Connect with us

MUMBAI: Advertisers, marketers and media establishments around the globe can bring out the bubbly. dentsu’s latest Global Ad Spend Forecasts has revealed a projected buoyant 6.8...

MUMBAI: Bullish is the mood at marketing effectiveness specialist Warc. The firm had forecast in August 2024 that global advertising spend is on course to grow...

Mumbai: After two Covid-impacted years, the mood among consumers and advertisers for the festive season is a lot better. Media agencies expect a decent uptick in...

Mumbai: CTV/OTT viewership has exploded in India since the start of the pandemic, opening a new market of opportunities for advertisers. Combining the best of digital...

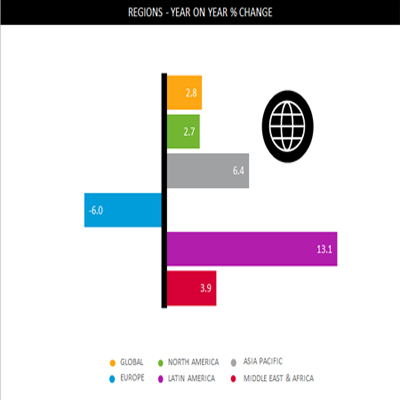

Mumbai: Global advertising expenditure is expected to grow 8 per cent in 2022, according to Zenith’s latest Advertising Expenditure Forecasts report, which was released on Wednesday....

Mumbai: Advertising expenditure in the Asia Pacific is expected to grow by 5.9 per cent, with India being the fastest-growing market globally at 14.6 per cent,...

Mumbai: The television ad volume recorded significant growth in 2021, beating the previous year’s performance, according to the latest data released by the Broadcast Audience Research...

MUMBAI: Management guru Peter Drucker once said, “Because its purpose is to create a customer, the business enterprise has two — and only these two –...

Mumbai: The media industry and the economy saw an unprecedented level of disruption post-lockdown phase. As marketers went back to the drawing board to scrutinise their...

MUMBAI: As the world adapts to the post-pandemic world, there’s been a significant shift in the way people shop, eat and look for entertainment among other...

Mumbai: TV advertising continues to remain resilient, despite the onslaught of the second wave of the pandemic. According to Broadcast Audience Research Council (BARC) India’s latest THINK...

New Delhi: Global advertising spend is expected to rise 12.6 per cent during 2021 as a whole to reach $665bn, according to WARC Data’s report tracking...

New Delhi: After a 27 per cent plunge in 2020, ad revenue in India is forecast to rebound strongly over 2020-25 with a CAGR of 13...

MUMBAI: Alcohol ad spend in 12 key markets, including India will grow by 5.3 per cent in 2021, ahead of the 4.9per cent growth of the...

MUMBAI: GroupM, the media investment group of WPP, today announced their advertising expenditure (adex) forecasts for 2020. As per the GroupM futures report ‘This Year, Next...

MUMBAI: Consumers across the globe are becoming increasingly engaged with online videos. Zenith’s Online Video Forecasts 2018 reveals global consumers will spend watching online videos more...

MUMBAI: Ad growth in India–a contender for Asia’s most dynamic market–was weighed down in 2017 by the lingering effects of demonetisation as well as a new...

MUMBAI: The price of Colgate-Palmolive Co’s shares plummeted on Friday after the company reported lower-than-expected quarterly sales despite spending more on advertising and cutting prices. The...

BENGALURU: Shemaroo Entertainment has its maiden annual numbersafter listing in September 2014. The company has reported 50.7 per cent growth in profit after tax (PAT) at...

BENGALURU: Hawkins Cookers Limited (Hawkins) reported a 10.3 per cent quarter on quarter (q-o-q) increase in advertisement (ad) spends in Q2-2015 at Rs 3.72 crore (2.5...

MUMBAI: In its latest study of global media owner advertising revenues, covering 73 countries, Magna Global estimates that ad revenues grew by more than 5.5 per...

BENGALURU: Consumer products major and one of the largest advertisers in its segment in the country, Colgate-Palmolive (India) spent 21.64 per cent more towards advertising expense...

NEW DELHI: Ad spends grew by a substantial 6.4 per cent in the first half of 2013, making it the largest growth among different regions of...

MUMBAI: Due to the continuing sluggishness in the US and European economies, the global ad spend in 2013 will grow by 4.5 per cent, as per...

MUMBAI: Advertising spend in China rose 20 per cent in the first half of the year to $17.7 billion. Companies like Procter & Gamble Co were...

MUMBAI: Television advertising in India is expected to grow by 14 per cent by 2007, while over the next one year the increase is likely to...

MUMBAI: Advertising spending for 2004 in the US rose by 6.3 per cent over the same period last year. This has been attributed to gains across...

NEW YORK: A study by BIGresearch and the US based Centre for Media Research concludes that the growth of simultaneous media usage should have direct impact...