Connect with us

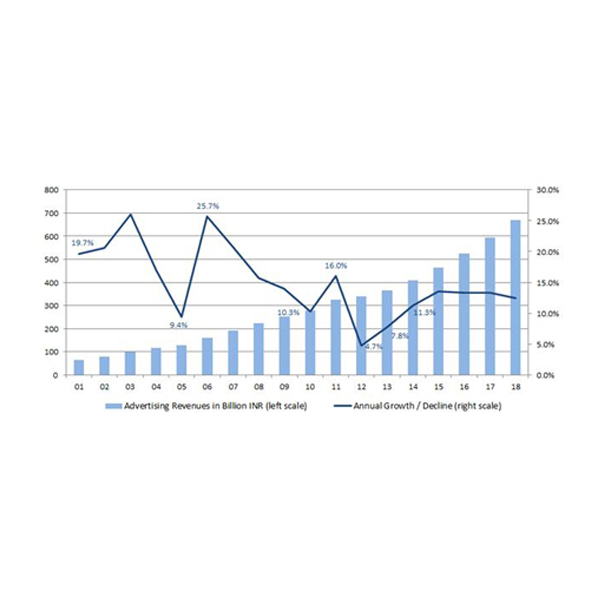

MUMBAI: Going by the recently released half yearly Adex report by IPG Mediabrands India, the Indian advertising industry is growing at a rate of +16.2 percent...

MUMBAI: Going by the recently released half yearly Adex report by IPG Mediabrands India, the Indian advertising industry is growing at a rate of +16.2 percent...

MUMBAI: In its latest report on the global advertising marketplace, Magna Global estimates that media owner advertising revenues grew by +3.2 percent in 2015 to $503...

MUMBAI: The year is coming to an end, and it’s time to introspect. Various studies will be done to review how the years went by. Was...

MUMBAI: Folks in advertising, there’s reason to cheer. The Indian advertising market is going to grow at a healthy 7.8 per cent in 2012-2013, outpacing its...

MUMBAI: The Indian ad revenue market is projected to grow 8.7 per cent in 2013 with internet leading the growth at 31.2 per cent, says Magna...

MUMBAI: Guess whom the huge US television networks are most at risk from? None other than their fans. As fans increasingly turn towards downloaded video content...

This will close in 10 seconds