Connect with us

NEW DELHI: Three Indian films share seven nominations among 42 films nominated in 14 categories for the Asian Film Awards this year. Haider has four nominations. In...

MUMBAI: After making a documentary about Chinese constitution, Shen Yongping , a Chinese filmmaker, has been sentenced to one year in prison for “illegal business activities”....

MUMBAI: The Committee to Protect Journalists (CPJ) has identified that 220 journalists are in jail around the world in 2014. This is an increase of nine...

MUMBAI: Aadarsh Pvt. Ltd. has joined hands with leading publisher Sarasavi Book Shop Pvt. Ltd., to launch Purple Turtle story books in Sinhala Language in Sri...

NEW DELHI: Chinese censors have blocked the website of the British Broadcasting Corporation (BBC) as tensions rise in Hong Kong between pro-democracy protesters and police. ...

MUMBAI: It was in the month of June when Google announced that it will shut Orkut down at the end of September 2014. And now,...

NEW DELHI: The 3rd Asian Film Summit, part of the 39th Toronto International Film Festival (TIFF) will have an additional masterclass with China’s Ning Hao this year. The...

MUMBAI: Tourism New Zealand says the industry has turned a corner with the release of ‘Tourism 2025 – Growing Value Together/Whakatipu Uara Ngatahi’ and its aspirational...

MUMBAI: Digital pay TV is slowing down in Asia. That was the key takeaway from Media Partners Asia (MPA) executive director Vivek Couto’s annual report on...

MUMBAI: In a recent development, Swarovski has promoted Francis Belin to take a bigger role in the company. Belin who has been in charge of...

NEW DELHI: India stands at sixth position in terms of spam distribution in February 2014, while China has been ranked number one. According to Kaspersky...

KOLKATA: The people in Kolkata seem to be addicted to the new ways of shopping. Star CJ Alive, a home shopping channel from the house of...

MUMBAI: Global advertising expenditures were up 3.2 per cent in the third quarter of 2013 for year-over-year period, driven largely by Asia Pacific’s expanding powerhouse ad...

MUMBAI: Universal Pictures has announced dates on three upcoming high-profile projects and it means more Minions in the coming years, along with Grinch; the third installment...

MUMBAI: China will launch high-definition terrestrial digital TV broadcasts in 2008. A five-year (2006-2010) guideline on cultural development has been published. Media reports inform that China...

MUMBAI: When it comes to technology, China is one of the leading Asian countries in the world that comes to mind. So it’s no surprise when...

MUMBAI: For a few years now, animated shows like SpongeBob SquarePants, have entertained the young viewers almost across the world. Now, many such popular Nickelodeon children’s...

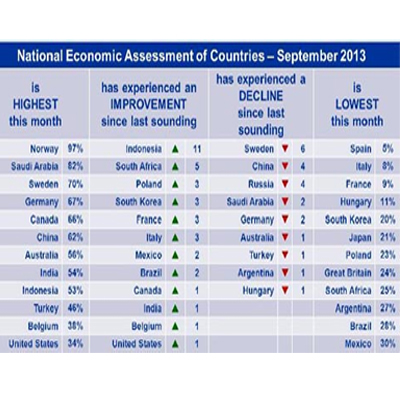

MUMBAI: India’s economic confidence revived substantially due to healthy farm output, a sharp boost in exports and narrowing of current account deficit, according to a report...

NEW DELHI: India has ranked fourth in phishing attacks in the third quarter of 2013, said RSA, a division of EMC. India received three per cent...

MUMBAI: Women are on top, literally! The 2013 search trends released by Bing that includes search data from Australia, Brazil, Canada, China, France, Germany, India, Italy,...

MUMBAI: India is just a year into the process of digitisation, and, in another year, it is quite likely all of the nation’s 100-odd million cable...

MUMBAI: The Digital Asia Festival Awards, honouring the best digital marketing communications across Asia Pacific, has announced this year’s shortlist. Chaired by Jason Kuperman, vice...

MUMBAI: Production company Ivanhoe Pictures was launched in Toronto earlier this year by Ivanhoe Capital Corporation principal Robert Friedland, GreeneStreet president and co-founder John Penotti, and...

NEW DELHI: Microsoft, which had officially acquired Skype in 2011, is taking over Skype’s operations in China from 24 November. Skype China is still being run...

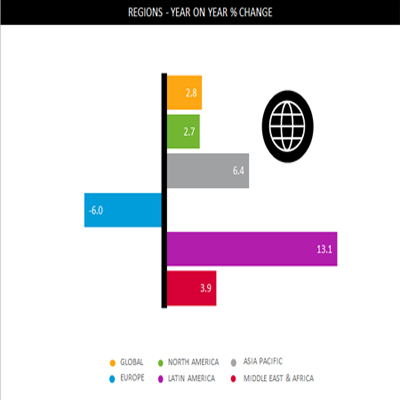

NEW DELHI: Ad spends grew by a substantial 6.4 per cent in the first half of 2013, making it the largest growth among different regions of...

NEW DELHI: Even as India continues to produce the largest number of films, China has shown a major growth with total box office revenue for the...

MUMBAI: Are the winds of change blowing in probably what is the most hypercompetitive and protected media market in the world after China? It looks likely...

MUMBAI : A new global study from CareerBuilder shows that a typical day in the office is not so typical across the globe: When you look...

MSLGROUP, Publicis Groupe’s strategic communications and engagement consultancy, was named the ‘Best Corporate Consultancy in the World 2013’ by The Holmes Report, one of the most...

NEW DELHI: Even as India ranks third in terms of the highest number of internet users in the world after US and China and the number...

Forevermark, the diamond brand from the De Beers Group of Companies, announced its collaboration with British fashion designer, Gareth Pugh today. On the occasion, Mr. Sachin...

MUMBAI: Global ad spend has hiked 2.8 per cent on a year-over-year basis for the first half of 2013, according to Nielsen’s Global AdView Pulse report,...

MUMBAI: China’s Huading awards are set to see some high profile Hollywood actors such as Quentin Tarantino, Nicole Kidman and Nicholas Cage. The award night is...

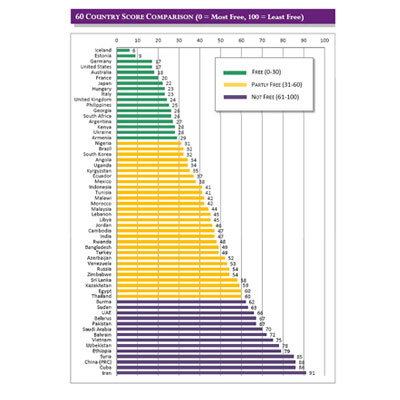

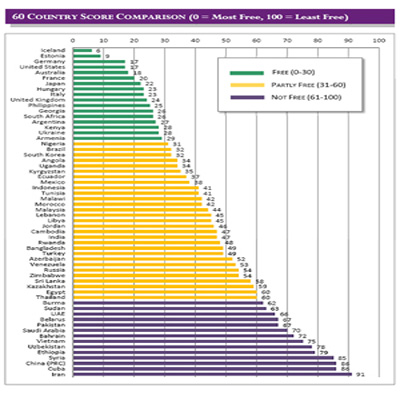

NEW DELHI: India is 35th among sixty countries in the Freedom on the Net 2013 report. The annual report is carried out by Freedom House, an...

NEW DELHI: India is 35th among sixty countries in the Freedom on the Net 2013 report. The annual report is carried out by Freedom House,...

MUMBAI: Seven in ten (69 per cent) Indians admit they say things in that they would not say voice-to-voice or person-to-person; compared to 43 per cent...

MUMBAI: India’s economic confidence recovered marginally but it remains uncomfortably uncertain as food inflation remains sky high and economic growth dwindling, according to a report by...

MUMBAI: Beijing has made the landmark decision to lift a ban on internet access within the Shanghai Free-trade Zone to foreign websites considered politically sensitive by...

NEW DELHI: ValuAccess, a leading provider of gift cards and loyalty programs in Asia has launched gift card programme for Country Inn & Suites, Sahibabad. ValuAccess...

Vinod Ganatra, an independent award winning film maker from Mumbai, is a member of the international jury of the 12th China International Children’s Film Festival to...

NEW DELHI: In its mission to offer distinct and enriching content for children, Discovery Kids presents 1001 NIGHTS – an animated series that brings the most...

NEW DELHI: Steven Spielberg’s 1993 dinosaur spectacular Jurassic Park had a huge opening when it was released in its first 3-D version in China this week....

MUMBAI: Star India has scored the rights to carry the upcoming 2014 Winter Olympics from Sochi and the 2016 Summer Olympics from Rio across seven South...

MUMBAI: In an effort to thwart imported animated flicks, the government has denied permission to release the movie in the country. The previous installment was also...

MUMBAI: Paramount Pictures and Michael Bay have added Asian superstar Han Geng to the cast of Transformers 4. He would be joining the likes of Chinese actress...

NEW DELHI: Chinese cinema is expected to be given the pride of place at the International Film Festival of India in Goa in November this year....

MUMBAI: Pixar‘s Monster‘s University, a sequel to the 2001 Monster Inc. is slated to release in China as the curtain raiser of the Shanghai International Film...

MUMBAI: After a much eagerly awaited Super-Man reboot, Zack Synder‘s Man of Steel is all set to release on June 14. The movie will also be...

NEW DELHI: The 12th New York Film Festival will include a major tribute to Taiwan exploitation cinema and close with the Taiwan-produced kung fu-musical The Rooftop....

MUMBAI: As part of a new partnership between DreamWorks Animation and Sands China, the studio will debut its DreamWorks Experience at the Sands Cotai central resort...