Connect with us

You may need sizeable funds to scale a business, renovate your home, or consolidate existing liabilities. In such situations, selling assets may not always be the...

In today’s evolving financial ecosystem, a loan against property (LAP) has become one of the most reliable instruments for accessing large sums of money. Whether it...

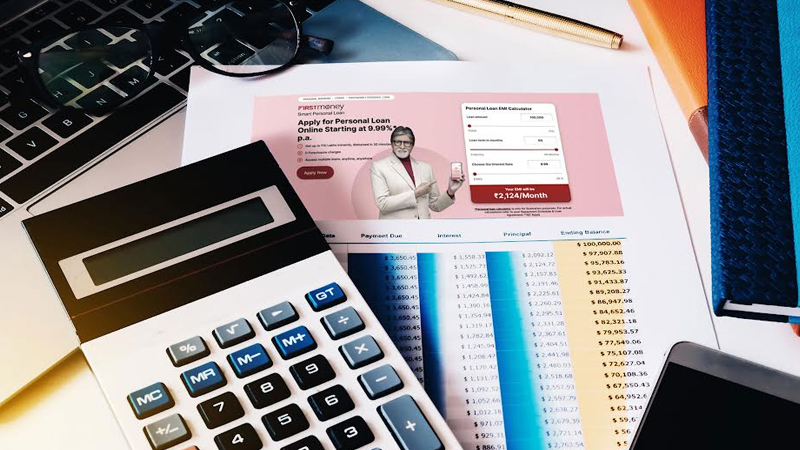

In today’s digital world, applying for a personal loan is quicker than ever. But before you commit to borrowing, it’s essential to know how much you’ll...

Choosing the right funding option is tricky when you need funds to handle an emergency or fulfil a dream. Personal Loans and instant loans are the...

Diwali, the festival of lights, is a time of celebration, joy, and togetherness. It signifies the victory of light over darkness, and good over evil, and...

Mumbai: With the festive season transpiring in full swing, Bajaj Finance in collaboration with Bajaj Finserv Direct Ltd has launched its Diwali campaign ‘EMI hai na’ to offer discounts...

MUMBAI: Bajaj Finance Ltd, the lending arm of Bajaj Finserv launches #FitForLife campaign to encourage individuals to achieve their New Year fitness resolutions. The company will...

MUMBAI: Bajaj Finance, the lending arm of Bajaj Finserv has launched the digital campaign to drive awareness around its EMI Network. The campaign aims towards highlighting...

MUMBAI: Bajaj Finance Ltd, the lending arm of Bajaj Finserv has launched a campaign #FitForLife Fest to offer fitness and wellness products on no cost EMI...

MUMBAI: The Telecom Regulatory Authority of India (TRAI) late last evening issued two tariff orders prescribing standard tariff package for set top boxes (STBs) for digital...

MUMBAI: EMI Music and UK pubcaster the BBC’s commercial arm BBC Worldwide have struck a deal that will see thousands of hours of pop and rock...

MUMBAI: MediaCorp Radio has announced the launch of Singapore’s hit music station Y.E.S. 93.3FM, which is the first Chinese language radio station to be made available...

MUMBAI: EMI Group would make its music catalog available to the first advertising supported peer-to-peer service as the entertainment industry embraces the same technology that once...

MUMBAI: The international TV channel dedicated to fashion – Fashion TV (FTV) together with EMI Music Southeast Asia have formed a strategic alliance whereby the music...

MUMBAI: The music industry is in consolidation mode battered and bruised as it is by Internet music sharing, poor retail revenues and competition with other sources...

MUMBAI: From today, Channel [V] is wholly a Star subsidiary. The Hong Kong-based Star TV, a unit of media baron Rupert Murdoch’s News Corp Ltd, today...