Connect with us

MUMBAI: The attention span may be shrinking, but the audience for micro-drama is exploding. More than one in ten internet users worldwide now regularly watch drama...

MUMBAI: Audiences worldwide are consuming more South Korean content than ever, but the number of new TV commissions is shrinking, according to research from Ampere Analysis....

MUMBAI: YouTube’s not just for prank videos and pet fails anymore. That was a point made by YouTube global head Neale Mohan earlier this year when...

MUMBAI: South Korean content is delivering knockout streaming figures for Netflix, now accounting for a whopping 17 per cent of the platform’s top 500 non-US shows...

MUMBAI: The big media and entertainment boys are at it, despite all round murmurings that the content production business is seeing a massive slowdown. At least,...

Mumbai: A combined offering of Disney+ and Hulu would account for the largest share of the 100 most popular titles of any US subscription video on...

Mumbai: Western Europe will generate annual revenues of $1.9 billion for Netflix from advertising by 2027, more than the US and almost as much as North...

Mumbai: According to a new report by Ampere Analysis, the Asia-Pacific will be the strongest growth region for Netflix’s ad tier, with one of the largest...

Mumbai: Ampere Analysis Q1 2022 reported rising demand for renewed seasons on Video-on-Demand (VoD) platform giving impressive numbers altogether. The increase in the volume of streaming...

Mumbai: Streaming giant Netflix is slated to release 398 shows in 2022 which is with more original TV content expected to air on the platform, according...

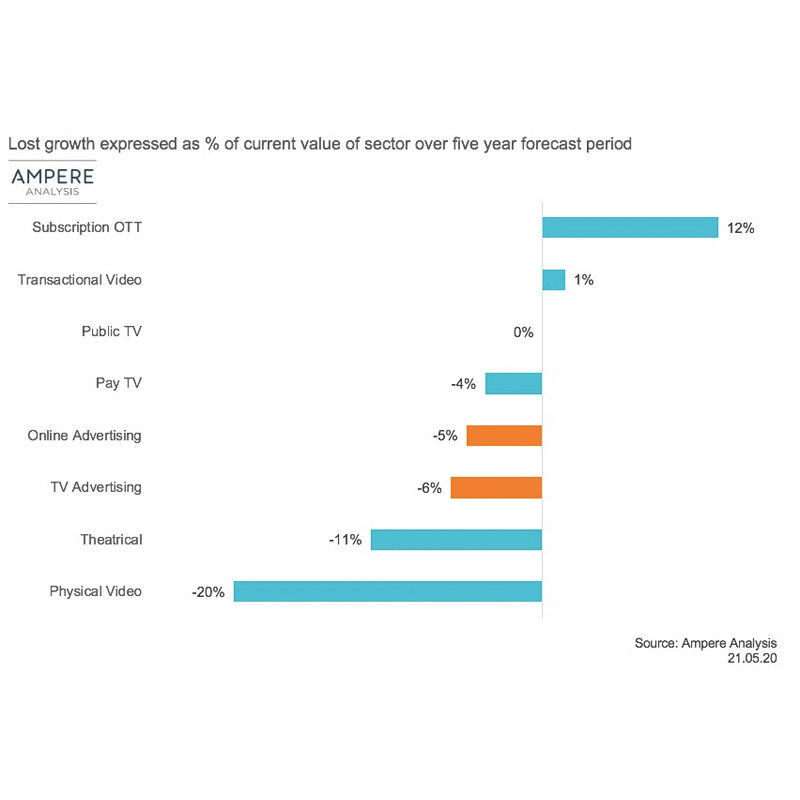

MUMBAI: The global entertainment sector will lose $160 billion of growth due to the Covid2109 pandemic in the coming five years, according to research by Ampere...

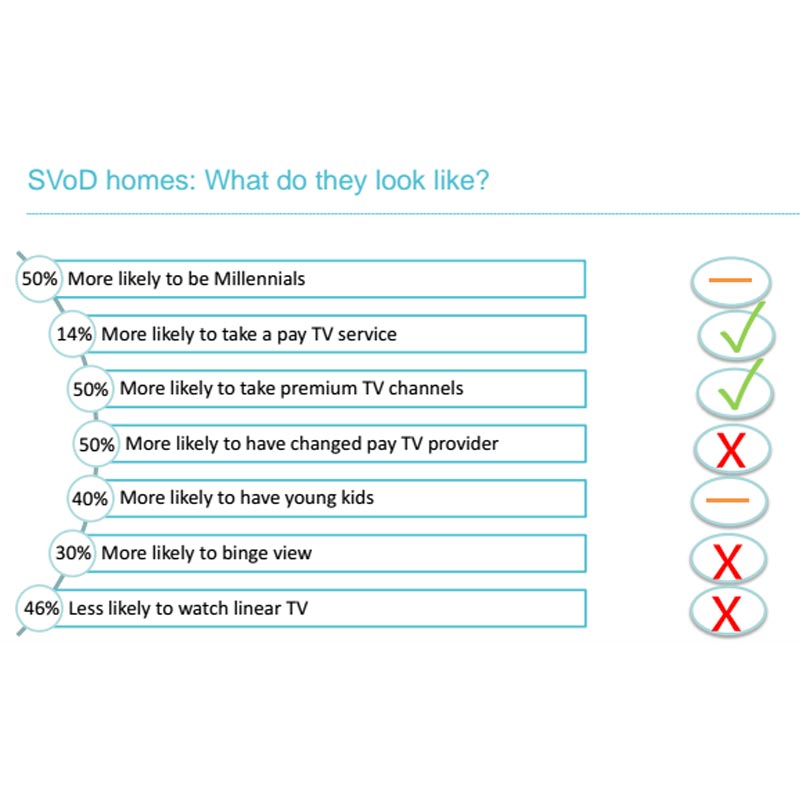

MUMBAI: Subscription video on-demand (SVoD) content is increasing more and more as compared to Pay TV. Several discussions have taken place in India with the growing...

MUMBAI: Subscription video on-demand (SVoD) content is increasing more and more as compared to Pay TV. Several discussions have taken place in India with the growing...