Connect with us

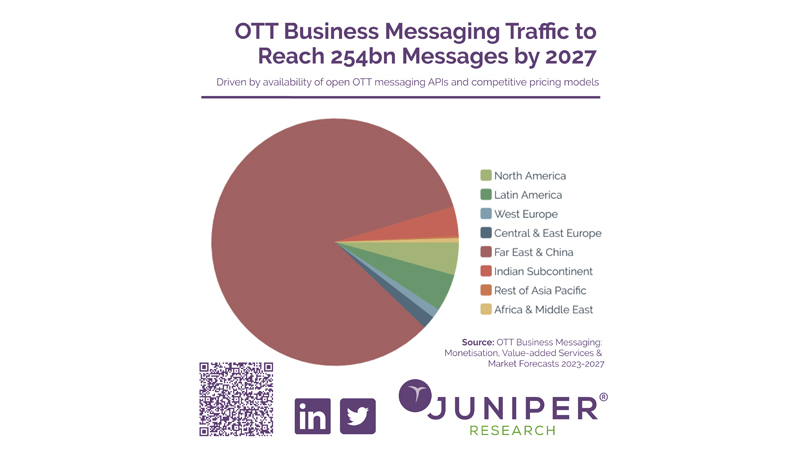

MUMBAI: Looks like Whatsapp is about to have the last word quite literally. A new study by Juniper Research predicts that over-the-top (OTT) business messaging will...

MUMBAI: It’s not just rockets taking off satellite broadband revenues are too. A new study by global tech strategist Juniper Research predicts that fixed satellite broadband...

HAMPSHIRE: The subscription economy is heading for $1.2 trillion by 2030, up 67 per cent from $722 billion this year, according to Juniper Research. But consumers...

MUMBAI: In a new research, the UK-based Juniper Research has forecasted that unique viewers of eSports (competitive playing of video games) and Let’s Plays content (tutorials...

NEW DELHI: New data from UK-based Juniper Research has found that advertising spend on FVoD (free video on demand) content, such as media on YouTube and...

NEW DELHI: The mobile gaming market is likely to generate revenue of $28 billion by 2016 – a growth of over 38 per cent on the...

MUMBAI: Juniper Research predicts that the mobile entertainment market is set for a new era of rapid growth as 3G environments become more commonplace, applications built...

MUMBAI: The increasing influence of mobile video enabled on 3G networks will drive the uptake of many mobile sports, leisure and information services over the next...

MUMBAI : Mobile sports information and entertainment services are expected to take an increasing share of the global mobile sports, leisure and information content (infotainment) market...

MUMBAI: The number of mobile phone users subscribing to streamed or broadcast TV services is expected to reach 65 million worldwide by the end of 2010....

This will close in 10 seconds