Connect with us

MUMBAI: LTIMindtree has brought a seasoned AI strategist into its top leadership, appointing Manoj Kothiyal as chief business officer and global head of AI. The move...

MUMBAI: Sony Pictures Networks India (SPNI) has hired Boston Consulting Group to conduct a comprehensive audit of its operations, according to media reports. The review, ordered...

MUMBAI: Insurance just found its digital double. HDFC Ergo has roped in Consumr.ai, India’s next-gen customer intelligence platform, to pilot a proof-of-concept (POC) that could transform...

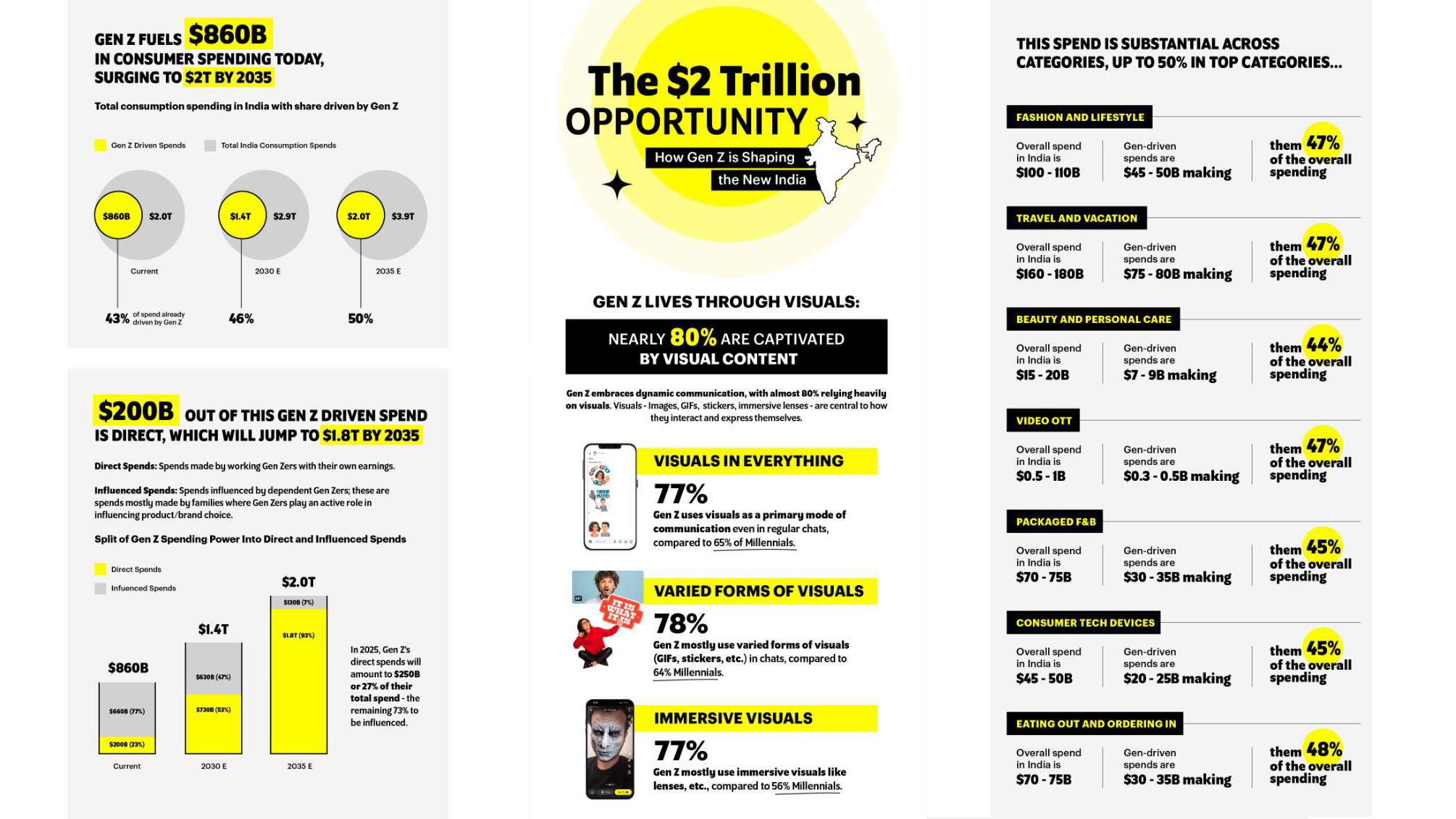

Mumbai: With a population of 377 million, Gen Z is now the largest generation ever to live in India. While they’re often perceived as teenagers, Gen...

Mumbai: The production of local originals in India is heating up and giving a boost to the creative economy. Online video platforms are expected to invest...

Mumbai: Consumer anxiety is at its highest level since the coronavirus outbreak hit India last year, shows the latest round of consumer sentiment survey conducted by...

MUMBAI: The Indian media industry, experiencing disruptions, is witnessing an increase in consumption that has been facilitated by proliferation of broadband too and over the last...

MUMBAI: Content on demand on trains and at stations is a sizeable market, says a report by the Boston Consulting Group (BCG) and, the Indian Railways...

MUMBAI: CASBAA, the Association for digital multichannel TV, content, platforms, advertising and video delivery in Asia, has announced its 4th OTT Summit, Asia’s OTT industry marquee...