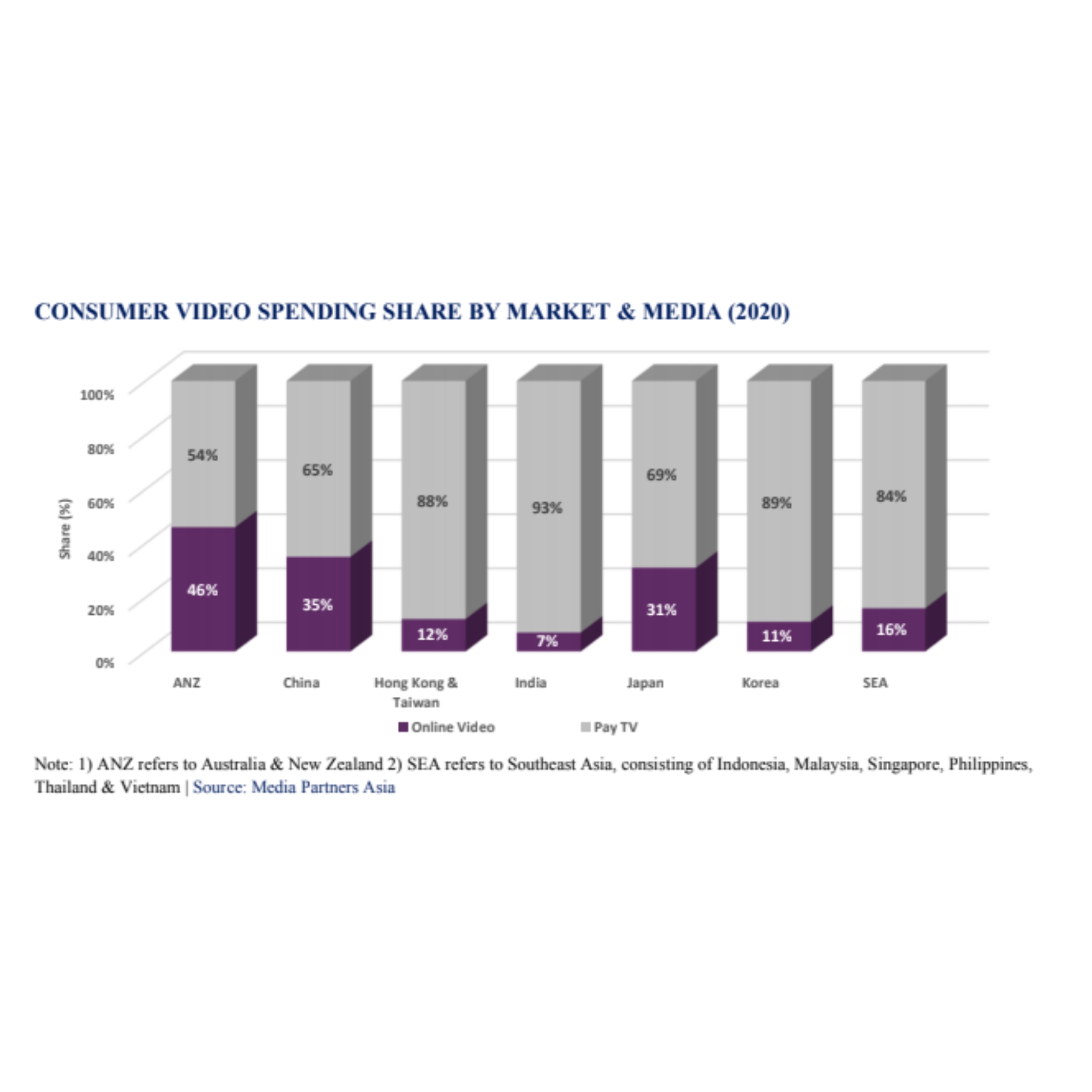

New Delhi: Consumer spending on video in the Asia Pacific (APAC) region grew nine per cent in 2020 to reach $58.3 billion in aggregate, according to...

New Delhi: Creator-led franchises will be more powerful and more profitable in the years to come if they can take a little more risk and own...

New Delhi: India is among a handful of countries where there is great scope for further penetration of television. Since the turn of the millennium, pay-TV...

NEW DELHI: As per a recent Media Partners Asia (MPA) report, India is going to be the most scalable pay-TV market in the APAC region, with...

MUMBAI: APOS, the defining voice and global platform for the Asia Pacific media, telecoms and entertainment industry, is shifting online in 2020 with two virtual editions...

MUMBAI: Disney+ Hotstar could have 25 per cent of the total online video revenue pie by 2025, second only to YouTube, according to Media Partners Asia...

MUMBAI: Video content budgets across India, Korea and Southeast Asia climbed 12% in 2018 to reach ~US$10 bil., according to the latest edition of Asia Video...

MUMBAI: 2018 could have been easily dubbed as the Indian year digital or OTT, with its chaotic growth continuing and multi-million dollars being poured into programming...

MUMBAI: As per a new report by Media Partners Asia (MPA), the pay TV revenue in Asia will top $56 billion in 2018. This will continue...

MUMBAI: The terminator…, oops sorry, the disruptor is back. And, this time it is targeting India’s multi-billion-dollar cable TV and DTH businesses with promises to unleash...

MUMBAI: With telcos handing out data at cheap rates in various package sizes under innovative schemes, mobile data consumption has increased rapidly in India in the...

MUMBAI: New research on the pay-TV channel ecosystem shows India powering revenue and profit growth for regional pay-TV broadcasters in Asia Pacific. Revenue for pay-TV channel...

MUMBAI: Pay-TV players in Asia-Pacific region are girding up their loins to integrate online video into their service bouquets and recalibrate owing to broadband growth while...

“There’s only one war that matters. And it is here”. So reads the caption of HBO’s official trailer for the blockbuster sixth episode of ‘Game of...

MUMBAI: Media Partners Asia (MPA) estimates that the Indian online video industry generated approximately US$ 230 million in total sales in 2016, and is on course...

MUMBAI: The TV, film and video production sector in Asia is set to enter a new cycle of growth, according to a new report from Media...

MACAO: When the hundred billion dollar man, GroupM Global Chairman Irwin Gotlieb, says that the role of the media is to create content, it’s time to...

MACAO: When the hundred billion dollar man, GroupM Global Chairman Irwin Gotlieb, says that the role of the media is to create content, it’s time to...

MUMBAI: Media Partners Asia (MPA) and Shanghai TV Festival (STVF) announced a partnership to collaborate on the first ever knowledge exchange forum at the STVF in...

MUMBAI: Media Partners Asia (MPA) and Shanghai TV Festival (STVF) announced a partnership to collaborate on the first ever knowledge exchange forum at the STVF in...

MUMBAI: According to a report by Media Partners Asia (MPA), Asia Pacific online video revenue is expected to reach US$35 billion by 2021, an average annual...

MUMBAI: According to a report by Media Partners Asia (MPA), Asia Pacific online video revenue is expected to reach US$35 billion by 2021, an average annual...

MUMBAI: The Indian advertising market is poised to grow fastest over the next five years in the Asia Pacific region at a rate of 10.7 per...

MUMBAI: The Asia-Pacific pay-TV industry will grow at a 6.6 per cent average annual rate from 2014 to 2019, according to a new report, Asia Pacific...

MUMBAI: Tata Sky has partnered with IBM to launch new mobile solutions that will enable it to reach new markets, and improve customer service and responsiveness...