Mumbai: In a reflection of the changing media consumption habit and the surge both in digital consumption & advertising, 38 per cent of consumers shared that they have majorly seen ads on digital platforms in the latest Consumer Sentiment Index (CSI) survey by Axis My India. In terms of brand advertisement placements, 44 per cent said they had seen it on television, while only 11 per cent and seven per cent of the audience believe that they have seen ads on print or outdoor respectively. This digital growth is led by the 26-35 age group audience, as per the survey.

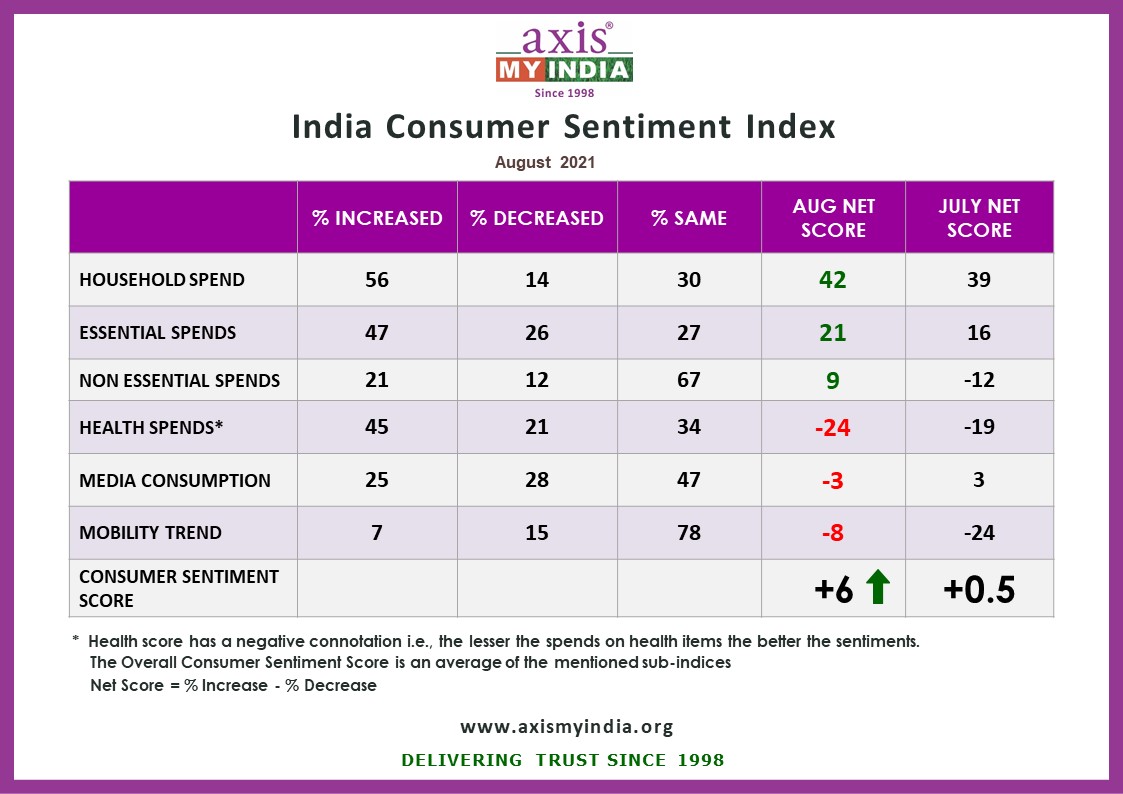

Consumer data intelligence company Axis My India released its latest findings of the India CSI, a monthly analysis of consumer perception on a wide range of issues. The sentiment analysis delves into five relevant sub-indices – overall household spending, spending on essential and non-essential items, spending on healthcare, media consumption habits, and mobility trends. The surveys were carried out via computer-aided telephonic interviews with a sample size of 10430 people. 62 per cent belonged from Rural India while 38 per cent belonged from urban counterparts.

Reflecting the view of the majority, the survey for the month of October reveals that media consumption remains the same for 48 per cent of the families while the same has increased by 25 per cent. In addition, a combined 82 per cent said that they had seen more ads on TV and digital platforms over others.

Overall household spending has increased for 63 per cent of families which reflects a seven per cent increase from the last month. This increase is highest in Northern India.

The increase in spending on essentials like personal care & household items stands at 50 per cent reflecting a surge by five per cent. The net score which was +20 last month has increased to +27 this month. The growth in rural India is slightly higher as compared to urban markets.

Spending on non-essential & discretionary products like AC, car, refrigerator has increased for 18 per cent of families. For 73 per cent spends on non-essential purchases remain the same which reflects an uptick of three per cent from last month. The non-essentials November net score, therefore, lies at +9. The trend on spends on discretionary products reflects a fine balance between caution and indulgence.

With more exposure to outside activities, the importance of health bounced back quickly. Consumption of health-related items increased for 47 per cent of families as compared to 44 per cent last month. The health score which has a negative connotation i.e. the lesser the spends on health items the better the sentiments, has a net score value of -27.

Consumption of media remains the same for a majority of 48 per cent of families and increased for 25 per cent of the family, while mobility net score reflects a constant improvement over the last four months.

88 per cent of families said that they are going out the same or more on getaways/staycations /malls/restaurants, with travel bans being lifted and double vaccination providing easier movement opportunities. The overall mobility score is at -4 which is an improvement over last month which was at -5. This reflects slow but consistent progress in people’s sentiments for engaging in out of home activities

Gauging views around the Diwali festivities, Axis My India, further discovered that 36 per cent of the consumers are planning to go beyond small-ticket purchases this festive season. While 24 per cent are looking to spend on household or personal items like White Goods (AC, TV, Washing Machine, Refrigerator, etc.), furniture, electronics, and jewellery; Nine per cent are looking to buy a four-wheeler or a two-wheeler. Further from a purely sentimental outlook, 59 per cent of the consumers reflect the view of a more hopeful and cheerful Diwali this year!

The November net CSI score, calculated by percentage increase minus percentage decrease in sentiment, was recorded at +9, up from +7 last month and rising at a constant pace over the last three months, indicative of a positive shift in consumer consumption metrics.

“With the festivities at its peak, one can easily witness consumer’s excitement in terms of loosening their purse strings for varied expenses and experiences. While Diwali has triggered spending on products of personal indulgence (like 2-wheeler/4-wheelers or jewellery) and household items, the upcoming festivities and enthusiastic consumer sentiment will further set the momentum for the last half of this year,” said Axis My India CMD Pradeep Gupta, commenting on the October report.

“In addition, one can also witness a transition in terms of preferences amongst consumers’ like opting for EVs or cheering for privatisation of loss-making companies. The growth of digital as a medium of advertising overtaking print & just after TV reflects the change in media consumption habits which was triggered by the pandemic. Lastly, our survey shows that a vast majority of India is still not investing in this age of cryptocurrencies, it would be interesting to see how financial players beyond traditional banks can capture and convert their interests for investments using varied instruments,” he added.

This month, Axis My India’s Sentiment Index also delved deeper to understand consumers’ views on varied issues of national interest. These include privatisation of loss-making public-sector companies like that of Air India, views on economic recovery by 2022, alternatives to rising fuel prices, investment preferences, sentiments around Diwali, and on brand advertisement placements.

While the long-awaited sale of Air India to the Tata group reflected a hopeful future for the airline. Axis My India further gauged consumer’s sentiment on whether or not the government should privatise other loss-making public sector companies. 46 per cent are in agreement with privatisation of such companies while 36 per cent disagreed with this view.

When asked if economy/livelihood and business is expected to bounce back by January 2022, 41 per cent believe that the same is possible and Southern India being more optimistic with 54 per cent agreeing to this. With rising fuel prices being a concern, 48 per cent are optimistic about shifting to electric vehicles wherein 33 per cent and 15 per cent said that they will consider buying a 2-wheeler and 4-wheeler respectively in this segment. The younger age group of 18-35 have a more likelihood, with 53 per cent in agreement to an EV shift.

Sharing their views on financial planning, a majority of 23 per cent still prefers to park their money in savings accounts, while a combined 12 per cent prefers to invest in fixed deposits, shares/stock market, and mutual funds. Gold is still seen as a reliable investment option for four per cent of the consumers. 40 per cent of the audience still don’t invest and interestingly two per cent still save their money in post offices.