Connect with us

MUMBAI: He came, he saw, he was not happy with what he saw. That reportedly sums up what was the feeling that information and broadcasting joint...

MUMBAI: Mumbai based cable operators have expressed disappointment over the recent comments of I&B secretary Pawan Chopra that indicate that the government might soften its stand...

NEW DELHI / MUMBAI: Has CAS finally degenerated into unconditional uncertainty? The joke seems to be coming true. But, say government officials, things may not turn...

In all the confabulations around CAS, one assumption that has generally made is that broadly speaking the cable fraternity stands as one. Indiantelevision.com met a group...

MUMBAI: Is the “non-negotiable” deadline of 14 July for the rollout of conditioinal access in the four metros about to be extended? Looks likely. ...

NEW DELHI: The cable fraternity today went before the politicians to make a spirited case for implementing the conditional access system . They were snubbed at...

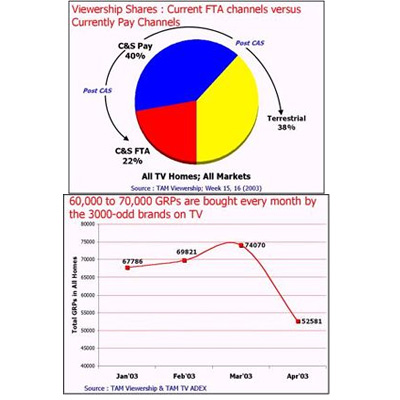

MUMBAI: India’s First ever CAS Summit on the TV Advertising Scenario Post CAS will be held on 4 July at the Hyatt Regency Mumbai. Hosted...

NEW DELHI: The Indian government is not averse to the idea if the main channels, including the sports and entertainment ones like Star Plus, Zee TV,...

MUMBAI: When the cable industry committed on Saturday to provide all channels (pay and FTA) available for a total monthly tab of Rs 222 (exclusive of...

MUMBAI: The political tango around the introduction of conditional access in India just refuses to simer down. The Delhi Government on Saturday opposed the implementation of...

NEW DELHI: CAS is indeed turning out to be better than any of the soaps that most entertainment channels air with unexpected twists and turns. ...

MUMBAI: Although ETC Networks had earlier announced that its channels etc and etc Punjabi would become free-to-air after 14 July 2003, there is a possibility that...

MUMBAI: Although ETC Networks had earlier announced that its channels etc and etc Punjabi would become free-to-air after 14 July 2003, there is a possibility that...

MUMBAI: The implementation of the conditional access system (CAS) rollout could have created several opportunities for the cable trade and made life easier for the consumers....

Theres a lot of wishful thinking going on in government. That it can and should control pricing. That too, in a country which is moving from...

NEW DELHI: MSOs now want to fix the price of pay channels and offer an invitation price of Rs 200. The cable fraternity is not giving...

MUMBAI: TV producers are about to be hit with another whammy. Bad sentiment for media on the stock market aside, the implementation of conditional access systems...

NEW DELHI: Further to its drive to educate and inform consumers and partners on the advantages of CAS, Zee Turner Ltd, the distribution arm of Zee...

MUMBAI: The Shiv Sena stance on CAS remains unsoftened. Shiv Sena supremo chief Bal Thackeray, who had reportedly eased up on his objections to conditional access...

MUMBAI: The Rajan Raheja promoted Hathway Cable & Datacom (Hathway), in which Star India has a 26 per cent stake, is all set to roll out...

Conditional Access System (CAS) is definitely changing the name of the game for the national broadcaster too. Last Saturday, Doordarshan director general Dr SY Quraishi met...

MUMBAI: A delegation of cable operators of Delhi met chief minister Mrs Sheila Dikshit yesterday and urged her to support the implementation of conditional access system...

MUMBAI: “The post-CAS scenario – good interplay of market forces; healthy intervention of the government!” These were the words with which information and broadcasting minister Ravi...

NEW DELHI: Facing opposition from Shiv Sena Supremo Bal Thackeray on the Conditional Access System, information and broadcasting minister Ravi Shankar Prasad is likely to meet...

MUMBAI: With the countdown to the conditional access rollout deadline well and truely on, the information and broadcast ministry is attempting to “educate” the public on...

MUMBAI: If there was an element of speculation earlier it is now official. A watered down version of French fashion channel FTV will be what is...

NEW DELHI: Consumer Coordination Council to information and broadcasting ministry: the conditional access system (CAS) is still not consumer friendly and should be implemented only after...

These days information and broadcasting minister Ravi Shankar Prasad does not look uncertain as he did some months back when he was allocated the I&B ministry...

A study carried out by Starcom Worldwide and Hansa Research Group to understand the viewer‘s viewpoint on CAS shows that not only is the consumer aware...

MUMBAI: Conditional access could bring in inventory pressures for free to air channels if demand for their air-time explodes. This is the conclusion drawn by TAM...

NEW DELHI: The Indian government today further tightened the screws on the broadcast and cable industry on conditional access system (CAS) by issuing a notification that...

MUMBAI: The Indian Broadcasting Foundation (IBF), which has been riven recently by persistent reports of major rifts between pay and free-to-air lobbies within it, sought today...

MUMBAI: Shiv Sena supremo and an important ally of the NDA government, Bal Thackeray, has warned the government that it will find its decision to go...

NEW DELHI: The Indian government wants to ensure a smooth rollout of conditional access system (CAS) in the first phase in the four metros — maybe...

NEW DELHI: The Subhash Chandra-promoted Zee Telefilms is very bullish on certain aspects of conditional access system (CAS) and feels that it is rightly positioned to...

MUMBAI: Cable Quest, a cable and satellite publication, has announced a seminar CAS Myth & Reality in The Park Hotel in New Delhi on 6 June....

MUMBAI: Conditional access may exist in Mumbai only when quoting legalese, but it is taking the legal position in mind that a Mumbai civil court on...

HTMT group director and CTO (chief technology officer) KV Seshasayee is the man in the centre of action. He is the man who will spearhead the...

NEW DELHI: Even as the Indian government was initiating steps to see that the rollout of conditional access system (CAS) becomes as least bumpy as possible,...

NEW DELHI / MUMBAI: The government today took a huge step towards incentivising the rollout of set-top boxes into the market by cutting tariffs on the...

NEW DELHI: Stung by various politicians coming out against CAS, it is the turn of the cable operators to issue warnings. Reacting to Delhi chief minister...

MUMBAI:Hinduja group MSO INCableNet today announced it would brand its Conditional Access System (CAS) service as ‘INDigital’. For provision of CAS service to customers through Set...

Makers of software for the television industry will be among those to be hit by reduced budgets and a demand for more quality programming once CAS...

NEW DELHI: Zee Telefilms has set the cat amongst the pigeons by taking its set-top-boxes-for- rent scheme a step further. It asserts multiple TV homes consumers...

NEW DELHI: The battle to enter the set top boxes into Indian cable homes, in the four metros initially, is getting interesting. In order to send...

NEW DELHI: The CAS conundrum is getting more confounding and murky. Even as consumer organisations were attempting to put forward their case at a press conference...

NEW DELHI: India’s information and broadcasting minister Ravi Shankar Prasad is reported to have sought an appointment with Prime Minister AB Vajpayee today after returning from...

NEW DELHI:Just in case if it interests you all in the industry, India’s information and broadcasting minister Ravi Shankar Prasad is reported to have sought an...

NEW DELHI: Does the Bharatiya Janata Party (BJP), leading the coalition government in India, want the implementation of conditional access to be deferred? As of today,...

NEW DELHI: Even as the task force was discussing various aspects of conditional access system (CAS) and its implementation amidst media reports that the implementation may...