Connect with us

Mumbai: The advertising industry is gaining momentum after COVID-19 due to large exposure to digital platforms. Large conglomerates are spending heavily on advertising consumers and also...

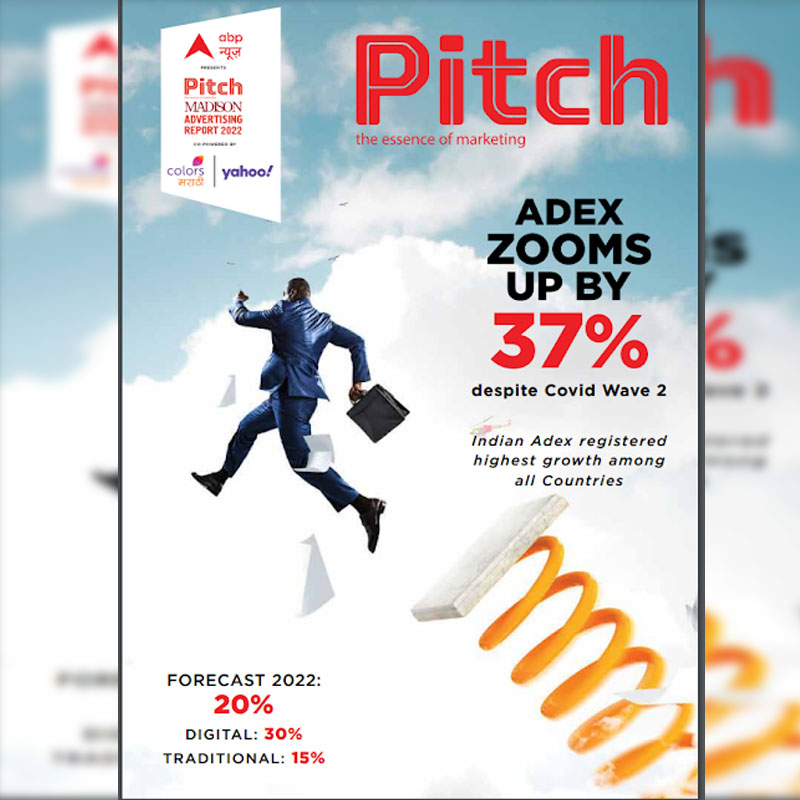

Mumbai: Despite the lingering impacts of the pandemic, advertising expenditure is set to surge by 20 per cent to reach nearly Rs. 90,000 crore, according to...

MUMBAI: Global media network Carat’s first forecast for worldwide advertising expenditure in 2016 shows that Indian advertising spend is poised to grow by 11.3 per cent...

MUMBAI: Global online advertising revenues will reach $143 billion in 2017, double the $66 billion recorded in 2010 and considerably up from the $92 billion predicted...