Connect with us

BENGALURU: 21st Century Fox reported that international affiliate revenue increased 11 percent driven by rate and subscriber growth at both FNG International and Star India for...

BENGALURU: Indian multi system operator (MSO) and broadband internet services (broadband) provider GTPL Hathway Limited (GTPL) has reported a year-over-year (y-o-y) growth in standalone as well...

BENGALURU: Siti Networks Limited (Siti) reported higher revenue and operating profit (EBIDTA) for the quarter ended 30 September 2017 (Q2-18, current quarter) as compared to the...

BENGALURU: The demerged Hathway Cable and Datacom Limited (Hathway) reported standalone profit before tax (PBT) of Rs 140.1 million for the quarter ended 30 September 2017...

BENGALURU: Airtel Digital TV services (Airtel DTH), the DTH segment of Indian telecom major Bharti Airtel Limited (Airtel), saw revenue grow 10 percent for the quarter...

BENGALURU: The Essel group’s news arm – Zee Media Corporation Limited (ZMCL) reported higher revenue, but lower profit after tax for the quarter ended 30 September...

BENGALURU: Indian cinema chain Inox Leisure Limited (Inox) has reported improved revenue and net profit after tax (PAT) for the quarter ended 30 September 2017 (Q2-18,...

BENGALURU: Indian entertainment and exhibition company PVR Limited (PVR) reported a slight decline in total revenue for the quarter ended 30 September 2017 (Q2-18, current quarter)...

BENGALURU: Time Warner Inc., (Time Warner) reported increase in revenues and income – both operating as well as adjusted – due to increase across these parameters...

BENGALURU: Indian media group HT Media Limited (HT Media) reported a drop in consolidated revenues and increase in consolidated profits for the quarter ended 30 September...

BENGALURU: The Subhash Chandra led Zee Entertainment Enterprises Limited (Zeel) reported a 2.9 percent increase in advertising revenue for the quarter ended 30 September 2017 (Q2-18,...

BENGALURU: Indian integrated media content house Shemaroo Entertainment Limited (Shemaroo) reported 8.6 percent higher y-o-y consolidated Total Revenue for the quarter ended 30 June 2017 (Q1-17,...

BENGALURU: A forty four percent year-on-year (y-o-y) decline in carriage fees and a thirty five percent y-o-y decline in internet subscription fees for the quarter ended...

BENGALURU: The Essel Group’s television direct to home (DTH) Dish TV India Limited (Dish TV) reported 5 percent and 5.1 percent declines in subscription and operation...

BENGALURU: Restructuring at Indian multi system operator (MSO) Hathway Cable and Datacom Limited (Hathway) has brought for it a positive bottomline. The pared company reported a...

BENGALURU: Hong Kong based telecommunications, media, IT solutions, property development and investment and other businesses group PCCW Limited reported lower numbers for its video operations comprising...

BENGALURU: Sun TV Network Limited (Sun TV) reported improved numbers across all important parameters for the quarter ended 30 June 2017 (Q1-18, current quarter) as compared...

BENGALURU: After the sale of certain investments and restructuring and integration costs in the previous fiscal (FY-17), including in the quarter ended 30 June 2016 (Q1-17),...

BENGALURU: After declaring a maiden 10 percent dividend for the previous fiscal, Indian Multi-System Operator (MSO) and Broadband Internet Services (broadband) provider GTPL Hathway Limited has...

BENGALURU: After three consecutive profitable quarters in fiscal 2017 (year ended 31 March 2017, FY-17), Indian direct to home Saurabh Dhoot led major Videocon d2h Limited...

BENGALURU: India FM Radio company Music Broadcast Limited (MBL) or Radio City reported higher revenue and improved profits for the year ended 31 March 2017 (FY-17,...

BENGALURU: Videocon d2h Limited (Videocon d2h) led by executive chairman Saurabh Dhoot reported its maiden annual net profit for the year ended 31 March 2017 (FY-17,...

BENGALURU: The Anurradha Prasad led B. A. G. Films and Media Limited (BAG Films) reported improved revenue and profit after tax (PAT) for the year ended...

BENGALURU: Siti Networks Limited (Siti) reported 4.4 percent growth in revenue for the year ended 31 March 2017 (FY-17, current year or fiscal) as compared to...

BENGALURU: Sun TV Network Limited (Sun TV) reported improved numbers across all important parameters for the year ended 31 March 2017 (FY-17, current year, fiscal) as...

BENGALURU: The Sunil Lulla led Eros International Media Limited (Eros) reported 7.9 percent growth of consolidated profit after tax attributable (PAT) to Eros shareholders for the...

BENGALURU: TV Today Network Limited (TVTN) reported greatly improved consolidated results for the year ended 31 March 2017 (FY-17, current year). The Arun Purie controlled company’s...

BENGALURU: The Ekta Kapoor led Balaji Telefilms Limited (Balaji Telefilms) had 8 shows on air at the end of the financial year 2017 (FY-17, current year,...

BENGALURU: Indian multi system operator (MSO) Den Network reported 21.8 percent increase in operating revenue for its Cable distribution (cable) business for the year ended 31...

BENGALURU: Atria Convergence Technologies Pvt. Ltd (ACT) leads in wired broadband internet subscribers additions in calendar year 2017 (CY-17) until 31 March 2017 (Mar-17) as per...

BENGALURU: The Bibhu Prasad Rath led Ortel Communications Limited (Ortel) reported less than one tenth profit after tax (PAT) for the year ended 31 March 2017...

MUMBAI: NDTV Group has recorded a net profit of Rs. 5 crore for the quarter compared to a loss of Rs. 1 crore in the same...

BENGALURU: Subhash Chandra’s Zee Entertainment Enterprises Limited (Zeel) reported more than double (2.36 times) consolidated total comprehensive income (TCI)for the year ended 31 March 2017 (FY-17,...

BENGALURU: Time Warner Inc., (Time Warner) reported growth in revenue across all its segments – Turner, Home Box Office (HBO) and Warner Bros in the quarter...

BENGALURU: Sony Corporation (Sony) reported a 1.9 percent or ¥5.5 billion decline in consolidated operating income for the fiscal ended 31 March 2017 (FY-17, current year)...

MUMBAI: Network18’s Q4 results showed a five per cent YoY growth (driven largely by its TV operations) over last year, posting consolidated revenue of Rs 3,471...

BENGALURU: The Sunil Lulla led Eros International Media Limited (Eros) reported almost 2.5 times (2.496 times) consolidated profit after tax (PAT) for the quarter ended 31...

BENGALURU: Prime Focus Limited (PFL) reported consolidated Profit After Tax (PAT) of Rs 22.68 crore (4.5 percent margin) for the period ended 31 December 2016 (Q3-17,...

BENGALURU: Indian private FM player Entertainment Network (India) Limited (ENIL), which runs the Mirchi brand radio network in India, reported 4.9 percent increase in Total Income...

BENBALURU: After a few consecutive quarters during which the Ekta Kapoor run Balaji Telefilms Limited (Balaji Telefilms) reported consolidated operating losses, the company is showing signs...

BENGALURU: Sun TV Network Limited (Sun TV) reported improved numbers across all important parameters for the quarter ended 30 December 2016 (Q3-17, current quarter) as compared...

BENGALURU: Once again following the trends of the first four weeks of 2017, FMCG advertisers hogged most of the ranks (9 out of the top 10...

BENGALURU: Indian multi system operator (MSO) Hathway Cable and Datacom Limited (Hathway) reported 25.5 per cent growth in Total Income from operations (TIO) and 46 percent...

BENGALURU: MukeshAmbani’s Reliance JioInfocomm Limited (Jio) replaced Sunil Mittal’s Bharti Airtel Limited (Airtel) as the largest internet services provider in the country. All the other players...

BENGALURU: MukeshAmbani’s Reliance JioInfocomm Limited (Jio) replaced Sunil Mittal’s Bharti Airtel Limited (Airtel) as the largest internet services provider in the country. All the other players...

BENGALURU: Indian digital cinema distribution network and in-cinema advertising platform, UFO Moviez Limited (UFO) reported a 5.2 percent year-over-year (y-o-y) growth in advertising revenue for the...

BENGALURU: Indian digital cinema distribution network and in-cinema advertising platform, UFO Moviez Limited (UFO) reported a 5.2 percent year-over-year (y-o-y) growth in advertising revenue for the...

BENGALURU: Indian telecom major Bharti Airtel Limited (Airtel) reported 3 percent decline in total revenue for the quarter ended 31 December 2016 (Q3-17, current quarter) as...

BENGALURU: Indian telecom major Bharti Airtel Limited (Airtel) reported 3 percent decline in total revenue for the quarter ended 31 December 2016 (Q3-17, current quarter) as...

BENGALURU: The Subhash Chandra led content and broadcast player Zee Entertainment Enterprises Limited (ZEEL) reported a small hike of 3.1 percent in advertisement revenue in the...

NEW DELHI: Hamdard Laboratories gathered a cross-section of India’s achievers in New Delhi on Friday, handing out the Hakeem Abdul...

MUMBAI: For decades, creative storytelling has been the cornerstone of brand communication. The “big idea” amplified through catchy jingles, striking...

MUMBAI: Zepto has elevated Ahmad Muneeb to vice president – HR centre of excellence, placing him at the helm of...

MUMBAI: When the applause gets louder than the dialogue, you know the fans have taken over. That was the unmistakable...

MUMBAI: As audiences spread across TV, OTT, and short-form platforms, deciding what gets greenlit has become more strategic than ever....

MUMBAI: Jacques Barreau has spent two decades helping Hollywood speak the world’s languages. From The Lord of the Rings to...

INDIA: Dell Technologies is doubling down on artificial intelligence in marketing. The company has elevated Aishwarya Sudhakar to director of...

GURUGRAM: Adidas has appointed Gaurav Pathak as director of key and field accounts, bringing back an executive who began his...

MUMBAI: Myntra has stitched a new thread into its leadership fabric, appointing seasoned technologist Pramod Adiddam as chief technology officer....

A wave of panic swept through Delhi and Mumbai over the past week as viral social media posts claimed a...

MUMBAI: India’s blind women’s cricket team emerged as the standout honouree at the fourth edition of the Zee Samvad with...

MUMBAI: The FMCG arm of Reliance Industries has acquired a majority stake in Australia-based Goodness Group Global, marking its entry...

WASHINGTON: At OpenAI, the fight was not about artificial intelligence going rogue—it was about who got the GPUs.An internal email...

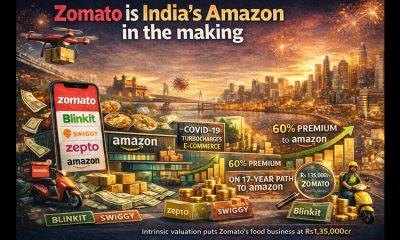

MUMBAI: Zomato, India’s dual-headed monster of food delivery and quick commerce, is marching towards profitability at a clip that puts...

INDIA: From almonds to alcohol, American imports are about to get easier on the Indian wallet. India and the United...