News Broadcasting

CNBC’s post budget show captures industry sentiments

MUMBAI: CNBC, the business and financial channel has lined up a series of pre and post budget specials. CNBC also held a post budget round table in Mumbai where leaders and experts spoke on the budgets pros and cons.

The six-part post budget show, Budget-The Reality show will have comprehensive reports and analysed the implications of the budget. The show will combine in-studio debates and comments from experts from all over the country. It will air from 3-10 March.

The following are some reactions from captains of the industry who participated in the discussions.

Bajaj Auto chairman Rahul Bajaj:

“Without substantially increasing the fiscal deficit he (finance minister) has taken care of the democratic aspirations of the people, the fact that elections are coming later this year and next year. Some people think that’s a very negative thing to do. But here, I think, he has said that we are moving away from this exemption economy, maybe it will take two-three years or maybe this was the wrong year for that. But he has not changed the basic tax rates except for individuals and corporates.’ Overall, it is a good budget.”

Bharti Enterprises CMD Sunil Mittal:

“There is a big jump in service tax from 5 per cent to 8 per cent. The telecom industry actually caters to a large part of service tax collections by the government. We hope this will allow them to reduce the licence fee that they charge from the telecom industry because 8 per cent service tax and nearly 16% of the revenue share, which goes as licence fee, is too much for the industry to bear.”

Ashish Guha of Lazard India

“The finance minister has not touched upon agriculture infrastructure. That is a miss. He has done a lot for the capital markets. On interest rate, for the industry, 1 per cent gone on mall savings rate. Despite being an election year, he touched upon fertiliser pricing”.

TISCO MD B Muthuraman

“On infrastructure, the budget has been very good, which is going to be good for steel, cement. The finance minister made a small announcement that 25 per cent of the roads be made of concrete. Excise duty on cars, ACs are rationalised. This being an election year, I was not expecting a budget like this.”

Enam Financial Consultants director Vallabh Bhansali

“The finance minister has put a lot more money in the hands of consumers and investors. He has done something on state finances, which are in a disarray. I’m pleased about that. In terms of misses, I wish he had done something on power reforms because half the state deficit is on account of power. Another miss which market men rue very much is the SBI FII limit.”

“Health coverage announced for poor people is a good thing and if it can become a basis for social security, a lot of opposition to liberalisation can go down. The market was technically overbought. It has not understood the implication of the capital gains tax move. Maybe, the market did not want the dividend distribution tax.”

Alliance Capital Management CEO Nikhil Johri

“The impact of budgetary announcements on the mutual fund industry will be quite positive. Dividends received in the hands of investors will now be tax-free and at the mutual fund level, there will be no dividend distribution tax for equity and equity-oriented schemes, and a 12.5 per cent distribution tax for debt schemes.”

“This policy will henceforth make investments in mutual funds much more attractive for both retail and institutional investors. The relative advantages of mutual funds over other savings instruments such as bank deposits, etc, will focus significant attention on mutual funds, particularly when the interest rates on administered small savings schemes have been brought down.” he added.

“The substitution of TDS provision by dividend distribution tax is also going to be operationally more convenient for industry. The removal of surcharge on personal income tax will increase the investible surpluses of individual investors, thereby increasing his allocation to mutual funds. The decision to set up a separate pension regulatory authority and to allow a defined contribution based pension system, is a very welcome step. Overall, the Budget is as positive as it could be for the Indian mutual fund industry.” he added.

Godrej Consumer Products ED Hoshedar K Press

“‘The budget has only partially met the expectations of our industry. The main positive is the reduction of the maximum rate of import duty from 30 per cent to 25 per cent. The reduction of IT surcharge may not help to stimulate demand for our flagging categories. The much needed reduction in excise duty did not come through except for rationalisation of alcohol-based toiletries. Thus, the budget has not taken the opportunity to take the business to a higher plane.”

Zensar Technologies MD Ganesh Natarajan

” The big hits (of the budget) are Sections 10A/10B and infrastructure improvement because, today, the industry is attracting a number of people to come back from Europe and US. And, for them, good infrastructure in the country will be important. The small miss is the domestic sector because the government had announced last year that three per cent of spending would be on IT. We hope that a lot more will be done to make sure that spending happens, which would improve the state of Indian industry and the economy.

Vikram S Mehta of Shell Group

“There are two important developments. One, for the first time in several years the finance minister has focused on renewable energy. He has specifically mentioned a fund for research for solar energy and wind power. Second, he has reduced the customs duty on regassified natural gas from 25 per centto 5 per cent. This will be an impetus to the power sector. Also, it is a very realistic budget. He hasn’t put out a number on disinvestment, which is very good because they haven’t been able to fulfill that number. But, he has made his commitment known to is investment.”

KERALA: A forensic audit commissioned by the Broadcast Audience Research Council (BARC) India has emerged as the centrepiece of the government’s response to fresh allegations of television rating point manipulation involving a regional news channel in Kerala, with both the audit findings and a parallel police investigation still awaited.

Replying to a query in the Lok Sabha, minister of state for information and broadcasting L Murugan, said Barc had appointed an independent agency to conduct a forensic probe into the conduct of senior personnel allegedly linked to the case.

The move followed media reports claiming that a Barc employee had accepted bribes to manipulate viewership data in favour of a regional television news channel.

“The report from BARC is still awaited,” Murugan told Parliament, signalling that the forensic exercise remains ongoing.

Industry specialists say forensic audits are crucial in alleged TRP fraud cases, as they examine internal controls, data access trails, panel household integrity, staff communications and financial transactions. The outcome could determine whether the alleged manipulation was an isolated breach or a deeper systemic weakness in India’s television measurement framework.

Running alongside the audit, the Kerala Police has formed a special investigation team to probe the allegations. The ministry has sought a preliminary report from the state’s director general of police, including details of action taken on the first information report. That report, too, is yet to be submitted.

The episode has revived long-standing concerns over the vulnerability of India’s TRP system, particularly in regional news markets where competition for ratings is fierce and advertising revenues hinge on weekly viewership rankings.

India’s sole television audience measurement body Barc, has faced scrutiny before, most notably during the nationwide TRP controversy involving news channels in 2020. While tighter compliance norms were introduced in the aftermath, the latest allegations suggest enforcement challenges may persist.

On regulatory consequences, the government said any punitive action against television channels, including suspension or cancellation of uplinking and downlinking permissions, would be governed by the Policy Guidelines for Uplinking and Downlinking of Television Channels issued in November 2022, and would depend on investigation outcomes and due process.

The ministry also pointed to ongoing efforts to overhaul the ratings ecosystem. Television measurement continues to be regulated under the Policy Guidelines for Television Rating Agencies, 2014. Draft amendments were released for public consultation in July 2025, followed by a revised version in November 2025, aimed at tightening audit mechanisms and improving transparency and representativeness.

In November 2025, Barc said it had taken note of allegations aired by Malayalam news channel Twenty-Four, which linked an internal employee to irregularities in audience measurement. The council said it had engaged a “reputed independent agency” to conduct a comprehensive forensic audit, underscoring the seriousness of the claims.

The ratings system sits at the heart of India’s broadcast advertising economy, shaping billions of rupees in annual ad spends. With trust in audience data once again under strain, advertisers, broadcasters and regulators are closely watching the outcome of the investigations.

Barc has urged industry stakeholders and media organisations to exercise restraint while the probe is underway, calling for an end to “unverified or speculatory claims” and reiterating its commitment to integrity and accountability.

Until the forensic audit and police findings are submitted and reviewed, the government said it would refrain from drawing conclusions.

News Broadcasting

Rajat Sharma defamation row: Delhi court summons Congress leaders Ragini Nayak, Pawan Khera and Jairam Ramesh

NEW DELHI: A Delhi court has ordered the summoning of senior Congress leaders Ragini Nayak, Pawan Khera and Jairam Ramesh in a criminal case filed by veteran journalist Rajat Sharma, sharpening a legal battle over alleged defamation and doctored digital content.

The order was passed on Monday by Devanshi Janmeja, judicial magistrate first class at Saket Courts, after the court found prima facie grounds to proceed under multiple sections of the Indian Penal Code, including forgery, creation of false electronic records and defamation.

Sharma, chairman and editor-in-chief of India TV, had approached the court over allegations made in June 2024 that he had used derogatory language against Congress spokesperson Ragini Nayak during a live television debate. He denied the charge, claiming it was fuelled by a manipulated video circulated online.

According to the complaint, a clipped version of the broadcast carrying superimposed captions, which were not part of the original programme, was first shared on social media platform X by Nayak and later amplified through retweets and public statements by Khera and Ramesh. Sharma said the viral spread caused serious reputational harm and personal distress.

The court took note of forensic science laboratory findings that pointed to visible post-production alterations in the video, including added titles and captions. It also cited witness testimonies from those present during the live broadcast, who stated that no abusive or objectionable language had been used.

In a related civil matter, the Delhi High Court had earlier observed a prima facie absence of abusive remarks and directed the removal of the disputed social media posts.

With criminal proceedings now set in motion, the case adds to mounting scrutiny around political messaging, digital manipulation and accountability on social media platforms.

News Broadcasting

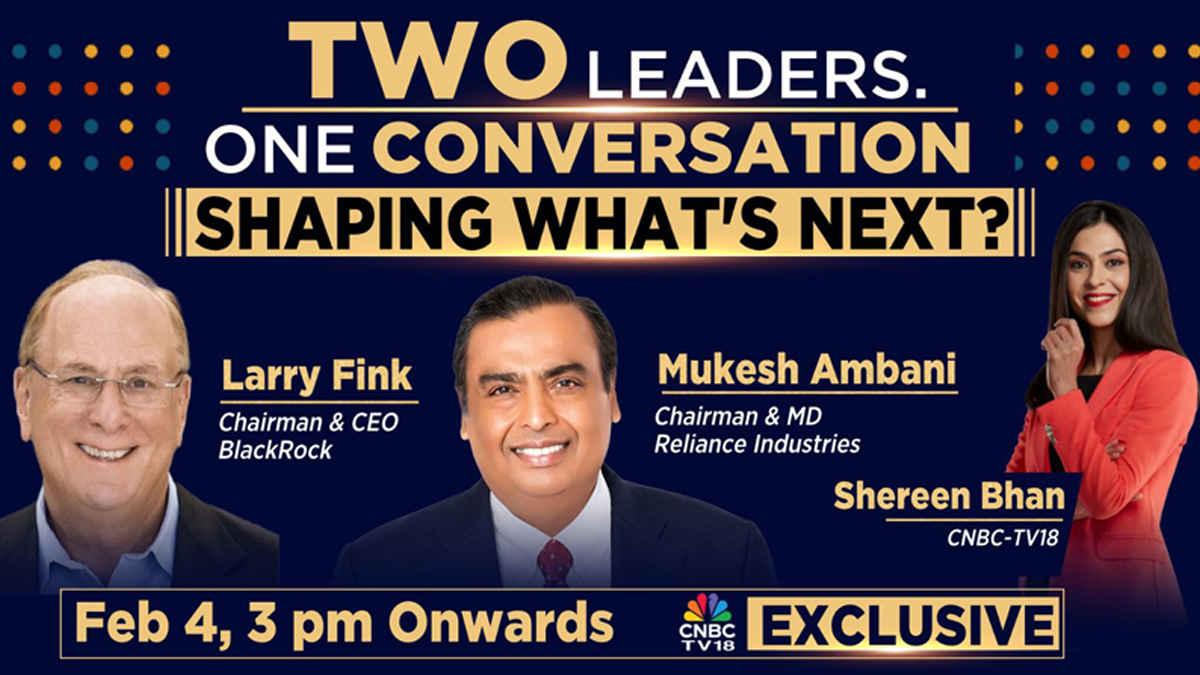

Mukesh Ambani, Larry Fink come together for CNBC-TV18 exclusive

Reliance and BlackRock chiefs map the future of investing as global capital eyes India

MUMBAI: India’s capital story takes centre stage today as Mukesh Ambani and Larry Fink sit down for a rare joint television conversation, bringing together two of the most powerful voices in global business at a moment of economic churn and opportunity.

The Reliance Industries chief and the BlackRock boss will speak with Shereen Bhan, managing editor of CNBC-TV18, in an exclusive interaction airing from 3:00 pm on February 4. The timing is deliberate. Geopolitics are tense, technology is disruptive and capital is choosier. India, meanwhile, is pitching itself as a long-term bet.

The pairing is symbolic. Reliance straddles energy transition, digital infrastructure and consumer growth in the world’s fastest-expanding major economy. BlackRock, the world’s largest asset manager, oversees more than $14 tn in assets and sits at the nerve centre of global capital flows. When the two talk, markets tend to listen.

Fink’s appearance marks his third India visit, a signal of the country’s rising strategic weight for the Wall Street-listed firm, which carries a market value above $177 bn. His earlier 2023 trips included an October stop in New Delhi, where he met both Ambani and Narendra Modi.

India is now central to BlackRock’s expansion plans, notably through its joint venture with Jio Financial Services. Announced in July 2023, the 50:50 venture, JioBlackRock, commits up to $150 mn each from the partners to build a digital-first asset-management platform aimed at India’s swelling investor class.

The backdrop is robust. BlackRock ended 2025 with record assets under management of $14.04 tn, helped by $698 bn in net inflows, including $342 bn in the fourth quarter alone. Scale gives Fink both heft and a long lens on where money is moving.

He has been openly bullish on India. At the Saudi-US Investment Summit in Riyadh last year, Fink argued that the “fog of global uncertainty is lifting”, with capital returning to dynamic markets such as India, drawn by reforms, demographics and durable return potential.

Expect the conversation to range beyond balance sheets, into technology’s role in finance, access to capital and the mechanics of sustainable growth in a fracturing world order. For investors and policymakers alike, it is a snapshot of how big money is thinking about India.

At a time when capital is cautious and growth is contested, India wants to be the exception. When Ambani and Fink share a stage, it is less a chat and more a signal. The world’s money is still looking for its next big story, and India intends to be it.

MIB sets OTT accessibility rules, mandates captions and audio description

Boney Kapoor acquires remake rights of Tamil political satire Thalaivar Thambi Thalaimaiyil

Netflix India names Rekha Rane director of films and series marketing

Zabeen signs off from TV9 after shaping the network’s public voice

Dhawan steps up to bat for Delhi’s grassroots sports push

Orient Beverages pops the fizz with steady Q3 gains and rising profits

Cheekatilo shines in the dark with record debut on Prime Video

Swiggy Instamart’s GOV surges 103 per cent year on year to Rs 7,938 crore

These ’90s fashion trends are making a comeback in 2017

The final 6 ‘Game of Thrones’ episodes might feel like a full season

According to Dior Couture, this taboo fashion accessory is back

ATN International brings ATN Bangla to Canada

The old and New Edition cast comes together to perform

Phillies’ Aaron Altherr makes mind-boggling barehanded play

MIB sets OTT accessibility rules, mandates captions and audio description

Boney Kapoor acquires remake rights of Tamil political satire Thalaivar Thambi Thalaimaiyil

Netflix India names Rekha Rane director of films and series marketing

Zabeen signs off from TV9 after shaping the network’s public voice

Dhawan steps up to bat for Delhi’s grassroots sports push

Orient Beverages pops the fizz with steady Q3 gains and rising profits

Cheekatilo shines in the dark with record debut on Prime Video

-

e-commerce1 month ago

e-commerce1 month agoSwiggy Instamart’s GOV surges 103 per cent year on year to Rs 7,938 crore

-

iWorld1 year ago

iWorld1 year agoKuku TV transforms India’s OTT space with vertical microdrama boom

-

News Headline1 year ago

News Headline1 year agoTRAI puts a ‘stop’ to unsolicited calls and messages

-

News Headline2 months ago

News Headline2 months agoFrom selfies to big bucks, India’s influencer economy explodes in 2025

-

Comedy2 years ago

Comedy2 years agoTaarak Mehta Ka Ooltah Chashmah celebrates 4,000 episodes

-

MAM2 years ago

MAM2 years agoOpenAI joins C2PA steering committee

-

News Headline2 years ago

News Headline2 years agoOdisha to host Ultimate Kho Kho Season 2 from December 24

-

News Headline1 year ago

News Headline1 year agoAbhishek Bachchan joins as co-owner of European T20 Premier League