Connect with us

New Delhi: Network18 Media & Investments Ltd reported a consolidated net profit of Rs 121.51 crore for the first quarter ended June 2021. The company had posted a...

MUMBAI: India’s first DTH operator Dish TV India continues to slog it out to get out of the financial quagmire it has got itself into. That’s...

New Delhi : Multiplex major PVR Ltd continues to bear the brunt of the ongoing pandemic, as it recorded a consolidated net loss of Rs 289.12...

New Delhi: ITC Ltd on Tuesday reported a consolidated net profit of Rs 3,816.84 crore for the fourth quarter ended March 2021. The cigarette-FMCG-to-hotel major had...

KOLKATA: Zee Entertainment Enterprises Limited (ZeeL) has posted operating revenue of Rs 1965.8 crore for the fourth quarter. The leading broadcaster has reported a consolidated net...

KOLKATA: Airtel Digital TV, Bharti Airtel’s direct-to-home (DTH) segment has reported Rs 767.3 crore revenue in q4 FY21 compared to Rs 603.5 crore in the corresponding...

New Delhi: Riding on higher sales, FMCG major Colgate-Palmolive India reported a 54.1 per cent jump in its net profit at Rs 314.6 crore for the...

NEW DELHI: Homegrown telecom gear maker HFCL reported net profit of Rs 86.47-crore for the quarter ended 31 March 2021, a 1.6 per cent increase over...

NEW DELHI: FMCG major Dabur India reported Rs 378 crore in net profit for the quarter ending 31 March 2021, a 34 per cent leap compared...

New Delhi: Fox Corporation on Thursday reported increase in quarterly net income which rose to $582 million as compared to the $90 million reported in the prior year quarter. A...

NEW DELHI: FMCG major Hindustan Unilever (HUL) reported a good set of numbers on all fronts for the quarter ending 31 March 2021. Beating market estimates...

New Delhi: Facebook on Thursday reported stronger than expected financial results for the first quarter with soaring ad revenue during the pandemic. The social media giant...

MUMBAI: Automobile manufacturer Maruti Suzuki India’s net profit tumbled 10.7 per cent to Rs 1,166 crore for the quarter ended 31 March 2021. This, despite sales...

NEW DELHI: In the fourth quarter of the financial year that ended on 31 March 2021, TV18, a listed subsidiary of Network 18, has reported a...

KOLKATA: After a year of astounding growth, Netflix has missed the subscriber addition estimates in the first quarter of 2021. The company has added 3.98 million...

NEW DELHI: FMCG major Nestle India posted a strong performance in the opening quarter of 2021, reporting a 14.6 per cent year-on-year growth in its net...

KOLKATA: On the back of strong performance in the fourth quarter of FY21, GTPL Hathway has posted Rs 599.1 crore revenue, up 29 per cent year-on-year....

NEW DELHI: Quint Digital Media Ltd (QDML) has reported positive growth during the quarter ended 31 March 2021, posting a net profit of Rs 45 lakh...

KOLKATA: Multinational media entertainment company Eros STX Global Corporation has reported $144 million revenue million for the six months ended 30 September 2020, compared to $210...

MUMBAI: Despite increased engagement due to shelter-in-place directives in many countries, Facebook experienced a significant reduction in the demand for advertising. After the initial steep decrease...

MUMBAI: It seems Facebook has great ambition for e-commerce and small business in India. While speculations have been rife on the scope of the social media...

Being successful in business involves several inputs. You have to set your business above the competitors' and ensure that you market wisely to make it in...

BENGALURU: The Essel group’s television news broadcasting arm Zee Media Corporation Ltd (ZMCL) reported a 123.1 per cent growth (more than double) in consolidated profit after...

BENGALURU: The Sameer Manchanda-led Indian cable distribution network and broadband internet services (broadband) provider Den Networks Ltd reported 5.3 percent drop in consolidated operating revenue numbers...

Since the dawn of the television industry, you all must have seen hundreds of serial dramas. Over the last three decades, serials have been a major...

BENGALURU: Indian multi-system operator and internet service provider GTPL Hathway Ltd (GTPL) reported 13.8 percent increase in total income for the quarter ended 30 September 2018...

BENGALURU: TV Today Network Ltd (TVTN) reported 3.5 percent year on year (y-o-y) increase in standalone operating revenue at Rs 163.29 crore for the quarter ended...

BENGALURU: Sun TV Network Ltd (Sun TV) reported improved year-on-year (y-o-y) standalone numbers across all important parameters for the quarter ended 30 September 2018 (Q2 2019,...

MUMBAI: HVL on standalone basis reported a total income of Rs. 26.72 Crores for the half year ended September 30, 2018. Pursuant to adoption of INDAS,...

BENGALURU: Indian direct to home (DTH) behemoth Dish TV India Ltd (Dish TV) reported profit after tax (PAT) of Rs 19.7 crore for the quarter ended...

BENGALURU: Mukesh Dhirubhai Ambani’s media arm, Network18, reported improved numbers for the quarter ended 30 September 2018 (Q2 2019, quarter under review) as compared to the...

BENGALURU: The Sunil Lulla-led Indian film and media company Eros International Media Limited (Eros) reported 25.3 per cent year on year (y-o-y) jump in profit after...

BENGALURU: The Essel group’s television news broadcasting arm Zee Media Corporation Ltd (ZMCL) reported a 386.3 per cent growth (almost five fold) in consolidated profit after...

BENGALURU: The Subhash Chandra-led Zee Entertainment Enterprises Ltd (Zeel) reported a 15 per cent year on year (y-o-y) growth in total revenue for the quarter ended...

BENGALURU: Higher competitive intensity in the market, delay in collections and issues pertaining to debt repayment are some of the reasons that Indian regional cable and...

BENGALURU: The board of directors of TV Today Network Ltd (TVTN) has recommended a dividend of Rs 2.25 (45 per cent) per equity share of face...

BENGALURU: Indian multi system operator (MSO) Den Networks (Den) reported growth in revenue and operating profit (EBITDA) for the quarter ended 31 March 2018 (FY 2018,...

BENGALURU: Backed by higher subscription revenue and a 95 per cent collection efficiency, Indian multi-system operator (MSO) Siti Networks Ltd (Siti) posted 16.8 per cent higher...

BENGALURU: Indian news, entertainment and film company TV18 Broadcast Ltd (TV18) reported triple the revenue from its film business for the year ended 31 March 2018...

BENGALURU: American multinational media conglomerate with interests primarily in cinema and cable television, Viacom Inc (Viacom) reported lower numbers for the quarter ended 31 December 2017...

BENGALURU: A recovered but not fully-up-to-speed rural sector and higher selling and distribution expenses during festival time led to Indian direct-to-home (DTH) major Dish TV India...

BENGALURU: Anil Dhirubhai Ambani-led Reliance Communications Ltd (RCom) reported 95 percent lower loss for the third quarter ended 31 December 2017 (Q3 2018, the quarter under...

BENGALURU: Subhash Chandra-led Zee Entertainment Enterprises Ltd (Zeel) today reported an 11.5 per cent and 28.3 percent increase in consolidated total revenue and profit after tax (PAT), respectively,...

MUMBAI: Multi-system operator (MSO) Den Networks’ financial results for Q3 2018 show consolidated revenue of Rs 330 crore as against Rs 293 crores in the corresponding...

MUMBAI: Network18 Media & Investments (Network18) reported a marked improvement in its numbers for the quarter ended 31 December 2017. The consolidated revenue (net of revenue...

BENGALURU: TV18 Broadcast Ltd (TV18), the subsidiary of the Mukesh Dhirubhai Ambani-controlled Network18 Media and Investments Ltd (Network 18), reported consolidated total income of Rs 10...

BENGALURU: Sunil Lulla-led Eros International Media Limited (Eros) reported 21 per cent margin (on operating income) for consolidated profit after tax (PAT) for the quarter ended...

BENGALURU: Operating profit at NDTV Digital has enabled New Delhi Television Limited (NDTV) to narrow consolidated operating loss (EBIDTA) to Rs 137.7 million for the quarter...

BENGALURU: Riding on the high of an increase in subscription revenue, Sun TV Network Ltd (Sun TV) reported improved numbers across all important parameters for the...

BENGALURU: Indian multi system operator (MSO) Den Network (Den) reported growth in operating revenue, operating profit (EBIDTA) and profit after tax (PAT) for the quarter ended...

NEW DELHI: Hamdard Laboratories gathered a cross-section of India’s achievers in New Delhi on Friday, handing out the Hakeem Abdul...

MUMBAI: For decades, creative storytelling has been the cornerstone of brand communication. The “big idea” amplified through catchy jingles, striking...

MUMBAI: Zepto has elevated Ahmad Muneeb to vice president – HR centre of excellence, placing him at the helm of...

MUMBAI: When the applause gets louder than the dialogue, you know the fans have taken over. That was the unmistakable...

MUMBAI: As audiences spread across TV, OTT, and short-form platforms, deciding what gets greenlit has become more strategic than ever....

MUMBAI: Jacques Barreau has spent two decades helping Hollywood speak the world’s languages. From The Lord of the Rings to...

INDIA: Dell Technologies is doubling down on artificial intelligence in marketing. The company has elevated Aishwarya Sudhakar to director of...

GURUGRAM: Adidas has appointed Gaurav Pathak as director of key and field accounts, bringing back an executive who began his...

MUMBAI: Myntra has stitched a new thread into its leadership fabric, appointing seasoned technologist Pramod Adiddam as chief technology officer....

A wave of panic swept through Delhi and Mumbai over the past week as viral social media posts claimed a...

MUMBAI: India’s blind women’s cricket team emerged as the standout honouree at the fourth edition of the Zee Samvad with...

MUMBAI: The FMCG arm of Reliance Industries has acquired a majority stake in Australia-based Goodness Group Global, marking its entry...

WASHINGTON: At OpenAI, the fight was not about artificial intelligence going rogue—it was about who got the GPUs.An internal email...

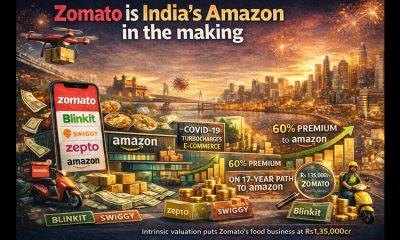

MUMBAI: Zomato, India’s dual-headed monster of food delivery and quick commerce, is marching towards profitability at a clip that puts...

INDIA: From almonds to alcohol, American imports are about to get easier on the Indian wallet. India and the United...