Connect with us

GREATER NOIDA: Coforge has launched Data Cosmos, an AI-enabled, cloud-native data and analytics platform aimed at helping enterprises overhaul fragmented data estates and accelerate digital transformation....

A high-profile hospital visit can make cashless treatment look effortless. The reality for most people, however, is far messier, especially when navigating policy wording, network rules,...

Owning a vehicle comes with more than just the freedom to travel at will—it also comes with legal responsibilities. One of the most important is having...

MUMBAI: The Advertising Standards Council of India (ASCI) has given its influencer guidelines a much-needed shot in the arm — and a dose of financial clarity....

Commercial vehicle insurance is a kind of policy designed to protect businesses and individuals who use vehicles for commercial purposes. Unlike private vehicle insurance, it offers...

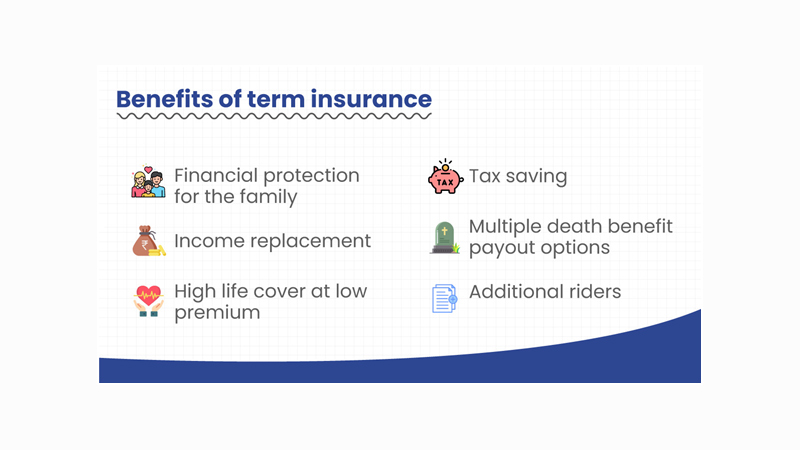

Introduction to Term Insurance When it comes to securing the future, we are often reminded to plan for unforeseen circumstances. While talking about making investments, things...

Mumbai: Future Generali India Insurance marked International Women’s Day 2024 with the launch of a trailblazing initiative, the #DontBeAPlus1 campaign. Aimed at raising awareness about the...

Mumbai: Capri Global Capital Limited (CGCL) received a composite Corporate Agency license from the Insurance Regulatory and Development Authority of India (IRDAI) in December 2023 to...

Mumbai: Capri Global Capital Limited (CGCL) has received a Composite Corporate Agency license from the Insurance Regulatory and Development Authority of India (IRDAI) to distribute life,...

Mumbai: Niva Bupa Health Insurance, formerly known as Max Bupa Health Insurance, has launched a digital campaign to kickstart the Diwali festivities. The campaign, conceptualised and...

Mumbai: PhonePe has launched an integrated multi-media brand campaign focused on tension-free motor insurance renewals. The campaign drives awareness around the benefits of renewing motor insurance...

New Delhi: Niva Bupa Health Insurance, formerly known as Max Bupa Health Insurance, has signed Leo Burnett as its advertising agency partner. The account was won...

Mumbai: The ministry of finance has released a special music video called “Thank You” as part of the “Azadi ka Amrit Mahotsav” celebrations, which mark the...

Mumbai: Hybrid digital agency from Dentsu Creative India WATConsult has released its latest issue of monthly WATPapers titled ‘Consumer’s outlook towards health insurance.’ The report explores...

Mumbai: Online insurance marketplaces Policybazaar unveils its newest brand campaign featuring actor Pankaj Tripathi to raise awareness quotient regarding the significance of term life insurance. Presented...

Mumbai: Bajaj Allianz Life Insurance has launched an educational initiative under the theme “Life Goal Mantras”. The campaign aims to simplify personal finance and insurance concepts...

Mumbai: Good dogs can make bad decisions. With this thought in mind, Future Generali India Insurance (FGII) has launched a digital campaign called ‘Oh My Dog!’...

Mumbai: Acko, a new-age insurance company has released a print campaign with Ogilvy India to communicate the advantage of using its paperless services over traditional insurance providers,...

Mumbai: Digital payments company PhonePe has announced its latest brand campaign “Tension chhodo, Insurance lo” to make customers aware of how insurance can make life easy...

New Delhi: Stepping up to take care of its employees during the devastating second wave of Covid2019, AI-driven online automobile marketplace Droom on Thursday announced Rs one...

MUMBAI: UK producers are in discussions with the government to extend the landmark £500 million ($664.6 million) Covid2019 insurance scheme for film & TV production. Media...

MUMBAI: The pandemic may have halted production activities, but the costs are mounting, especially the rent, according to ANM Global managing partner Nidhish Mehrotra. He was...

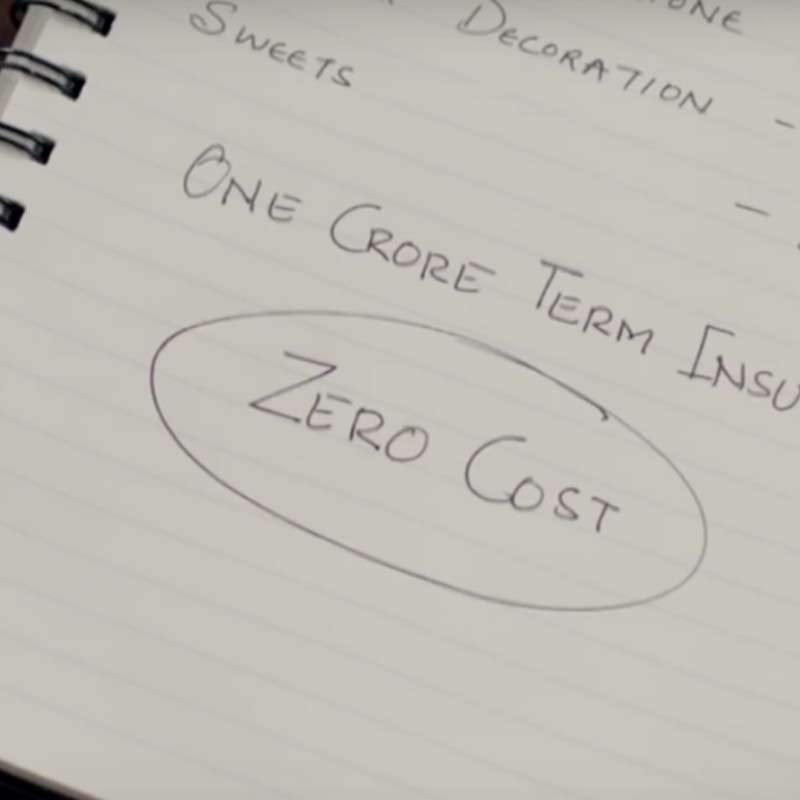

MUMBAI: This festive season, Exide Life Insurance took the unconventional route to reign in a Happy Diwali with its Zero Cost Term Insurance. Through its latest...

MUMBAI: Online insurance company, Aegon Life Insurance, has appointed Saba Adil as the chief operating officer with a mandata to drive the strategic goals and operating...

MUMBAI: Life insurance ads with depressing thoughts about the future and forcing you to invest to avoid gloomy situations like an accident, health failure, etc aren’t...

MUMBAI: BFSI equals boring. That is usually what people think about anything to do with banking, financial services and insurance (BFSI). You may have witnessed how...

MUMBAI: Bajaj Allianz General Insurance has launched a one-month digital campaign #HealthKaNotification, to create awareness about the importance of Health Insurance amongst consumers. Conceptualised and executed...

MUMBAI: Bajaj Allianz General Insurance has launched a one-month digital campaign #HealthKaNotification, to create awareness about the importance of Health Insurance amongst consumers. Conceptualised and executed...

MUMBAI: The Union Government has radically liberalized the FDI regime today, with the objective of providing major impetus to employment and job creation in India. The...

MUMBAI: The Union Government has radically liberalized the FDI regime today, with the objective of providing major impetus to employment and job creation in India. The...

Mumbai: Bloomberg TV India, the country’s leading English business news channel, will unveil the show “Wealth Manager”. The first ever show on Wealth management will highlight...

NEW DELHI :Big Boy Toyz, the specialized dealer of pre-owned and exotic luxury cars now gives you not one, but 10 reasons to buy from their...

BANGALORE: Aviva Life Insurance has embarked on expansion plans. The company is opening 13 new branches in the year 2005, taking its current strength from 24...

As the curtains fall down on 2004, the all important figures are also out — that of the Top 10 categories of advertisers on television and...

MUMBAI: CNBC goes vroom vroom, this time with consumer angle in mind. Starting today, 10 June at 10:30 pm, the business channel will be getting behind...

he multiple levels and multi-point Service Tax imposed on the Entertainment Industry is making survival difficult for the small content producers. Presently, the Entertainment Industry...