NEW DELHI: From “let there be voluntary CAS” to “if you must mandate CAS stay out of the pricing mechanism”. That could well sum up how the view of the broadcast sector in general to the prospect of the rollout of addressability has changed from the situation that existed back in 2003.

That was a recurring theme during the informed discussions that went on in the post-lunch session of the Indian Broadband Digital Networks Forum organised by Indiantelevision.com and Media Partners Asia in the capital yesterday. The two sessions – The Strategic Imperative: Consolidation & Convergence and Ground Realities: Content Distribution & Technology flowed seamlessly from one to the other taking further the cues that had been provided in the morning’s keynotes.

Unless pricing was elastic, it was a non-sustainable business model not just for the pay channels but for the cable service providers as well, was the view expressed by Raghav Sahgal, CBO, Converse. Speakiing during the morning keynote, John Malone-controlled Liberty Media board member Shane O’Neill suggested that a better formula for the government to consider might be that the baseline or lifeline service (basic tier?) be given maximum spread while the rest should be left to the market to determine.

Interestingly, that was the sentiment off the Orissa-based MSO Ortel Communications’ Jagi Mangat Panda as well. Said Panda, “CAS is important and necessary. But the regulator entering into pricing issues is unviable for long.” Mandate CAS but stay away from pricing, she offered. Panda also spoke of the need for a level playing field on issues like foreign investment similar to what the telcos enjoyed for all players in the broadcasty sector.

ADAPT OR PERISH:

Speaking on the issue of the shift to digital, HSBC Securities’ Sandeep Pahwa pointed out that “consolidation and building of scale is important but not a necessary recipe for success.” The ability to innovate according to the dynamics as determined by Indian situation was the critical factor, according to Pahwa. “Adapt or perish. The mantra is continual innovation,” Pahwa said.

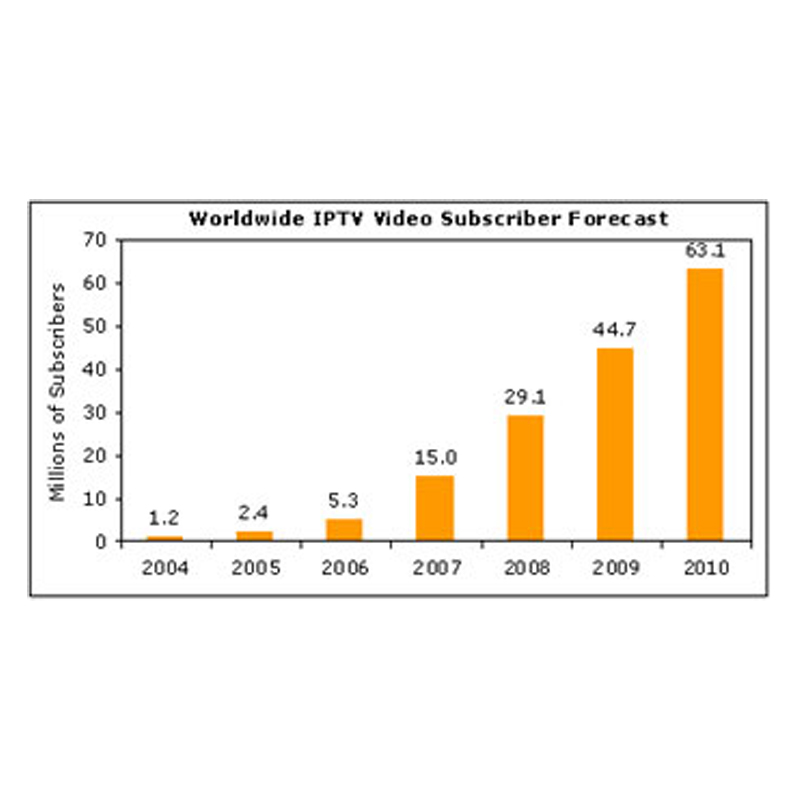

Another point that came through in the discussions was that in the move towards digital delivery, the real battle in the short to mid term would be between cable and DTH. “IPTV is a real challenge in an emerging market like India,” said Comverse CBO Raghav Sahgal.

According to Pahwa, DTH will compete on reach (cable dark areas in particular) and service. However, where cable service providers have got it right, there is a clear advantage in their favour.

WWIL’s JS Kohli said, “CAS is the trigger that will actually facilitate the move towards convergence.”

Tata Sky’s Vikram Kaushik said while in the medium term quality of service would be the key differentiator that DTH offered, going forward, once transponder limitations haad been overcome some element of exclusivity would come into play. 80 per cent of programming will be across platform and 15 per cent will be exclusive, Kaushik said.

Speaking on the content provider’s side Star India’s Paritosh Joshi said, “Star’s content for the mass audiences will remain the primary focus. We will look for opportunities – mobile in particular is something we’re particularly gung ho about. That’s something we’re already actively looking at.”

“A marginal higher value consumer may exist and these we will address,” Joshi said.

Speaking about the impact CAS would have Hathway MSO’s K Jayaraman said, “CAS is going to be painful in terms of investments required. If the first phase of CAS goes well then the funding is going to be a challenge.”

Incable’s Ashok Mansukhani offered, “We need to put in a lot of money to upgrade ourselves as well as LCOs. We believe in 100 per cent transparency.”

On the scope for IPTV, Tandberg Television’s Alan Delaney said, “There is plenty of space in the market for everybody.”

Bharti Televentures’ Sriram TV was clear that staying out of content creation was the way to go for telcos. Said Sriram, “Focus on what you’re best at. Bharti has taken its learnings from the experiences of Singtel / Vodafone in the UK as examples of networks that went into too many areas and lived to regret the decision. Network convergence, device convergence and industry convergence is what we are looking at. Bharti has content tie-ups with all the pay channels.”

HFCL’s Surendra Lunia, however, said, “We will evaluate according to opportunity.”

Another problem for broadband is that technical skill sets need to be sorted out before value added services can be rolled out, said Jayaraman. This statement coming from the head of a cable MSO who has 100,000 registered users reflects on the difficulties that lie ahead for introduction of IPTV in particular.

However, Mansukhani was more optimistic on that front: “It is a dynamic growth oriented business. Broadband adding significantly in the next three years.”