Connect with us

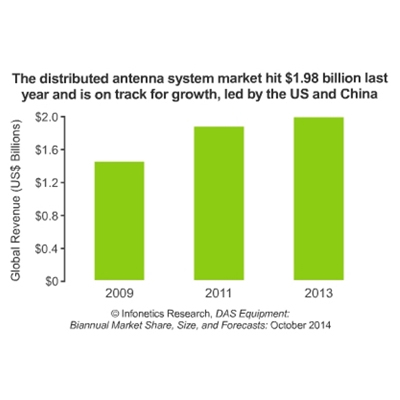

NEW DELHI: The market for distributed antenna system (DAS) rose 11 percent in the first half of 2014 to $1.1 billion. Infonetics Research shows that...

NEW DELHI: The Asia Pacific region has shown major growth of six per cent year-over-year in the telecom/datacom equipment and software revenue as against 4.5 per...

NEW DELHI: The largest growth in mobile broadband between 2012 and 2013 was in the Asia Pacific region, while it fell in Europe. According to...

NEW DELHI: The global business and residential VoIP services market rose eight per cent in 2013 to $68 billion and are expected to yield a revenue of...

MUMBAI: The emerging markets are driving growth in the pay-TV market. That is what a recent paper released by Infonetics Research says. Markets such as India,...

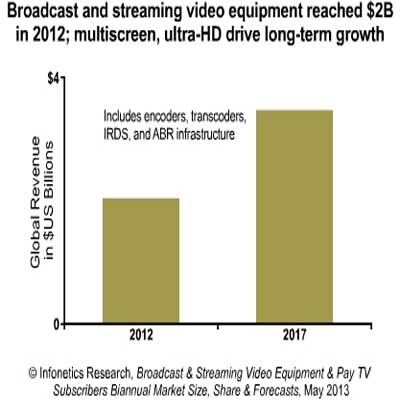

NEW DELHI: Broadcast and streaming video equipment market is likely to grow 12 per cent in 2013 from two billion dollars in 2012. According to...