Connect with us

The need for a local Indian phone number is a common challenge for global businesses, travelers, and privacy-conscious individuals in 2025. The decision to buy an...

Applying for a UAE visa entails more than simply forms and documentation. True copy attestation is an important step that many expats tend to overlook. Without...

In today’s evolving financial ecosystem, a loan against property (LAP) has become one of the most reliable instruments for accessing large sums of money. Whether it...

When you choose a health insurance plan or renew an existing one, how do you determine that it’s the right one for you? You might rely...

Owning a vehicle comes with more than just the freedom to travel at will—it also comes with legal responsibilities. One of the most important is having...

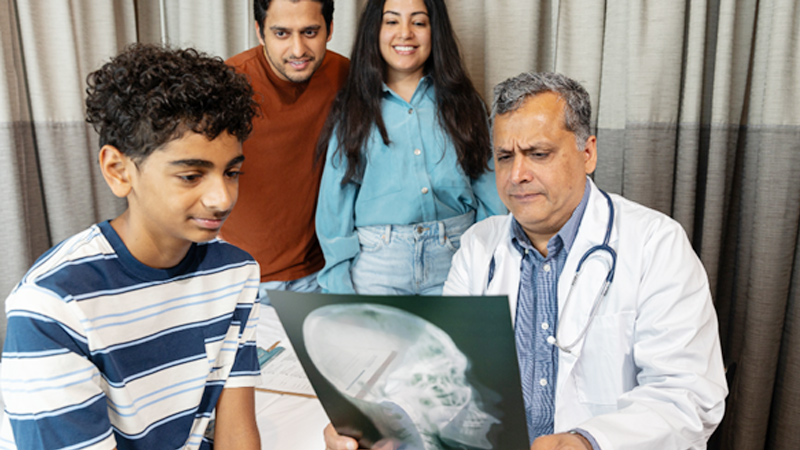

As medical costs continue to rise, opting for the right insurance plan has become a necessity. While choosing a plan, people often find the process challenging...

When you plan to take a personal loan, one of the first questions that comes to mind is – how much extra will I end up...

In India, the world of finance is always changing, especially when you look at life insurance and ways to save on taxes. ULIP plans and term...

Astrology has always been part of daily life in many cultures, and today, its online presence continues the traditional values with emerging technology. This shift helps...

KathaVersse, the content IP company on a mission to build a “Marvel for Bharat”, has appointed Ravi Luthria as its Chief Revenue Officer. An IIM Lucknow...

Retirement planning supports a structured financial approach for salaried and self-employed individuals. It allows individuals to prepare for future income needs after their active working years...

Have you ever wondered why some investors look beyond financial statements before picking shares? In recent years, ESG factors, environmental, social, and governance considerations, have become...

In a media landscape dominated by fiction and celebrity, Game of Change is flipping the script. Premiered across Mumbai, Hyderabad, and Chennai, this new-age docufilm series...

There are many life situations where you might have to seek legal guidance. Divorce, prenuptial agreements, estate planning, business formation, contract disputes, personal injuries, and criminal...

For many years, fixed deposits (FDs) have been a trustworthy method for building your savings safely and sustainably. FDs provide guaranteed returns and do not require...

Building a good savings habit is important to secure your financial future. Savings help you in emergencies and they also let you enjoy a quality life....

The Indian monsoon season is generally accompanied by torrential rainfall, floods, landslides, hailstorms and high humidity. All these can seriously damage your car, causing corrosion, engine...

As Bitcoin continues to dominate headlines with its dramatic price surges, institutional adoption, and volatile swings, many retail investors are left asking the same question: Did...

MUMBAI: Serial growth specialist and former AltBalaji, Z5 and Google Appscale mentor Divya Dixit has taken over as chief executive officer of Recz, a luxury-focused consumertech...

Explore how tracking gold rates in Bangalore can help you make smart borrowing decisions. Get quick funds against your gold and enjoy exclusive cashback during the...

Indian TV is no longer just for Indian households. Viewers from the U.S., UK, Canada, and Australia are tuning in like never before. Shows from Mumbai,...

Parents have the responsibility of ensuring long-term financial security for their family, even in their absence. While parents strive to provide comfort, stability, and opportunities for...

New Delhi [India], July 16: Thinking about making an addition to your family, or want to start a family? Well, it may be a wake-up call...

In today’s digital world, applying for a personal loan is quicker than ever. But before you commit to borrowing, it’s essential to know how much you’ll...

MUMBAI: After a bit of a cool-down, the crypto market is once again buzzing with talk of the next big bull run. Of course, anyone who’s...

Let’s be real-if you’re a movie lover, there’s a high chance that YouTube is your second favorite cinema screen. Whether you’re into movie facts, behind-the-scenes stories,...

Stylish design and impressive camera performance are two strong points of vivo’s V series smartphones, and the latest V50 5G is no different. The vivo V50...

The best family term insurance plans help you and your loved ones in many ways. While it helps you plan your finances during your lifetime, it...

In a major development in the branding and communication space, Teamology Softech and Media Services, one of India’s fastest-growing digital PR consultancies, has been awarded the...

Insurance is an important tool to secure your loved ones’ future. Among the most common types are term insurance and life insurance. While both offer financial...

In the ever-changing world of remote work, hybrid schedules, Teams meetings, and back-to-back calls on the move, one thing is non-negotiable: a solid pair of earbuds....

PUNE : Vijaya Diagnostics, a leading name in healthcare diagnostics, has been making waves in the medical imaging industry by providing fast, reliable, and highly accurate...

MUMBAI — Crypto exchange heavyweight Bybit has inked a deal to become title sponsor of the India Blockchain Tour (IBT) 2025 — a high-octane, eight-city Web3...

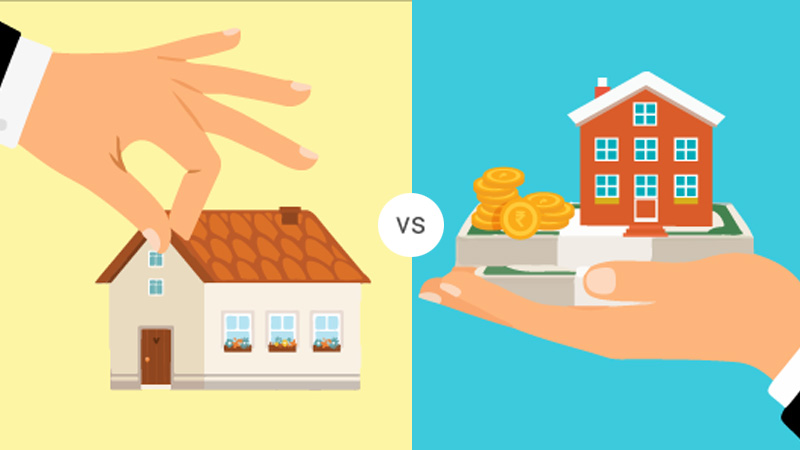

Buying a home tends to be the single biggest financial commitment most people ever take on. Because property prices are high, many buyers rely on a...

The National Pension System (NPS) is a retirement savings instrument that offers attractive tax benefits to encourage people to save for their golden years. However, there...

Retirement is a phase when you want to spend quality time with your family and pursue your long-due dreams. However, it requires financial stability as a...

Choosing the right mutual fund from the many options in India can feel daunting. Picking one based only on high returns might not suit your financial...

MUMBAI: Sagar Panda has joined Lokal App as Regional Head – Digital Business – West & North India Market. With nearly two decades of experience in...

Every year, as the first raindrops hit the Indian roads, drivers breathed relief from the summer heat. But soon after, a familiar set of challenges –...

Father’s Day is around the corner and if you’ve been waiting to surprise your dear Dad, now is the time to come up with the best...

When it comes to investing funds in India, two of the most popular options are Mutual Funds and the Public Provident Fund (PPF). Both are widely...

How to analyse sporting events and make accurate football bets at MostBet India The simple design, decreasing the possibility of competitive odds but also, new bonuses...

The 25th wedding anniversary, known as the Silver Jubilee marks a special moment to celebrate the first quarter of married life together. Picking the right 25th...

Video watermarking is now a crucial tool for content creators and companies looking to safeguard their intellectual property in the current digital world. With video content...

Travelling comes with its fair share of uncertainties. Losing your baggage is one of the most common inconveniences that can disrupt your trip. This is where...

Gambling has a rich cultural backdrop in India, from traditional games like Teen Patti and Rummy to modern online platforms offering cricket betting and casino games....

Travelling to Thailand offers a mix of adventure, culture, and tropical relaxation. From bustling markets in Bangkok to serene islands like Phi Phi and Koh Samui,...

Owning a bike in India means more than just enjoying the convenience of zipping through traffic—it also comes with legal responsibilities. A two-wheeler insurance policy acts...

For a large number of Indians, a home holds more value than it implies as far as a milestone. Instead, a home is a sign of...

From breakfast biscuits to smartphones, the everyday products we use often travel hundreds of kilometres before they reach us. Behind this smooth delivery system is an...

Reliance and BlackRock chiefs map the future of investing as global capital eyes India

Super Bowl pilot to refine how shared TV audiences are counted

MUMBAI: Netflix is celebrating ten years in India with a slick anniversary film voiced by Shah Rukh Khan, a nostalgic...

Gurugram: Delhivery’s boardroom is being reset. Deepak Kapoor, chairman and independent director, has resigned with effect from April 1 as...

SINGAPORE: Anuvrat Rao has taken charge as APAC head of commerce and signals partnerships at Meta, steering monetisation deals across...

Bengaluru: Brnd.me, the global consumer brands company formerly known as Mensa Brands, has entered the European market following strong momentum...

NATIONAL: TechnoSport has launched on Slikk, the ultra-fast fashion app offering 60-minute delivery, as the activewear brand accelerates its push...

MUMBAI: Jitendra Singh has been appointed senior vice president and division head – special projects at Reliance Industries Limited, marking...

MUMBAI: Dating, it turns out, is less about grand gestures and more about shared moments. The song you both hum,...

MUMBAI: This Republic Day, Godrej brought modern washing technology to the care of Indian handlooms. The appliances business of Godrej...

BENGALURU: Wipro Limited hosted the 15th edition of the Wipro earthian Awards 2025 at Azim Premji University, recognising schools and...

Gurugram: Blinkit has elevated Tulasi Mohan Padavala to associate director, capping a three-year climb inside the quick-commerce firm and signalling...

Noida: Haldiram’s has tapped a seasoned brand builder to sharpen its quick-service ambitions. Rajiv Singh has joined the snacks-to-sweets giant...

MUMBAI: When the stakes rise and seconds matter, even payments need a match-winning finish. That’s the cue for Bharatpe, which...

BENGALURU: In a city where red lights usually test patience and tempers, Oben Electric decided to give them a new job....