Brands

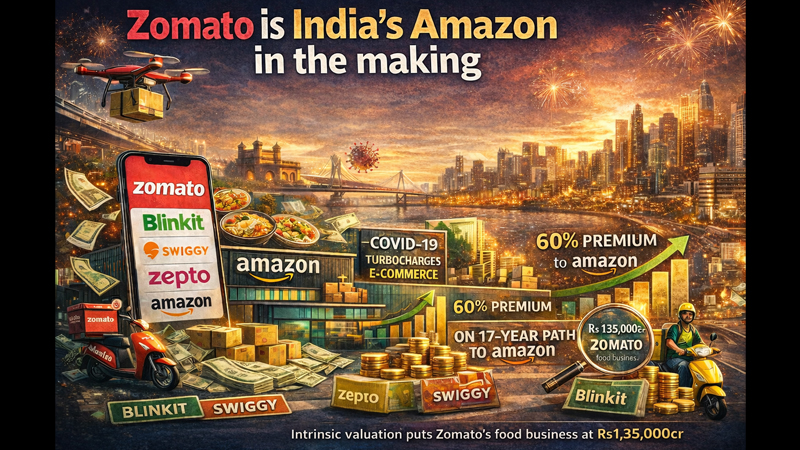

Eternal Limited is India’s Amazon in the making

MUMBAI: Zomato, India’s dual-headed monster of food delivery and quick commerce, is marching towards profitability at a clip that puts its global peers to shame. The company, which operates the Blinkit quick commerce platform alongside its core food business, is outpacing Amazon’s historical growth trajectory and deserves the hefty valuation premium it commands, said Karan Taurani at Elara Securities’ signature theme series webinar on Friday.

Taurani’s “Internet on Eternal” playbook:a deep dive into platform valuation methodology:compares Zomato to Amazon on a 30-year lifecycle basis. The verdict: Zomato is roughly in its 17th year of operation, precisely where Amazon sat when it finally hit breakeven profitability. But unlike Amazon in 2005, Zomato is growing revenue at 46 per cent compound annual growth versus Amazon’s 22 per cent at the same stage. That speed differential justifies Zomato trading at 4.9 times forward enterprise value-to-sales, compared with Amazon’s 2.3 times back then:a 60-70 per cent premium that investors have been questioning.

India’s e-commerce landscape is in the throes of a violent disruption, and Zomato sits at the epicentre. Quick commerce:delivering groceries, gadgets and guacamole in under 10 minutes:is cannibalising traditional online retail and forcing behemoths like Amazon and Flipkart to scramble. What COVID-19 sparked, quick commerce is turbocharging: online retail penetration has doubled from 3.5 per cent to seven per cent of total retail in just five years. Analysts reckon it could hit 13-14 per cent within the decade, with quick commerce the battering ram smashing through the doors.

Zomato’s food delivery arm has already reached steady-state profitability of four to 4.5 per cent EBITDA as a percentage of gross order value, and five per cent-plus as a percentage of net order value. The worst, Taurani insists, is behind the company. Blinkit, still bleeding cash, will follow suit:and faster than legacy e-commerce players managed. Flipkart, operating in India for 10-12 years, still posts EBITDA losses of over Rs1,000cr annually. Myntra only broke even last year. Quick commerce will crack profitability quicker, Taurani argues, because the customer habit of ordering online already exists, and advertising revenue:a “big lever”:offers margin upside that pure e-commerce lacked.

The growth rates tell the story. India’s overall e-commerce market has slowed from a galloping 25-30 per cent annually to a more pedestrian 15-18 per cent. But quick commerce platforms are tearing along at 50-60 per cent compound annual growth rates, grabbing market share with startling speed. They account for just seven to eight per cent of India’s e-commerce pie today. That is about to change, and fast.

Behind the growth lies a simple insight: Indians will pay for speed. Amazon Fresh, launched half a decade ago to crack India’s grocery market, flopped spectacularly because consumers would not wait for slotted delivery. Quick commerce changed the equation overnight. Categories like groceries:stuck at a miserable two per cent online penetration compared with 10-15 per cent globally:are suddenly ripe for plunder. So are general merchandise, stationery, beauty products and mobile accessories: precisely the sort of items people used to nip to the corner shop for.

Zomato’s dual platform gives it unmatched reach. Food delivery appeals to a narrower use case; Blinkit can hawk small appliances, apparel, accessories and everything in between. Taurani pegs Blinkit’s total addressable market at 60 per cent of India’s entire e-commerce market:a TAM that includes FMCG, grocery and general merchandise categories worth tens of billions of dollars. The kirana channel, with its 13-14m corner shops, remains dominant. Quick commerce replicates that proximity edge via dark stores:micro-warehouses scattered across cities:while offering selection no corner shop can match.

The model is not cheap. Take rates:the commission and advertising revenue platforms extract from brands:range from 15 per cent for large FMCG companies to a punishing 40 per cent for smaller direct-to-consumer brands. That includes discounts of 10-15 per cent, platform commissions of 12-14 per cent, and advertising spend of seven to eight per cent. For D2C brands, it is a Faustian bargain: quick commerce offers unmatched reach and AI-driven micro-targeting that delivers returns dwarfing traditional media, but at a price that makes modern trade look merciful.

Large brands, meanwhile, are hedging their bets. Quick commerce accounts for just one per cent of revenue for most big consumer goods firms on a pan-India basis:two to three per cent for the overall market:limiting their bargaining power vis-à-vis platforms. But advertising on these platforms delivers returns that dwarf social media, video or traditional channels. Brands are shifting ad budgets accordingly, even as they fret about ceding control to platform overlords.

Taurani’s intrinsic valuation, using discounted cash flow analysis, pegs Zomato’s food business at Rs 1,35,000 cr and Blinkit at Rs 2,00,001 cr, implying 54 times FY28 EBITDA for the food arm. The math assumes food delivery user penetration triples from 0.76 per cent of India’s population today to 3.5 per cent over the next decade, still well shy of the 5.5 per cent global average for platforms like DoorDash, Meituan and Uber Eats. For Blinkit, assumptions are bolder: user penetration could hit eight to 10 per cent of the population, driven by expanding non-metro markets and the platform’s vastly wider use case versus food delivery.

Dark stores are spreading, but their economics remain murky outside metro markets. Non-metro cities generate 40-50 per cent lower throughput per dark store, forcing platforms to cherry-pick locations carefully. The current count: 8,000-10,000 dark stores nationwide. That could explode if smaller cities adopt quick commerce at metro-like rates, but metro markets took three to four years to hit critical mass. Non-metros could take double that.

Regulatory risk looms. A draft code of conduct bill proposes welfare contributions pegged at either two per cent of platform revenue or five per cent of gig worker payouts, whichever is higher. For Zomato and Swiggy, that translates to Rs200-250cr annually:they already pay around Rs100cr. The incremental hit: Rs2-3 per order, likely passed to customers. Taurani reckons Zomato, with fatter margins and a more affluent customer base, can weather this better than Swiggy. The bill has been tabled but not implemented; timelines stretch four to six months. Southern states like Karnataka, Telangana and Tamil Nadu are pushing for higher payouts, sparking gig worker strikes in December and late December. Platforms refused to negotiate, waiting for legal clarity. The strikes barely dented order volumes; platforms simply paid Rs100-150 incentives that day versus the usual Rs90-200 during festive periods.

Of one crore gig workers in India, 25-30 lakh work in food tech and quick commerce. The December strike mobilised just two lakh workers:less than 10 per cent of the segment. Platforms are playing a waiting game: once the bill is law, workers’ bargaining power collapses.

Competition is heating up. E-commerce giants are muscling into quick commerce, but their DNA is wrong. Flipkart is burning cash on aggressive discounting; Amazon is focused on execution, not price wars. Quick commerce and e-commerce operate on fundamentally different lead-time models:10 minutes versus one to two days. Unless e-commerce players grab 10-12 per cent of the quick commerce market, they pose no existential threat. Over the past 12 months, Blinkit and Instamart have held 80 per cent-plus market share.

The wildcard is foreign competition. China’s Meituan, the quick commerce titan, is reportedly eyeing India. Its advantages: digital-first DNA and food delivery experience, which involves shorter lead times than traditional e-commerce. Its handicaps: late entry into a land-grab business that rewards hyper-local knowledge of micro-markets, plus potential foreign ownership restrictions that could hobble its one-party inventory model. Incumbents like Blinkit and Zepto, competing on execution rather than discounts, may have moats deep enough to fend off interlopers. Zepto’s price-led strategy, Taurani notes, is “not sustainable”.

Nykaa offers a cautionary tale. It is growing gross merchandise value at 27-28 per cent, but core beauty and personal care growth is sub-25 per cent once the B2B business is stripped out. Quick commerce has dented its margins, not its growth, because Nykaa’s own quick commerce push is protecting market share. The stock trades at a “hefty premium”; analysts reckon it is a hold at current levels, buyable only on dips at 30 per cent growth sustainability.

Zomato is in the 15th-to-17th-year window where internet platforms cross into steady profitability. Global peers took 14-15 years to hit breakeven, then another five to 10 years to reach mature margins. Zomato’s food business is there; Blinkit will arrive in three to five years. On a steady-state basis, Taurani forecasts Zomato EBITDA margins of five to seven per cent within five years:short of Amazon’s double-digit margins, which include AWS, but respectable for a pure consumer tech play.

The EV-to-sales methodology works for companies still scaling towards profitability; once margins stabilise, valuation pivots to PE or EV-EBITDA multiples. Zomato’s food arm is ready for that shift. Blinkit needs another few years. For now, investors are betting on a land grab that pays off in a $1trn retail market where online penetration is still in the single digits. The bonfire of cash is still burning. How long it lasts:and whether Zomato emerges as India’s true Amazon:is the Rs 2,85,000cr question.

Brands

Netflix India names Rekha Rane director of films and series marketing

Streaming giant bets on a seasoned marketer who helped build Amazon and Netflix into household names

MUMBAI: Netflix has put a proven brand builder at the helm of its films and series marketing in India, naming Rekha Rane as director in a move that signals sharper focus on audience growth and cultural cut-through in one of its most hotly contested markets.

Rane steps into the role after seven years at Netflix, where she has quietly shaped how the platform sells stories to India. Her latest promotion, effective February 2026, crowns a run that spans brand, slate and product marketing across originals, licensed content and new verticals such as games.

A strategic marketing and communications professional with roughly 15 years’ experience, Rane has spent much of her career building technology-led consumer businesses and new categories, notably e-commerce and subscription video on demand. She was part of the early push that introduced Amazon.in, Prime Video and Netflix to Indian homes, then helped turn them into everyday brands.

At Netflix, she most recently served as head of brand and slate marketing for India from March 2024 to February 2026, leading teams across media and marketing for global and local content portfolios. Before that, as manager for original films and series marketing, she led IP creation and go-to-market strategy for titles including Guns and Gulaabs, Kaala Paani, The Railway Men* and The Great Indian Kapil Show, spanning both binge and weekly-release formats.

Her earlier Netflix roles covered product discovery and promotion in India and integrated campaign strategy to drive conversations around the content slate, product awareness and brand-equity metrics.

Before Netflix, Rane logged more than three years at Amazon in brand marketing roles in Bengaluru. There she handled national and regional campaigns for Amazon.in, worked on customer assistance programmes in growth geographies and contributed to the go-to-market strategy for the launch of Prime Video India.

Her career began well away from streaming. At Reliance Brands in Mumbai, she worked on retail marketing for Diesel and Superdry. A stint at Leo Burnett saw her work on primary research for P&G Tide, mapping Indian shoppers’ paths to purchase. Earlier still, at Orange in the United Kingdom, she rose from sales assistant to store manager, running a team and owning monthly P&L for a retail outlet.

The arc is telling. As global streamers fight for attention in a crowded Indian market, executives who understand both mass retail behaviour and digital habit-building are prized. Rane’s career sits at that intersection.

For Netflix, the bet is simple: in a market spoilt for choice, sharp marketing can still tilt the screen. And with Rane now leading the charge, the streamer is signalling it wants not just viewers, but fandom.

Brands

Orient Beverages pops the fizz with steady Q3 gains and rising profits

Kolkata-based beverage maker reports stronger revenues and profits for December quarter.

MUMBAI: A fizzy quarter with a steady aftertaste that’s how Orient Beverages Limited, the company that manufactures and distributes packaged drinking water under the brand name Bisleri closed the December 2025 period, as the Kolkata-based drinks maker reported improved revenues and a healthy rise in profits, signalling operational stability in a competitive beverage market.

For the quarter ended December 31, 2025, Orient Beverages posted standalone revenue from operations of Rs 39.98 crore, up from Rs 36.42 crore in the previous quarter and Rs 33.53 crore in the same quarter last year. Total income for the quarter stood at Rs 42.24 crore, reflecting consistent demand and stable pricing across its beverage portfolio.

Profit before tax for the quarter came in at Rs 3.47 crore, a sharp improvement from Rs 1.31 crore in the September quarter and Rs 0.39 crore a year ago. After accounting for tax expenses of Rs 0.79 crore, the company reported a net profit of Rs 2.68 crore, nearly three times the Rs 0.99 crore recorded in the preceding quarter.

On a nine-month basis, the momentum remained intact. Revenue from operations for the period ended December 31, 2025 rose to Rs 117.66 crore, compared with Rs 106.95 crore in the corresponding period last year. Net profit for the nine months climbed to Rs 5.51 crore, more than double the Rs 2.18 crore reported in the same period of the previous financial year.

The consolidated numbers told a similar story. For the December quarter, consolidated revenue from operations stood at Rs 45.06 crore, while profit after tax came in at Rs 2.06 crore. For the nine-month period, consolidated revenue touched Rs 133.57 crore, with net profit of Rs 4.49 crore, underscoring the group’s improving profitability trajectory.

Operating expenses remained largely controlled, with cost of materials, employee benefits and other expenses broadly aligned with revenue growth. The company continued to operate within a single reportable segment beverages simplifying its cost structure and reporting framework.

The unaudited financial results were reviewed by the Audit Committee and approved by the Board of Directors at its meeting held on 7 February 2026. Statutory auditors carried out a limited review and reported no material misstatements in the results.

In a market where margins are often squeezed by input costs and competition, Orient Beverages’ latest numbers suggest the company has found a reliable rhythm not explosive, but steady enough to keep the fizz alive.

Brands

BCCL profit jumps 53 per cent in FY25 as tax bill shrinks

Revenue rises 4.3 per cent to Rs 10,209.33 crore while deferred tax gain lifts bottom line sharply

NEW DELHI: Bennett, Coleman and Company (BCCL) has posted a sparkling set of financial results for the year ended 31 March 2025, proving that there is still plenty of ink and gold left in the ledger.

Revenue from operations climbed a steady 4.3 per cent, reaching Rs 10,209.33 crore compared to Rs 9,786.44 crore the previous year. When you sprinkle in other income, which rose 8.9 per cent to Rs 949.36 crore, the total income for the media behemoth hit a healthy Rs 11,158.69 crore.

While the income grew at a modest pace, the bottom line tells a far more dramatic story. The real headline is the 53 per cent surge in annual profit. How did they pull off such a feat? While Profit Before Tax (PBT) saw a gentle nudge upward of 2.7 per cent to Rs 1,610.00 crore, it was a vanishing act by the taxman that really did the trick.

Total tax expenses plummeted by 32.4 per cent, dropping from Rs 468.76 crore down to Rs 316.97 crore. This was largely thanks to a swing in deferred tax, moving from an expense of Rs 156.02 crore in FY24 to a benefit of Rs 39.44 crore this year.

Total income rose from Rs 10,658.55 crore in FY24 to Rs 11,158.69 crore in FY25, marking a 4.7 per cent increase. Total expenses grew at a slower pace, up 3.0 per cent from Rs 9,306.06 crore to Rs 9,581.45 crore. Profit before tax inched up 2.7 per cent, moving from Rs 1,567.02 crore to Rs 1,610.00 crore. However, the standout figure was net profit, which jumped sharply by 53.0 per cent, climbing from Rs 1,042.03 crore in FY24 to Rs 1,594.73 crore in FY25.

Despite the rising costs of doing business across the globe, BCCL kept a tight grip on the purse strings. Total expenses rose by just 3.0 per cent to Rs 9,581.45 crore. By keeping costs lower than the rate of income growth, the company ensured that the final figure, a net profit of Rs 1,594.73 crore, was nothing short of a front-page sensation.

In a world of shifting digital tides, it seems the BCCL ship is not just steady, but sailing into significantly wealthier waters.

MIB sets OTT accessibility rules, mandates captions and audio description

Boney Kapoor acquires remake rights of Tamil political satire Thalaivar Thambi Thalaimaiyil

Netflix India names Rekha Rane director of films and series marketing

Zabeen signs off from TV9 after shaping the network’s public voice

Dhawan steps up to bat for Delhi’s grassroots sports push

Orient Beverages pops the fizz with steady Q3 gains and rising profits

Cheekatilo shines in the dark with record debut on Prime Video

These ’90s fashion trends are making a comeback in 2017

The final 6 ‘Game of Thrones’ episodes might feel like a full season

According to Dior Couture, this taboo fashion accessory is back

The old and New Edition cast comes together to perform

Phillies’ Aaron Altherr makes mind-boggling barehanded play

Uber and Lyft are finally available in all of New York State

Disney’s live-action Aladdin finally finds its stars

MIB sets OTT accessibility rules, mandates captions and audio description

Boney Kapoor acquires remake rights of Tamil political satire Thalaivar Thambi Thalaimaiyil

Netflix India names Rekha Rane director of films and series marketing

Zabeen signs off from TV9 after shaping the network’s public voice

Dhawan steps up to bat for Delhi’s grassroots sports push

Orient Beverages pops the fizz with steady Q3 gains and rising profits

Cheekatilo shines in the dark with record debut on Prime Video

-

News Broadcasting7 days ago

News Broadcasting7 days agoMukesh Ambani, Larry Fink come together for CNBC-TV18 exclusive

-

I&B Ministry3 months ago

I&B Ministry3 months agoIndia steps up fight against digital piracy

-

iWorld1 week ago

iWorld1 week agoNetflix celebrates a decade in India with Shah Rukh Khan-narrated tribute film

-

MAM3 months ago

MAM3 months agoHoABL soars high with dazzling Nagpur sebut

-

Hollywood4 days ago

Hollywood4 days agoThe man who dubbed Harry Potter for the world is stunned by Mumbai traffic

-

iWorld12 months ago

iWorld12 months agoBSNL rings in a revival with Rs 4,969 crore revenue

-

iWorld3 months ago

iWorld3 months agoTips Music turns up the heat with Tamil party anthem Mayangiren

-

MAM7 days ago

MAM7 days agoNielsen launches co-viewing pilot to sharpen TV measurement