MUMBAI: Global advertising expenditure is expected to grow by 5.3 per cent to $ 532bn, according to a report from media agency ZenithOptimedia.

The agency has increased its forecast for 2014 by 0.2 percentage points since September, after recent signs of stronger growth from markets like the US, the UK, Germany, Hungary, Poland, Australia and Mexico, together with evidence that Spain’s steep downturn is finally bottoming out.

Interestingly, this is the second time that the agency upgraded its expectations for 2014 this year, the first was in June (from 5.0 per cent to 5.1 per cent). In fact, for the year 2015, it expects the global ad market to accelerate to 5.8 per cent, followed by another year of 5.8 per cent growth in 2016.

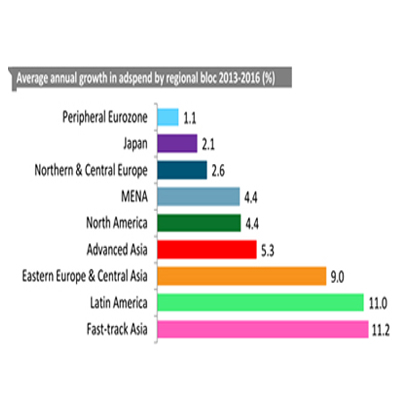

As part of its global analysis, the agency has also included Ireland in the so-called Peripheral Eurozone category. It assumes that the growth for these countries will be somewhat more muted.

The agency says that in Europe, it has separated the ‘PIIGS’ markets (Portugal, Ireland, Italy, Greece and Spain), which have faced the full brunt of the Eurozone crisis, into the Peripheral Eurozone. “Their ad markets have fallen even more sharply than their economies, as local advertisers cut back to reduce losses and preserve cash, and multinationals withdraw budgets to redeploy in more economically healthy regions. We estimate that ad expenditure in Peripheral Eurozone fell by 11.1% in 2013. 2014 looks a lot better, with ad expenditure forecast to shrink by just 0.9%, followed by a slow recovery of 1.8% growth in 2015 and 2.5% growth in 2016. This assumes that the Eurozone avoids disaster over our forecast period, and in particular assumes that no country crashes out of the euro, or falls into disorderly default on its debts,” says the report.

The report also reveals that the rest of Western Europe, as well as Central European countries like the Czech Republic, Hungary and Poland, which are currently performing more like countries such as France, Germany or the UK than the much-faster growing markets of Eastern Europe, such as Russia and Ukraine. “This is partly because many of these Central European markets are in the Eurozone, and because they have strong trading links with Zenith Optimedia Group Limited,” it says.

As far as the Asian market is concerned, the agency has divided it in to four parts – Japan, Eastern Europe and Central Asia, Advanced Asia and Fast-track Asia.

The report says that the Eastern European advertising markets, such as Russia and Ukraine, recovered quickly after the 2009 downturn and have since continued their healthy pace of growth, largely (though not entirely) unaffected by the problems in the Eurozone. “Their near neighbours in Central Asia, such as Azerbaijan and Kazakhstan, have behaved very similarly, so we have gathered them together under the Eastern Europe & Central Asia bloc. We expect this bloc to have grown 11.7% by the end of 2013, followed by 8%-10% growth for the rest of our forecast period,” it says.

The agency has kept Japan separate as the market behaves differently from the other markets in Asia. Even after the recent economic stimulus, Japan remains stuck in its rut of persistent low growth and grew 2.1 per cent in 2013. The agency estimates the growth rate of the country to remain at 2 per cent per year through to 2016.

Apart from Japan, there are five countries in Asia with developed economies and advanced ad markets and thus they are categorised as “Advanced Asia”. It includes Australia, New Zealand, Hong Kong, Singapore and South Korea. The report reveals that growth here has been a disappointing 1.3 per cent in 2013, after a period of heightened tension between North Korea and its neighbours caused advertisers in South Korea to cancel or postpone several campaigns. “We forecast a much healthier 4.5 per cent growth in 2014, followed by 6.6 per cent growth in 2015 and 4.8 per cent growth in 2016,” says the agency in the report.

Fast-track Asia includes countries like China, India, Indonesia, Malaysia, Pakistan, Philippines, Taiwan, Thailand and Vietnam as these economies are growing extremely rapidly as they adopt Western technology and practices. This group barely noticed the 2009 downturn (ad expenditure grew by 7.2 per cent that year) and since then has grown comfortably at double-digit rates. We estimate that ad expenditure in Fast-track Asia has grown 10.7 per cent in 2013, followed by 10 per cent to 12 per cent annual growth in 2014 to 2016.