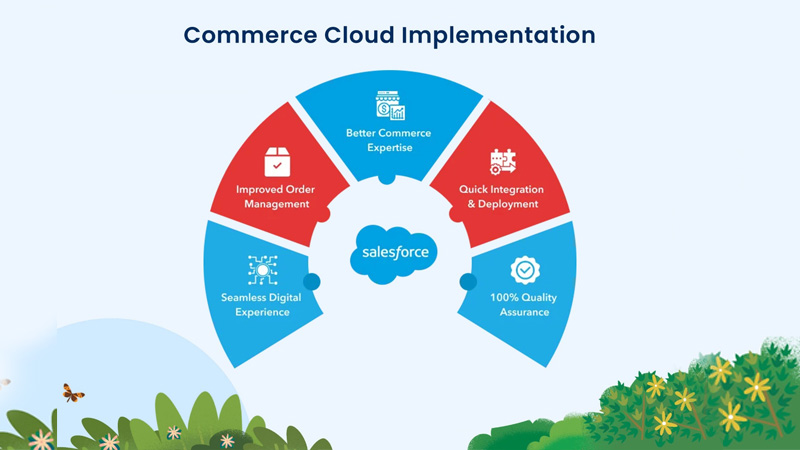

Customer Relationship Management (CRM) is where the business and nonprofit operations of today are beginning. Salesforce is the strongest and most enduring CRM system, allowing organizations...

Ever noticed that extra charge at the petrol pump? When you swipe your card to fill fuel, there’s often a little more added to your bill...

The Wipro share price has been an interesting subject for many investors, especially within the Indian market. As one of the leading IT services companies in...

A hidden treasure that offers an incredible escape from the bustle of the city is located just outside of Bengaluru, in the middle of Karnataka’s lush...

Taj Lands End has been very strategically located in the upscale neighbourhood of Bandra in Mumbai and stands as one of the iconic and luxurious five-star...

Cricket is already recognised as one of the biggest sports in India and New Zealand, so it’s hard to believe it’s still growing. However, that is...

With temperatures rising and power bills high, Indian households are rethinking how they can stay cool. While the traditional fan remains a familiar fixture in homes,...

Choosing the right insurance provider for your commercial vehicles is essential for protecting your business operations. With numerous insurers offering varied plans, it’s important to compare...

Growing older is a beautiful part of life—marked by wisdom, experience, and often, more time to enjoy the things that truly matter. But with age also...

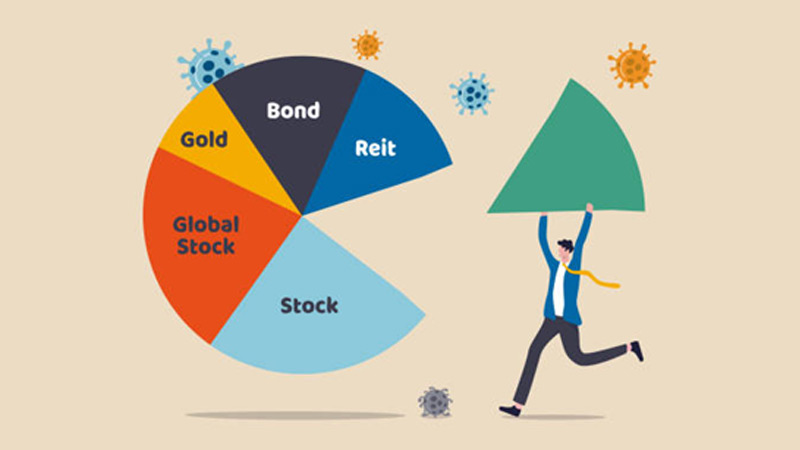

When investing, finding the perfect balance between risk and reward is important for long-term wealth creation. Mutual funds are a powerful financial product for investors seeking...

A home is not only four walls; it is a person’s personality, lifestyle, and aspirations. Introducing Asense Interior, the home remodelling trendsetter, where every design is...

Infertility is a deeply emotional and challenging journey for 15% of Married Couples in India. With the right medical expertise, your hope of becoming parents can...

Rummy is quite a popular game in India and other countries. It has inspired multiple variants like: 1. Points Rummy 2. Pool Rummy 3. Gin Rummy...

You must have heard this popular saying “A good teacher is like a candle—it consumes itself to light the way for others.” This is so true...

The share market often rewards those who keep an eye on new opportunities. In recent months, several companies have made headlines by doubling investors’ wealth within...

Paridhi Bhatiya created and led Ogilvy’s Content Force for the last five years. She is stepping down from her role on 28th April 2025, marking the...

India is home to some of the world’s biggest tech companies, and over the past few years, the country has repositioned itself as a new major...

Dubai, with its iconic luxurious lifestyle and automobile marketplace, has become a dream city for car enthusiasts and buyers willing to pay a fair price for...

A honeymoon is more than just a vacation – it’s the first big adventure of your married life. Travelling abroad offers new cultures, dreamy landscapes, and...

Imagine wanting to get life insurance but dreading the process—calls from agents, endless paperwork and confusing terms that leave you with more questions than answers. Sounds...

Personal Loans are funding options for managing unexpected expenses and achieving financial goals. Those with a regular income and stable employment are the candidates for Personal...

While it may seem like a challenge, prepayment helps you clear the debt faster, and the savings in interest can make a big difference in the...

India’s life insurance market has witnessed substantial growth over the past decade. The rise in disposable incomes, increased awareness about financial security, and favorable government regulations...

When you’re self-employed, you handle everything—your income, your business, and your family’s financial security. There’s no company insurance or fixed salary to rely on. That’s why...

Logistics, construction, and agricultural businesses need tractors for seamless business operations. Having a commercial fleet of tractors makes it easier to run the business, but owning...

Self-employment is rapidly becoming one of the top choices among job seekers and businesspeople. It is one of the few employment opportunities where you need not...

Healthcare-related sectors can offer varied growth opportunities to investors because it blends both defensive and cyclical elements. Defensive stocks, such as pharmaceuticals and healthcare facilities, tend...

If you qualify yourself as a bike enthusiast, your bike is definitely more than just a mode of transport for you. It is your passion, a...

Investing your capital in mutual funds through a lumpsum investment can be rewarding, but you must understand the risks and benefits involved. When aligned with long-term...

Traveling is one of the most exciting and rewarding experiences in your life. It allows you to explore different cultures, traditions, places, history, and even discover...

Abu Dhabi-based technology investment company MGX has made a record-breaking $2 billion investment in the leading cryptocurrency exchangeBinance. The transaction, conducted in an unnamed stablecoin, marks...

The crypto market is no stranger to major hacks, but the recent Bybit theft set a staggering new record. North Korea-affiliated hackers from the notorious Lazarus...

Tea is not a beverage-tours of the globe for tens of millions, it’s an experience, a comfort, a lifestyle. From the rich black to begin the...

Bangalore, the Silicon Valley of India, is one place that truly celebrates luxury, elegance, and style in the lifestyle while being the heart of creativity and...

Online gaming has become a major source of entertainment among multiple individuals. Whether it’s an intense multiplayer showdown or an immersive role-playing game, players demand seamless...

MUMBAI: In an era where news doesn’t just report events but shapes them, Live Times, India’s first global multicast news hub, is setting the standard for...

Commercial vehicle insurance is a kind of policy designed to protect businesses and individuals who use vehicles for commercial purposes. Unlike private vehicle insurance, it offers...

In the auto repair industry, customer trust and satisfaction are paramount. A key element in fostering both of these qualities is clear and transparent communication, which...

Investing in an SIP has become a popular long-term way to generate good returns. It uses rupee cost averaging to manage market volatility. Instead of investing...

Biometric authentication is transforming the way we secure our digital identities, offering a seamless and highly secure alternative to traditional passwords and PINs. From unlocking smartphones...

With the Competition Commission of India (CCI) launching an investigation into Google’s restrictive policies on real-money gaming (RMG) applications, India’s digital gaming industry is witnessing a...

Forex trading in India has gained significant traction over the years, with an increasing number of individuals exploring the currency markets to diversify their portfolios and...

Since its launch in 2019, the Hyundai Venue has emerged as one of India’s most popular subcompact SUVs. Its smart looks, feature-rich cabin, multiple engine-gearbox options,...

Tax planning is challenging, especially when required to deal with new and old regimes, income tax slabs, deductions and exemptions. Understanding these is crucial to saving...

Kolkata : Zupee, India’s leading skill-based gaming platform launched a week-long gaming festival – Ludo Fest on Monday, 10th February. Zupee Ludo Fest is a series...

Choosing the right funding option is tricky when you need funds to handle an emergency or fulfil a dream. Personal Loans and instant loans are the...

Everyone dreams of travelling the world, exploring diverse places, meeting new people, experiencing unique cultures, and savouring different cuisines. However, financial constraints often stand in the...

Weddings are one of life’s most significant milestones, but they come with significant expenses from catering and venue to photography and décor. Even with meticulous budgeting,...

If you have invested in a ULIP scheme (or are planning to do so), you might have had a few nagging concerns! They could be, “What’s...

A dependable and fast internet connection is a necessity nowadays. As smart devices increasingly dominate our lives and high-speed internet fuels activities from gaming to streaming,...

Reliance and BlackRock chiefs map the future of investing as global capital eyes India

Super Bowl pilot to refine how shared TV audiences are counted

MUMBAI: Netflix is celebrating ten years in India with a slick anniversary film voiced by Shah Rukh Khan, a nostalgic...

Gurugram: Delhivery’s boardroom is being reset. Deepak Kapoor, chairman and independent director, has resigned with effect from April 1 as...

SINGAPORE: Anuvrat Rao has taken charge as APAC head of commerce and signals partnerships at Meta, steering monetisation deals across...

Bengaluru: Brnd.me, the global consumer brands company formerly known as Mensa Brands, has entered the European market following strong momentum...

NATIONAL: TechnoSport has launched on Slikk, the ultra-fast fashion app offering 60-minute delivery, as the activewear brand accelerates its push...

MUMBAI: Jitendra Singh has been appointed senior vice president and division head – special projects at Reliance Industries Limited, marking...

MUMBAI: Dating, it turns out, is less about grand gestures and more about shared moments. The song you both hum,...

MUMBAI: This Republic Day, Godrej brought modern washing technology to the care of Indian handlooms. The appliances business of Godrej...

BENGALURU: Wipro Limited hosted the 15th edition of the Wipro earthian Awards 2025 at Azim Premji University, recognising schools and...

Gurugram: Blinkit has elevated Tulasi Mohan Padavala to associate director, capping a three-year climb inside the quick-commerce firm and signalling...

Noida: Haldiram’s has tapped a seasoned brand builder to sharpen its quick-service ambitions. Rajiv Singh has joined the snacks-to-sweets giant...

MUMBAI: When the stakes rise and seconds matter, even payments need a match-winning finish. That’s the cue for Bharatpe, which...

BENGALURU: In a city where red lights usually test patience and tempers, Oben Electric decided to give them a new job....