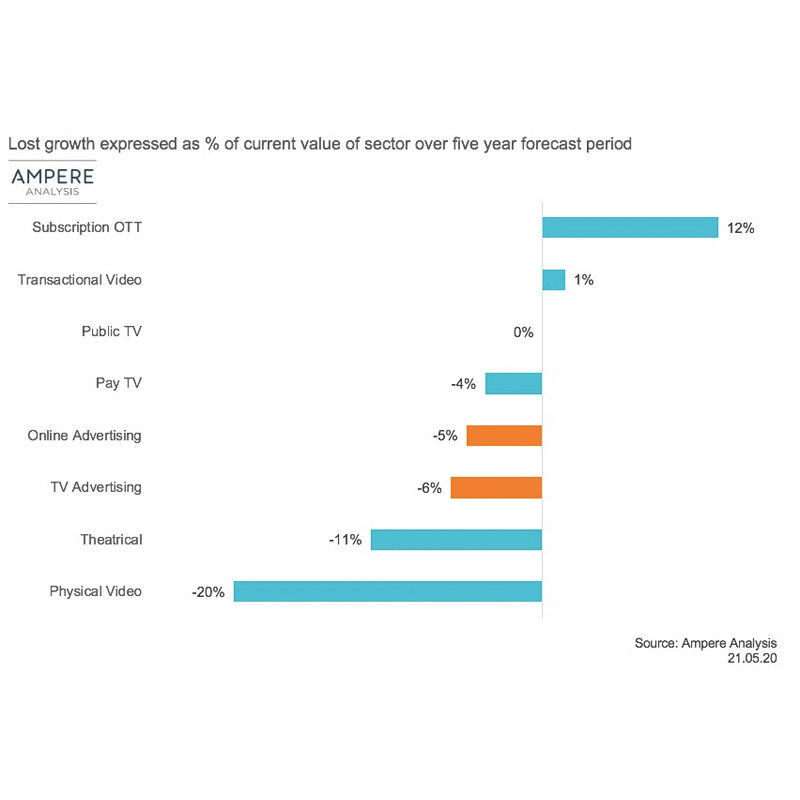

MUMBAI: The global entertainment sector will lose $160 billion of growth due to the Covid2109 pandemic in the coming five years, according to research by Ampere Analysis.

"While the biggest impact will be felt in 2020 and throughout 2021, growth will be reduced each year for the duration of the five-year forecast period. While gross loss (the total amount of lost growth in dollar terms) will be greatest for the advertising sector, it’s also important to look at the relative impact pegged to the size of the sector. On that basis, theatrical will be hardest hit, set to lose $24.4 billion over the next five years, with its revenue growth down more than 11 percent over Ampere’s previous forecasts," says Ampere Analysis.

The TV and online advertising market will lose almost $40 billion of revenue growth and $43 billion next year. Though a recovery can be expected in the year 2022, the figures will not come near the previous forecasts made by Ampere Analysis.

Ampere Analysis research director Guy Bisson said that advertising has been hit the hardest. "The interconnected nature of the entertainment value chain means that will have a number of effects in other areas of the value chain. Some of which will not be fully felt for several years to come," he said.

Shut theatres will have a direct bearing on theatrical revenues. However, the long-term effects “mean a glut of movies vying for release windows next year could ultimately lead to a slowdown in film production that impacts content acquisition and distribution further down the line," said the report.

Streaming winner

Streaming, however, will remain the big winner with viewers relying on such platforms heavily. Streaming will achieve 12 per cent more revenue growth in the next five years, says the research firm. Lockdown across the world have led to an exponential increase in “streaming consumption and new subscriptions, benefiting subscription video-on-demand, broadcaster video-on-demand and other catch-up services."

Pay TV, which has already gone through huge losses due to the lack of live sports, will be losing “significant value in what was already a challenging market structurally, representing around four per cent of its previously forecast value," says the research firm.

Scripted TV to suffer

The firm predicts disruption in the supply and release of new content for a year due to delays in production caused by Covid2019.

While the unscripted market will likely to easily withstand the pandemic, the scripted TV sector will be affected, and its effects remaining so for the rest of the year and even into 2021. This will remain so even if production resumes by June.

“There is one certainty among the current uncertainty – that the Covid2019 pandemic will change the TV production industry far beyond the end of the lockdown. Initially, we expect delays to cause gaps in scripted TV release schedules, which broadcasters and streaming players will have to fill with other content. However, as delayed productions begin to fill out content gaps in later months, these gaps will begin to close. But this has further ramifications. The knock-on effect of delayed releases is a likely depression of the number of new commissions for some time after the shutdown ends, as commissioners look to fill schedules with delayed projects they have already invested in before signing off new ones,” says Ampere Analysis senior analyst Fred Black.

Follow Tellychakkar for the consumer facing news & entertainment