Connect with us

NEW DELHI: India’s digital revolution hit a milestone in November 2025 that would have seemed fanciful a decade ago: one billion broadband subscribers. That is 100...

MUMBAI: Global broadband subscribers surged past 1.52 billion in the first quarter of 2025, marking a 1.21 per cent quarterly rise as South and East Asia...

MUMBAI: GTPL Hathway has unveiled its unaudited financial results for the first quarter ended 30 June 2025, revealing a mixed bag for the entertainment and broadband...

MUMBAI: In a mega-merger straight out of a business blockbuster, Charter Communications and Cox Communications have inked a definitive agreement to combine their businesses, creating an...

MUMBAI: Hathway Cable and Datacom has wrapped FY25 with a cautiously upbeat tune, posting a consolidated profit of Rs 92.5 crore—a modest dip from Rs 99.3...

MUMBAI: Cable TV MSO and broadband major GTPL Hathway Ltd has released its audited financial results for the fourth quarter and the entire financial year, ended...

MUMBAI: To use a cricket analogy, television is going to go even more on the backfoot while online video shall come charging down the pitch to...

MUMBAI: Two companies have tried to deliver TV signals via this mode. One of them- Jain headend in the sky (Hits) was too early – and...

MUMBAI: It has been a challenging year for the cable TV industry, with increasing pressure on their broadband operations from wireless operators like Jio, Airtel, and...

MUMBAI:: It’s a connection that they are hoping will work out for the best. State-owned telecoms provider Bharat Sanchar Nigam Ltd (BSNL) has announced a strategic...

MUMBAI: Bharti Airtel’s Sunil Mittal has planted his company’s flag on the Britain’s biggest broadband and mobile company, the BT group. Earlier this week, Bharti Global,...

Mumbai: OTTplay, an OTT app and AI-based recommendation platform has partnered with Quadrant Televentures (Connect Broadband), a major internet service provider in North India, to enhance...

MUMBAI: The cable TV sector is under pressure in India is known to many and a lot has been written about the rampant cord cutters and...

MUMBAI: Ahmedabad-hqed GTPL Hathway Ltd’s results for Q2 FY 2025 ended on 30 September 2024 are a bit of a mixed bag, according to the company’s...

Mumbai: ACT Fibernet (Atria Convergence Technologies Ltd), a fiber-focused wired broadband internet service provider, has announced its comprehensive suite of enterprise solutions designed to support and...

Mumbai: In a thrilling development for internet enthusiasts in Hyderabad, ACT Fibernet (Atria Convergence Technologies Ltd), a fiber-focused wired broadband internet service provider, has unveiled a...

Mumbai: The Telecom Regulatory Authority of India (Trai) has released the latest edition, for the quarter ending 20 June 2022, of its report “Indian Telecom Services...

Mumbai: Hinduja Group’s NxtDigital has announced the introduction of its flagship integrated solution, OneDigital. This customised customer solution provides a wide range of services, including wi-fi,...

Mumbai: Meta Description: The integrated ecosystem of 5G and IoT (internet of things) has the potential to revolutionise business fortunes if these new technologies are coupled...

MUMBAI: At Bharti Airtel’s fourth quarter 2022 results CEO Gopal Vittal noted that the DTH business continues to see headwinds. During the company’s Q4 FY22 earnings...

Mumbai: OneOTT Intertainment Ltd (OIL), the broadband subsidiary of NxtDigital Ltd (NDL), the media vertical of the Hinduja Group crossed one million wired home broadband subscribers....

MUMBAI: OneOTT Intertainment (OIL), the broadband subsidiary of NXTDigital (NDL), the media vertical of the global conglomerate, Hinduja Group announced that it has crossed one million...

Mumbai: The adoption of streaming in India has happened in stages driven by affordable handsets, cheap data, and most recently the pandemic. While the first two...

Mumbai: Indian digital service provider Jio Platforms Ltd (JPL) and SES, a Luxembourg-headquartered global satellite-based content connectivity solutions provider on Monday announced the formation of a...

Mumbai: Giving a boost to the country’s Digital India ambitions, finance minister Nirmala Sitharaman while announcing the union budget 2022 on 1 February said that 5G...

Mumbai: Telecommunication giant AT&T has rolled out the fastest consumer broadband services at new multi-gig speeds of 2-gig and 5-gig for its fiber customers across parts of...

Mumbai: NxtDigital has upskilled 30-35 per cent of its workforce in digital technology, in addition to making a complete shift to the pre-paid model through enabling...

Mumbai: After the edtech and fintech, it’s time for India to now witness the rise of media-tech, said M&E consultant and industry veteran Anuj Gandhi while...

Mumbai: Indiantelevision.com is back with the 18th edition of the Video & Broadband Summit (VBS). The day-long summit will be held virtually on 19 January 2022,...

Mumbai: Harit Nagpal, the MD and CEO of India’s largest Pay TV distributor – Tata Sky is known to be a vocal man. Time and again,...

New Delhi: Cable TV and broadband service provider GTPL Hathway Limited (GTPL) has clocked a standalone net profit of Rs 30.5 crore for the quarter ended...

New Delhi: The world is moving towards streaming at a pace like never before. And, the media titans are eyeing every opportunity they can get to...

New Delhi: The Society of Cable Telecommunication Engineers (SCTE), India has appointed NXTDIGITAL Limited MD and CEO, Vynsley Fernandes as the honorary chairman, Sandeep Bhargava as...

KOLKATA: GTPL KCBPL has partnered with UKIO to spread smiles during these difficult times and expand their product offering. UKIO is a personalised messaging platform that...

KOLKATA: One of the sectors that received a rapid boost last year amid the work from home scenario was fixed-line broadband. After years of tepid growth,...

KOLKATA: Cable TV services and broadband services were impacted across various places in Maharashtra and Gujarat, as Cyclone Tauktae left a trail of destruction along the...

KOLKATA: NXTDigital has turned its business profitable by raking in Rs 13.66 crore profit after tax (PAT) for the fourth quarter. The company has reported Rs...

KOLKATA: Pan India multi-system operator (MSO) GTPL Hathway is increasing its capex projection for FY22 to Rs 400 crore, compared to Rs 335 crore it invested...

KOLKATA: NXTDigital’s broadband subsidiary OneOTT intertainment Ltd (OIL) has surpassed 100,000 home broadband subscriber additions in the fourth quarter of the financial year 2020-21. According to a press...

KOLKATA: On the back of strong performance in the fourth quarter of FY21, GTPL Hathway has posted Rs 599.1 crore revenue, up 29 per cent year-on-year....

KOLKATA: Multi-system operator (MSO) Siti Networks will pick up 76 per cent stake in Meghbela Infitel Cable & Broadband through its subsidiary Indian Cable Net Company....

New Delhi: Telecom advertising will grow at an average rate of 4.5 per cent a year till 2023, as the sector recovers from an 8.7 per...

KOLKATA: Industry leaders have emphasised over and over again that despite recent developments and change in consumer preferences, pay TV will continue to coexist with over-the-top...

KOLKATA: As the number of internet users in India is reaching new levels gradually, having crossed 700 million in 2020, the home broadband sector also continues...

KOLKATA: Demand for broadband connectivity has existed in India for a while, but recently, calls for better quality of service are growing increasingly strident. While the...

KOLKATA: The Telecom Regulatory Authority of India (TRAI) has extended the deadline for receiving comments on a consultation paper concerning “Roadmap to promote broadband connectivity and...

KOLKATA: Digital is it. Across the country, and age groups, Indians are getting online, and consuming more high speed broadband data than ever before, whether it...

KOLKATA: Meghbela Broadband, one of eastern India’s largest multi system operators (MSOs) and internet service providers (ISPs), has launched Android TV services to its customers through...

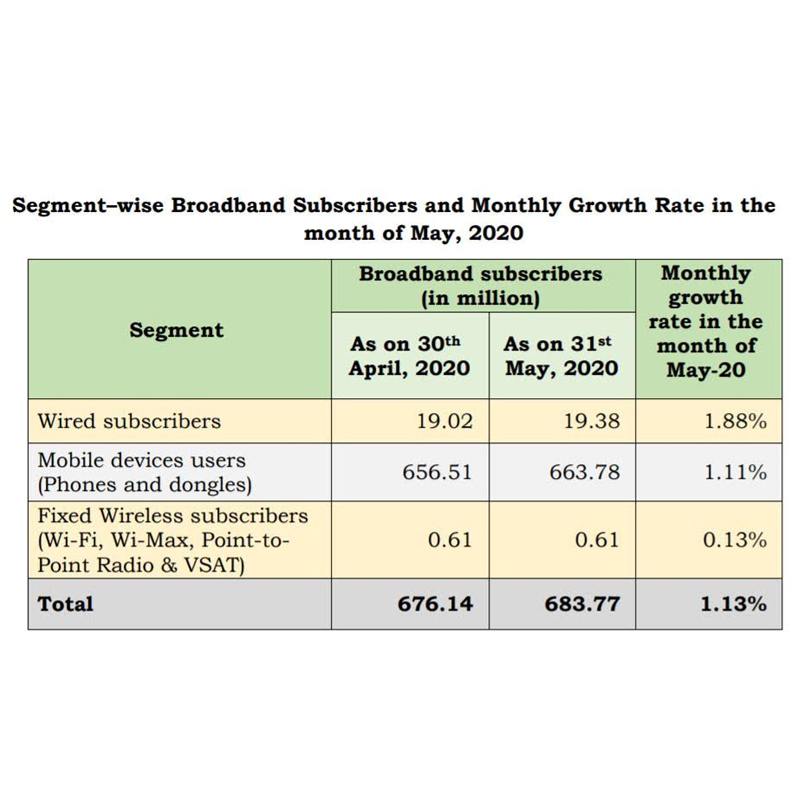

KOLKATA: After seeing a dip in April, the number of broadband subscribers reached 683.77 million at the end of May with an overall growth of 1.13...

KOLKATA: While Mukesh Ambani’s Jio has made quite a buzz for its innovation and acquisitions to expand its Jio Fiber business, Sunil Mittal’s Bharti Airtel is...