Connect with us

MUMBAI The advertising world, it seems, refuses to read the room. Whilst economists fretted over trade wars and geopolitical chaos, the ad business simply cracked on....

New Delhi: Advertising revenues swung back to a healthy growth rate of 14 per cent in 2021, rising from Rs 577 billion to Rs 657 billion....

New Delhi: Global advertising spend is expected to rise 12.6 per cent during 2021 as a whole to reach $665bn, according to WARC Data’s report tracking...

MUMBAI: Exceeding user addition forecasts, Netflix’s first quarter (Q1) earnings were in line with expectations while revenue bettered estimates. Revenue grew by 43 per cent year...

MUMBAI: Publicis Media Company Zenith has just released its new Advertising Expenditure Forecasts in which it predicts that global ad expenditure will grow 4.4 per cent...

MUMBAI: Publicis Media Company Zenith has just released its new Advertising Expenditure Forecasts in which it predicts that global ad expenditure will grow 4.4 per cent...

MUMBAI: The year 2014 saw the biggest Lok Sabha elections held in the country with Bharatiya Janta Party winning with a majority giving people a hope...

MUMBAI: Google will sell more mobile advertising than the rest of its rivals combined for the second straight year, according to a new forecast that highlights...

MUMBAIi: Media research and consulting firm Ormax Media has announced the launch of Opening Week Average (OWA), a scientific launch viewership forecasting model for Hindi general...

MUMBAI: Last year, the US telecom market grew at its fastest rate since 2000, showing that the drive towards convergence continues to stimulate the telecommunications industry,...

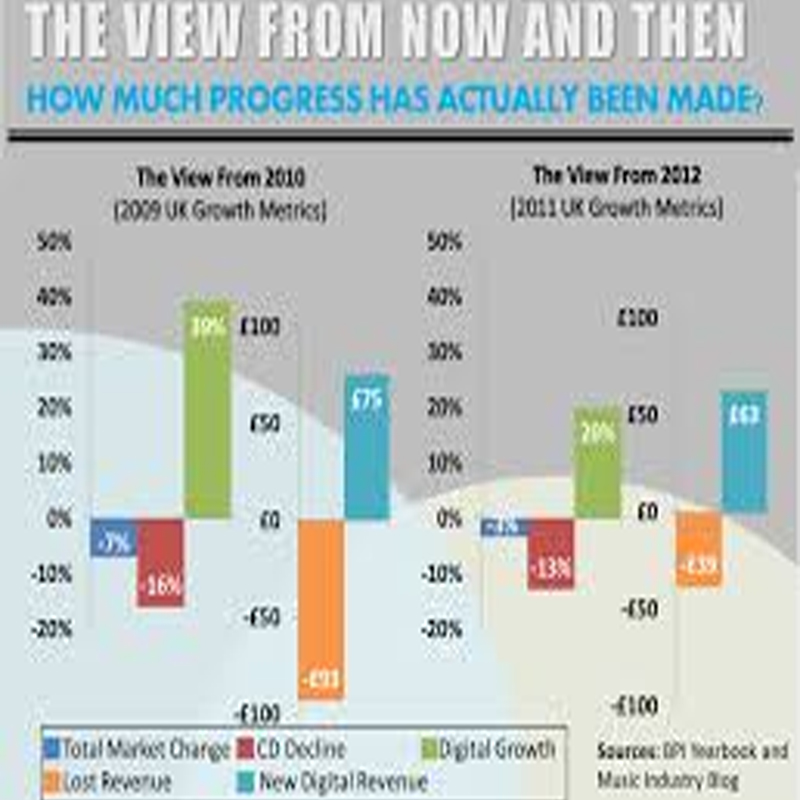

MUMBAI: A new report by media researchers Screen Digest, Online Music in Europe: Market Assessment and Forecast predicts that rapidly growing online music sales in Europe...

MUMBAI: Keeping with its annual tradition, Etc’s Kahani Kismat Ki will showcase the annual forecast of all the 12 star signs. Kahani Kismat Ki will be...

MUMBAI: With rising oil prices, the dollar downslide and the US current account deficit being potential causes for concern in 2005, media buyer Carat, a unit...

MUMBAI: UK broadcaster the BBC is hoping that the changes it has recently made to the Entertainment and Comedy Commissioning team will help put the window...

ARIZONA: With digital terrestrial transmission gaining acceptance worldwide, high-tech market research firm In-Stat/MDR forecasts a boom in the sale of DTV sets. According to In-Stat/MDR, with...