Connect with us

NEW DELHI: With the Government hoping to achieve complete digitisation of the cable television sector by the end of this calendar year, it is imperative that...

NEW DELHI: With the Government hoping to achieve complete digitisation of the cable television sector by the end of this calendar year, it is imperative that...

MUMBAI: The Indian advertising market is poised to grow fastest over the next five years in the Asia Pacific region at a rate of 10.7 per...

MUMBAI: Flip through business channels or newspapers and everyone seems to be talking about the Big Data. And in the current digital revolution phase, it...

MUMBAI: India’s entertainment and media industry is expected to double and grow to over Rs 2,27,000 crore by 2018 from Rs 1,12,044 crore in 2013, according...

MUMBAI: India’s direct-to-home (DTH) satellite pay-TV sector remains a growth oriented industry with significant potential for strategic and financial investors, according to a new report published...

MUMBAI: India’s low ad-spend-to-GDP ratio makes it one of the most promising ad markets globally, says IIFL’s Institutional Equities. In a Media sector report titled “India:...

MUMBAI: According to Euroconsult’s newly released report, “India Satcom Markets 2014”, India’s satellite communication sector has experienced significant growth over the past five years driven by...

BENGALURU: Bengaluru based Merino group’s agro division and ready to cook brand Vegit spends between 10-15 per cent of revenue on BTL activities. So far, a...

BENGALURU: At the opening ceremony of the FICCI MEBC (Media and Entertainment Business Conclave) – South, which was held on 29 and 30 October, Ministry of...

BENGALURU: The Digital March-Media and Entertainment in South India, a Deloitte-FICCI report was released on the eve of FICCI-MEBC 2013 in Bengaluru. The two day event...

NEW DELHI : Around 38-40 per cent of Indian population, between the age group of 14 and 25, who are on the verge of entering different...

Lex Witness- India’s 1st Magazine on Legal and Corporate Affairs today hosted a well-conceptualized The 2nd Annual Edition of Media, Advertising & Entertainment Legal Summit (MAELS)...

MUMBAI: India’s Entertainment & Media sector is expected to grow steadily over the next five years as per Confederation of Indian Industry-Price Waterhouse Cooper (CII-PwC) latest...

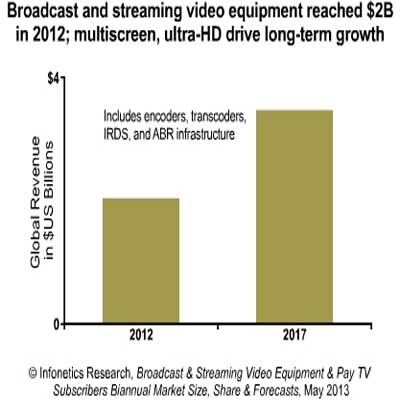

NEW DELHI: Broadcast and streaming video equipment market is likely to grow 12 per cent in 2013 from two billion dollars in 2012. According to...

MUMBAI: The total digital commerce market in India was valued at Rs 473.49 billion in December 2012 and is expected to grow by 33 per cent...

MUMBAI: Propelled by the government’s digitisation drive, pay TV revenues in India are projected to reach $17 billion by 2020 as opposed to the $7.8 billion...

MUMBAI: America‘s independent media research company BIA/Kelsey has forecasted the local media advertising revenues to climb from $132.5 billion in 2012 to $148.8 billion in 2017...

MUMBAI: Console continues to be the largest segment of the Indian gaming market. However, the Ficci KPMG report notes that its dominance is expected to reduce...

MUMBAI: Cable and satellite (C&S) television has posted double-digital growth in 2012, according to the latest figures by Indian Readership Survey (IRS). The C&S sector‘s reach...

MUMBAI: American Swan Lifestyle Company, a fashion and apparel-led lifestyle company, has got an investment of Rs 400 million for its Indian business, from global digital...

MUMBAI: Radio and cinema, which reported negative growth for the past three quarters, have shown positive compounded annual growth rate (CAGR) for the first time since...

BANGALORE: Titan Industries Limited youth fashion accessories brand Fastrack is targeting a CAGR of 50 per cent on its way to Rs 30 billion over the...

MUMBAI: The cable and satellite (C&S) sector continued its growth momentum, posting a CAGR of 13.9 per cent as its reach rose to 462.38 million, according...

MUMBAI: Cable & Satellite (C&S) and Internet are two sectors, which are continuously showing robust growth in the total reach. As per the Indian Readership Survey...

CANNES: Taking the cue delivered by CBS Corp. president and CEO Leslie Moonves at yesterday’s opening day main keynote, today’s keynotes harked on quality content as...

MUMBAI: Frames, the convention for the business of Indian entertainment organised by Ficci, will take place from 26 – 28 March in Mumbai. Radio and animation...

NEW DELHI: Hailing the country’s telecom sector as “one of the biggest success stories of market oriented reforms”, the Economic Survey of India, tabled in the...

MUMBAI: London-listed Eros International has announced that its film Salaam-E-Ishq, which was released worldwide on 25 January on an impressive 1200 screens, has grossed over Rs...

MUMBAI: Eros International has announced that it has signed a license deal involving minimum guarantee revenues with telecom solutions company Mauj Telecom for distribution of mobile...

MUMBAI: Mobile data services are the next wave of growth for the mobile communications industry amid the increasingly saturated subscriber base. While messaging will continue to...

MUMBAI: Zee Telefilms Ltd. chairman Subhash Chandra is giving his news business a big push. His latest plan of action: to launch a Marathi news channel...

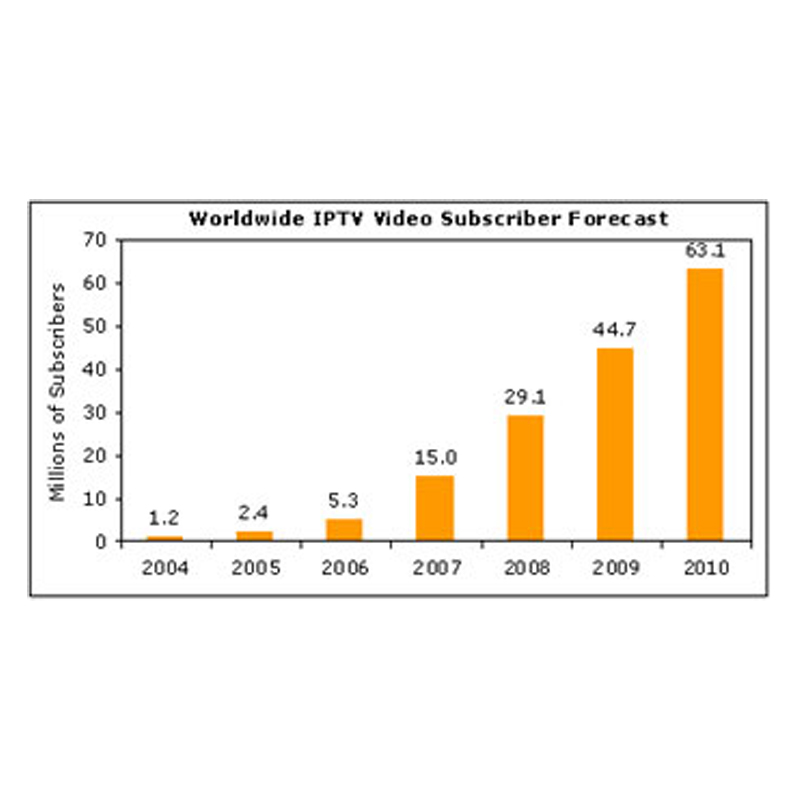

MUMBAI: The worldwide subscriber base for Internet Protocol Television (IPTV) services is expected to expand by a factor of more than 26 from 2005 to 2010,...

DELHI: The Indian entertainment and media (E&M) industry is poised to grow at 19 per cent compound annual growth rate (CAGR) to reach Rs 837.4 billion...

MUMBAI: London based business to business media group Expomedia Group PLC and South Asia’s first specialty media house CyberMedia today announced the signing of a 10-year...

NEW DELHI: Contrary to speculations and expectations – the Telecom Regulatory Authority of India (Trai), it seems is unlikely to make a definitive recommendation on introduction...

William H Roedy’s belief in localisation is complete. When in India, his business cards are printed in Hindi on one side, English the other. The 55-year-old...

NEW DELHI: Current uncertainty over conditional access system notwithstanding, all stakeholders of the game, barring the local cable operators (LCOs), will financially benefit (details later in...

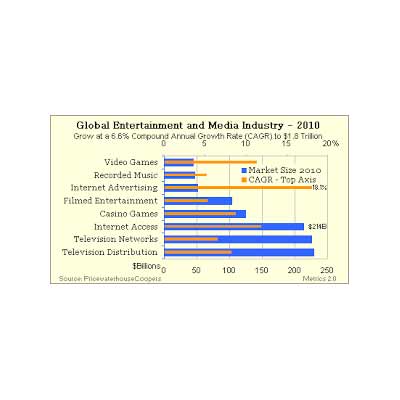

NEW YORK: The global entertainment and media industry spending will surpass $1.1 trillion this year, 3.7 per cent higher than its 2002 level, according to PricewaterhouseCoopers...

MUMBAI: Crisil risk evaluation for the Indian entertainment industry, a pioneering initiative undertaken by CII (Confederation of Indian Industry) would play a catalytic role in channelising...

MUMBAI: A study on wealth creation (1997-2002) by Motilal Oswal Securities’ Inquire Research (MOSt) has placed Zee Telefilms as the sixth fastest growing listed company with...

NEW DELHI: JM Morgan Stanley (JMMS) feels that the valuation of Zee Telefilms, India’s largest vertically integrated media and entertainment company, “looks attractive” in the Indian...

The entertainment and media industry continues to grow and has surpassed US $ 1 trillion in 2001 spending despite the dotcom fallout and a weak global...

Digital distribution of content, aided by rising broadband penetration, will be the greatest driver of new entertainment and media spending in 2005-2006, says the just released...

Ficci convergence committee chairman Amit Khanna believes the Indian entertainment industry is following a healthy growth curve and that piracy in the industry can be countered...